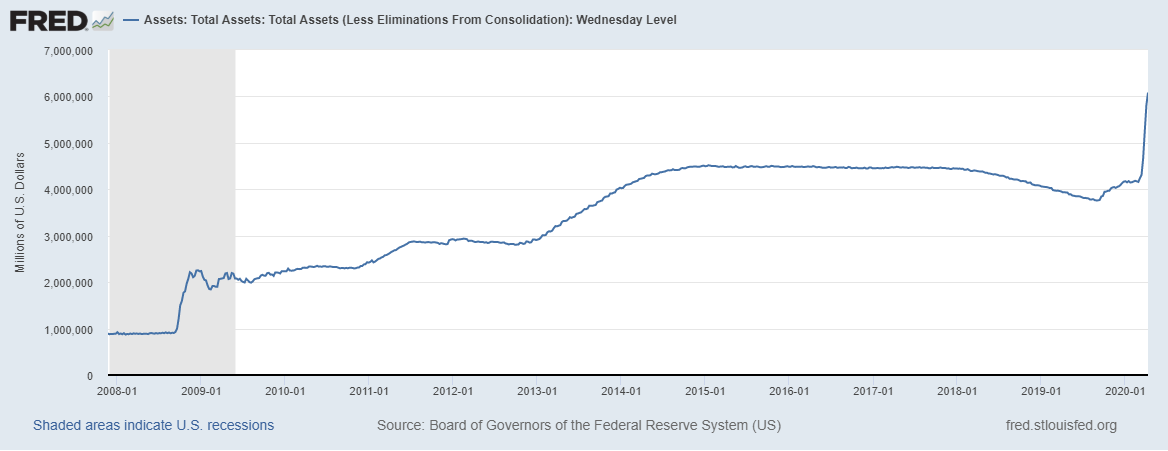

After a torrid week of gravity defying gains in the world’s stock indexes last week, we see a dose of reality hit the markets for open this week. That reality will be the earnings season that is kicking off and the question is really just how bad earnings will be. Everyone realizes that big corporation earnings will not be the 9% quarter over quarter increase that some predicted a few months ago. But will it be as bad as the 33% lower that Goldman Sachs predicted a few weeks ago? Estimates, predictions and suggestions are wildly varying – even coming from the same prognosticator. Wall Street’s formerly biggest bear, Morgan Stanley equity strategist Michael Wilson, flipped his position like a burger by becoming one of the market’s biggest bulls, saying that he is a “buyer of dips” since “2400-2600 on the S&P 500 will prove to be very good entry points for those with a time horizon of 6-12 months.” Even with such awful earnings predictions from Goldman, one of their analysts, David Kostin writes that the combination of unprecedented policy support and a flattening viral curve have dramatically reduced downside risk for the U.S. economy and financial markets and lifted the S&P 500 out of bear market territory. Our favorite dichotomy is from Oaktree Capital’s Howard Marks writing that it’s time to stop playing defense, just days after saying the worst is still to come for asset prices. Navigating these positions posted by “experts” does look like the whole system is wildly unpredictable. In all these analysts’ defense, however the actions of the Fed and the Treasury are completely unprecedented. The Fed announced last week that it will be buying up assets of all types from markets all over the world (including junk bonds.) Trying to estimate totals of what will be on the Fed’s balance sheet by the end of this crisis is folly – but from 10,000 feet we can say that it will dwarf what was purchased in response to 2008. Take a look…

Some of the “assets” that the Fed is purchasing are U.S. Treasuries (yes, this is MONETIZING our debt) because some of the foreign purchasers of our debt have been shying away. The federal government’s deficit for the first half of this budget year totaled $743.6 billion, up 7.6% compared with the same period last year and well on its way to topping $1 trillion even before the impacts of additional spending for the coronavirus pandemic. Considering the $2.2 trillion that Congress just passed, the budget deficit will top $2.5 trillion this year. The bill, the biggest economic stimulus package in United States history, was passed unanimously by the Senate on Wednesday and by voice vote with near-universal support in the House on Friday. It includes direct $1,200 cash payments to many Americans; $150 billion to help the healthcare industry; $500 billion for state and local governments and companies; and $350 billion in loans and assistance for small businesses. A debt jubilee is looming for many emerging markets (simply forgiving U.S. $ based debt) and possibly for the $1.5 trillion in dollar-based student loans. The system is hemorrhaging…

So, the Federal Reserve and the Federal Government are providing unprecedented support for the economy as the corona virus slowdown is gripping the world economy. The numbers pending in earnings season are going to be bad and that won’t recover overnight or in the next quarter. However, the prices we see of many asset prices – stocks, bonds and commodities included are decoupled from reality as there is so much central bank and government involvement. We expect things to remain extremely volatile in the near term and will invest accordingly.

Regards and good investing,

Greyson Geiler