The dichotomies in the financial world continue to manifest with several contradictions simultaneously occurring and financial commentators scratching their heads in an attempt to make sense of things. Earnings season is in full steam this week – and looking positive – but right after GDP data seriously disappointed last week showing a lackluster economy. The commercial real estate market appears to be a disaster waiting to happen – yet continued high interest rates don’t seem to facilitate any meaningful meltdown. Fiscal deficit and total US debt numbers are at nightmarish proportions and rocketing higher – yet the US Dollar is strong and is trending higher…

Yet another example – It has been almost precisely a year since the failure of First Republic Bank the aftermath of which was the FDIC gutting the carcass of the bank and “selling” the filet to JP Morgan Chase. The financial conditions that led to the bank failure (including an inverted yield curve) have not eased and yet the banking sector has held together pretty well – until last week. Now we have Republic First Bank in Pennsylvania being closed by regulators. Although this bank is quite small compared to Silicon Valley Bank and First Republic, which went belly-up last year, one has to be concerned about the banking environment and whether or not we will see more bank failures. The big question is whether or not the ending of the Bank Term Funding Program is going to be a catalyst for more such failures…

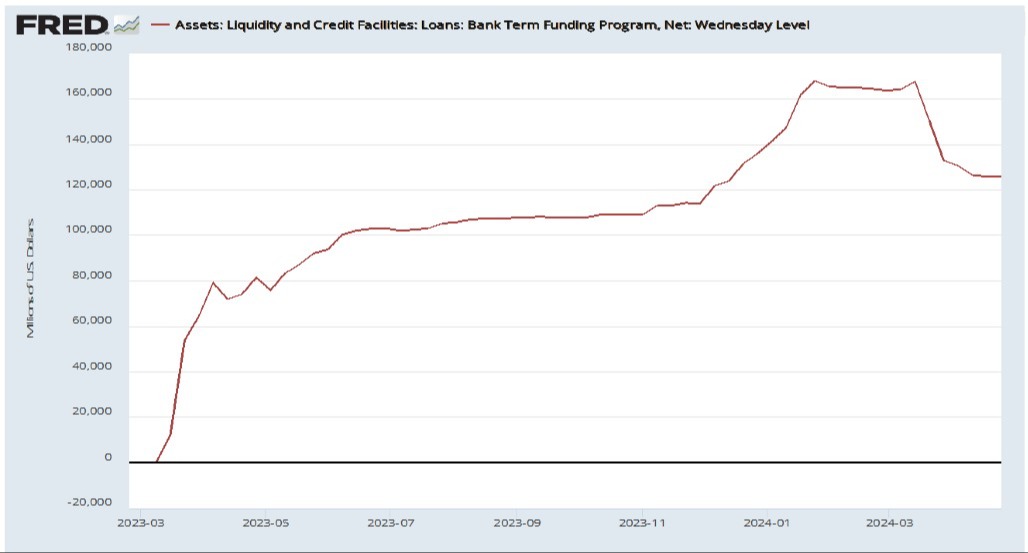

During the Covid “pandemic” interest rates went to all-time lows in the US. The ten-year treasury traded at a yield of less than .6%. With interest rates so low, of course note and bond prices are high. Many of the assets bought by banks such as Silicon Valley Bank were priced very high, and then came down as the Federal Reserve raised interest rates. So essentially, the Fed caused the problem for banks – they lowered interest rates taking bond prices very high, and then raised interest rates pushing bond prices back down. The yield curve inverted, and banks were in big trouble. In response to this, the Fed created a lending program in which banks could borrow against those under-water bonds at FULL PAR VALUE. Although many banks didn’t participate in this program because it may have strained capital requirements, banks that were in dire straits had a life raft and about $160 billion was loaned out through this program. Now it is coming to an end and the loans are due – here is a chart of the outstanding loans…

Could the ending of a small program like this be a catalyst for another round of bank failures? If $125 billion in loans has to get repriced or restructured across the multi-trillion-dollar banking system?

Could that really be what sets off more problems in our monetary system? Stay tuned…

In the meantime, some of the indicators of a change in the monetary landscape have been sending up red flags. Specifically, the Japanese Yen has sold off to multi-decade lows. Here’s another chart to take a look at:

This is another indicator to keep an eye on. As we have said for some time – the Japanese Yen is the “canary in the coalmine” for the world central banks’ continual strategy of printing money when their economy doesn’t perform perfectly. The problem won’t be the Yen going lower, if the problem comes it will be the Yen ACCELERATING lower. That would mean that the 5th largest economy in the world is in serious trouble.

As for now the US capital markets and economy are still holding together well considering some of the aforementioned concerns. This is a busy week of earnings and economic reports so we will reevaluate accordingly.

Regards and good investing,

Greyson Geiler