Income is an important part of any investment portfolio, whether we are referring to individual

investors spending their savings in retirement, institutional funds trying to continually compound

consistent growth or any investor class in between. Over the last few decades, the #1 complaint

about owning gold has been that it’s not a “producing” asset. Legendary investor Warren Buffett

has made multiple remarks through the years alluding to gold being a pet rock, or that if you own

an ounce of gold for eternity, you will own only an ounce of gold for eternity. Since gold became

available for individual investors in 1975 the price has had a 5.68% Compound Annual Growth

Rate (CAGR) according to Macrotrends—which is strangely similar to the average of the interest

rate of the 10-year U.S. Treasury Note (5.9%), also according to Macrotrends. Of course, 10-yr

treasuries pay a coupon – simple interest rate, so we are comparing apples to oranges a bit—but

the point is that just the price increase of gold has kept up with some traditional investment

strategies since it became available in 1975…

But now we are in an investing environment where things are changing, especially with regard to

investing in gold. Gold is coming back into the monetary system and is being deployed as a

capital asset! In the last decade, a transparent marketplace has emerged of leases and bonds that

are denominated in ounces of gold and silver rather than in U.S. dollars. Once again there is an

interest rate on gold! The interest earnings of these leases and bonds are also a percentage of the

original investment—just like the treasuries discussed above. However, the percentage is a

calculation of the number of ounces of principle, not the dollar value of the ounces. This is where

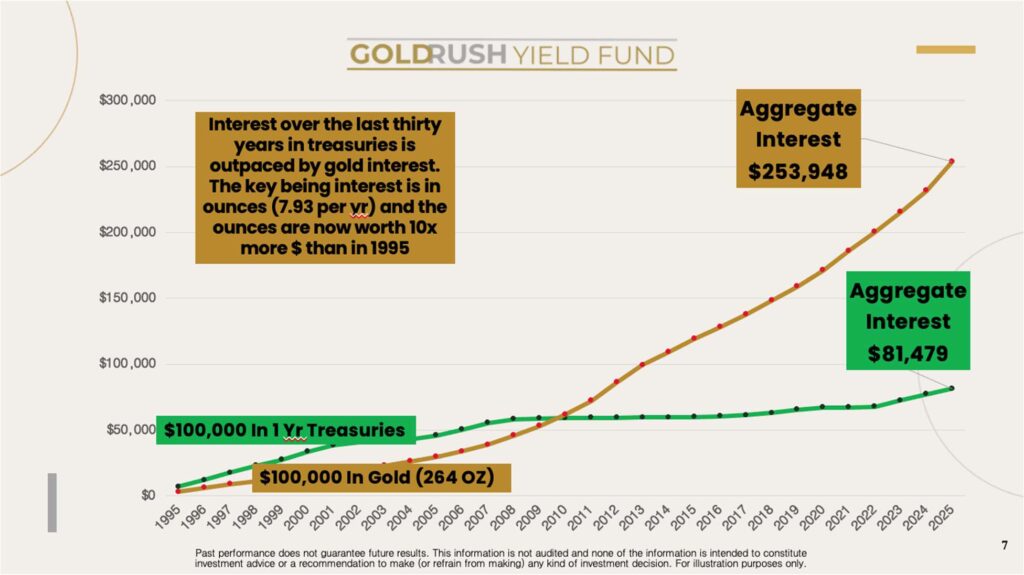

the rubber really meets the road. Let’s take a look at a chart of a comparison over the last 30

years of fixed income between gold leases—getting interest paid in ounces of gold—and ONE

YEAR treasuries to compare the same duration as the gold lease marketplace. We will

hypothetically invest $100,000 in one yr treasuries, withdraw the interest as income and keep

rolling the principal into one yr treasuries at the historical rates that occurred. The comparison is

buying $100,000 of gold (264 ounces as of Jan of 1995) withdraw the OUNCES of interest (7.93

ounces per year,) spend the dollar value of the ounces of interest and continually roll principal

into hypothetical one year gold leases at a constant 3% interest rate.

The comparison is quite staggering with the DOLLAR VALUE of the aggregate gold interest

earned being more than triple of that which treasuries paid. In the mid 1990s, there was a decent

interest rate for treasuries. But because of the “dot bomb” in 2001—and then especially after the

2008 financial crisis—the Federal Reserve kept interest rates artificially low. Consequently, the

returns on treasuries have been anemic for decades on the aggregate. The annual income in our

example for much of the 2010s was a pathetic .15% or so equating to about $150. Then we

compare treasuries to leasing gold. A thirty-year interest rate is hypothetical, but for the last

decade, the marketplace of one-year gold leases available to private investors has averaged about

3% (right now many of these leases are paying 4%). When you factor in how much the price of

gold has gone up, the 3% (7.93 OZ per year) is now income of over $20,000. That’s a pretty

good annual return considering the size of the original investment. Comparatively the income

from the treasury is now about $4000 which isn’t good – but at least better than 10 years ago…

Traditional or conservative investors might argue that treasuries are a better investment because

they are risk-free. However, we would point out that the U.S. government has restructured its

debt twice in the last hundred years casting some shadow on the “risk free.” In 1933, Roosevelt

devalued the dollar against gold, changing it from $20.67 per ounce to $35 per ounce giving a

HUGE haircut to anyone who owned some of the $22 Billion of U.S. debt. Then in 1971, Nixon

took the U.S. off the gold standard all together, which wildly repriced the dollar lower for a

second restructuring of U.S. Debt. Sadly, since then, Congress has been on absolute bonanza of

reckless spending, rocketing sovereign debt into the stratosphere ($36 Trillion). The point is that

while there isn’t any risk that you won’t get your dollars back when you own U.S. debt, but there

is a question of how much those dollars be worth…

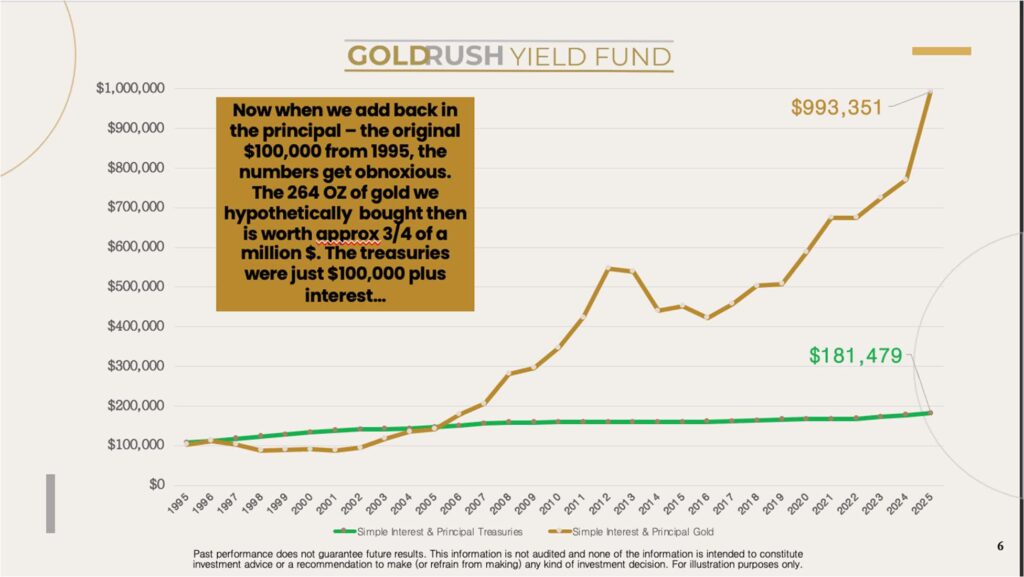

Now, let’s take a look at the second part of the equation—the value of the principle of the

original investment being added in to the aggregated interest earned over the 30-year stretch.

Again, these are hypothetical results, but if you bought $100,000 of gold in 1995 it would be

worth about $750K as of January 2025. Of course, the value of the treasury note being rolled in

our example is still just the original $100,000 from 1995…

The performance of gold over treasuries during this 30-year window is more than five to one,

and this is with simple interest being withdrawn. That is not a trivial amount of time. We would

need another chart to show the performance if interest were rolled back in, compounding over

thirty years. Gold out-performs more than eight to one in that scenario…

Obviously, assets of different types can outperform treasuries over certain periods of time. A

stock or real estate portfolio might show similar multiples of overperformance. Our objective as

investors is to design resilient portfolios that can withstand various economic scenarios rather

than depending on one specific asset class. Gold is more than a hedge – it is a necessary part of

this resilient portfolio. It is not issued by a central bank and historically it has been a stabilizer

during turbulent adjustments within monetary systems at the end of credit cycles. However, in

the past to realize any part of the portfolio protection that gold provided – an investor had to sell

gold returning them to the fiat currency issues they were trying to avoid! Now we can get

income in ounces to protect against the printing/debasement of the world’s paper currencies and

investors don’t have to time buys and sells within gold price movements to consistently realize

gains! Our Goldrush Yield Fund is a yield on gold by owning the physical and deploying into

leases and bonds for an INCOME IN OUNCES!

Regards and good investing!

Greyson Geiler

Market and industry data used in this presentation have been obtained from sources believed to be reliable. However, we have not independently verified such data and make no representation or warranty as to its accuracy or completeness.

Goldrush Yield Fund, LLC is managed by Andorra Capital, LLC, a Registered Investment Advisor. Andorra Capital has a conflict of interest in recommending the Fund to prospective investors. This material is informational only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. The Goldrush Yield Fund is an unregistered private placement and is available solely to accredited investors. No securities commission or regulatory authority has approved or disapproved of the Fund, and there is no obligation to provide investment advice. Investing in the Fund involves risks, including the potential loss of principal. Past performance is not indicative of future results. Any forward-looking statements are based on current assumptions and are subject to change. Investors are responsible for conducting their own due diligence. Please review the Private Placement Memorandum (PPM) for detailed risk factors and consult with legal, tax, and investment professionals before considering any investment. For more information, please contact Greyson Geiler at ggeiler@andocap.com