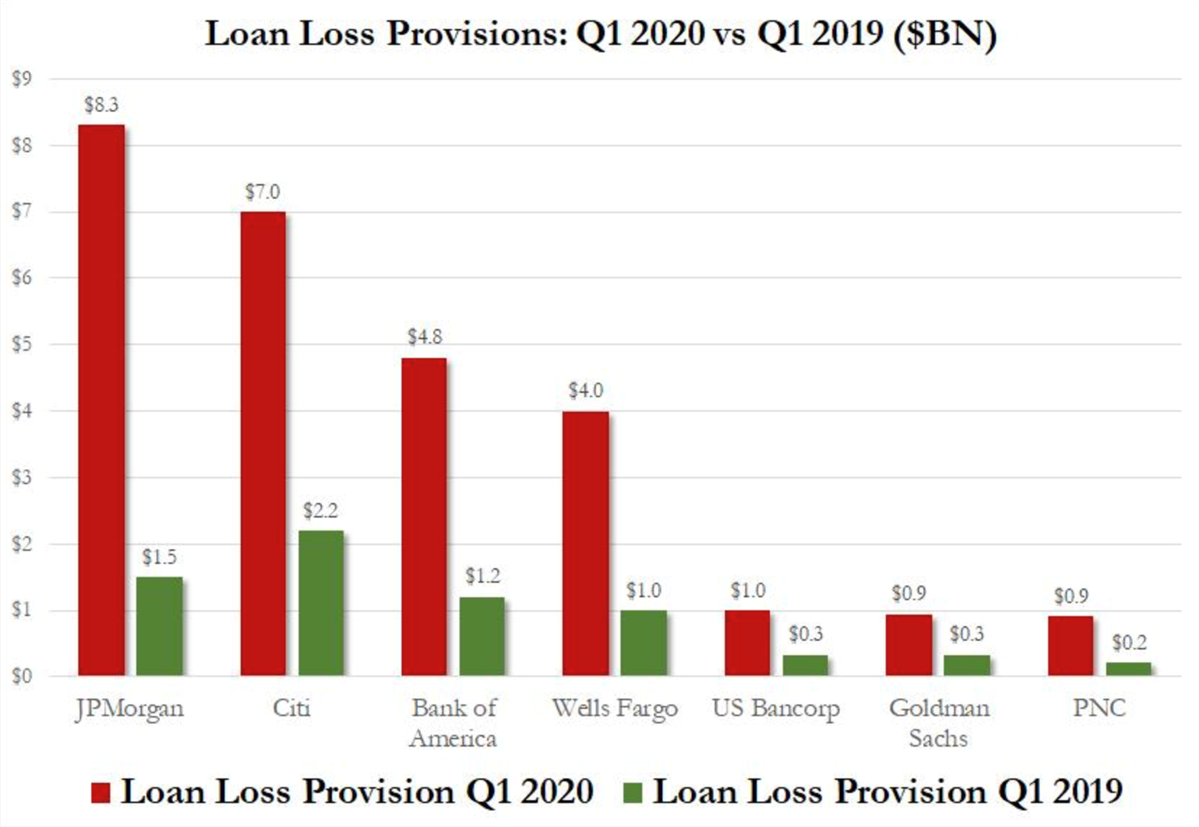

The turmoil in financial markets has been epic to say the least over the last two months. The coronavirus has effectively halted the world economy – and after the longest expansion in U.S. economic history, U.S. banks are officially bracing for impact. Now that we have seen all the big banks’ quarterly earnings and reports, the most interesting part is the loan-loss provisions that the banks are taking on in preparation of accelerating defaults…

To put this in context, so far the Big 4 banks have reserved an additional $24BN in Q1 for future loses. Of course, no one knows exactly how big those future losses will be, but if 2008 was used as a baseline, banks will have to take another $75-$100BN in reserves on loans that default. This would wipe out years of profits that weren’t saved for times like these, but instead for stock buybacks!

Going into 2020, conventional wisdom was that the U.S. banking system was over-capitalized and on firm financial footing. If that $100 Billion in losses comes home to roost, the Fed will undoubtedly be sticking the American taxpayer with the bill and it will be déjà vu all over again.

In the corporate bond world, we are talking about much bigger potential problems. The lowest tier of investment grade bond world (BBB) has ballooned to some 30% of the whole corporate bond market. Many fear massive downgrades in many of these issues which would stress the high yield (junk bond) market to domino defaults. For perspective, in 2008-09 the default rate on HY was about 15%. Now we have investment bank analysts predicting worse. Bank of America for one, thinks that things are to get dire, and don’t think much of the Fed bailouts so far writing that the Fed’s “bold, surprising” announcements “do nothing to address the ultimate credit risk – nonpayment, downgrades, and fallen angels, nor should they, and we thus remain comfortable with our existing views on expected default rates, which we estimate at 9% over the next 12mo.” However, it will only rise from there as B of A continues to make the argument that “default rates are unlikely to reach their peak levels in the next 12 months, given their historical tendency to rise only gradually following a turn in a given credit cycle. Issuers generally have a runway to deal with maturities, revolver capacity to tap, covenants to waive, and levers to pull to preserve cash by cutting employment and capex.”

As a result, B of A is sticking with its 21% cumulative default rate in HY once the credit cycle turns…

The junk bond index that we have put on the radar for readers to view as an indicator of credit cycle stress is JNK. Right now, that index is only roughly 10% off of its 52-week highs, being supported by Fed purchases and expectations of more. But there is a serious disconnect between the pricing in the high yield bond (and stocks for that matter) world and economic reality. For indicators of how that gap will narrow, we keep an eye out for defaults. in Retail, J.C. Penney elected not to make its $12 million scheduled interest payment this week, and has entered a 30-day grace period, with a default now inevitable. At the same time, Neiman Marcus Group was downgraded by S&P to CCC-/Neg O, with the rating agency viewing a restructuring as “more certain in the near term.” Other defaults included Frontier which also filed for Chapter 11 bankruptcy protection this week, while satellite provider Intelsat skipped its scheduled interest payment ($125 million). Finally, in Energy, offshore driller Diamond Offshore elected not to make its coupon interest payment. The defaults are where the rubber really meets the road and it appears that those may begin accelerating shortly. This will be a crazy week event- wise as Q1 earnings will step up a notch with 88 S&P 500 companies reporting and Europe joining the fray with 64 companies. – stay tuned…

Regards and good investing,

Greyson Geiler