Financial markets had a rough week last week and there are indicators causing market participants to brace for another bad week coming up. Last week we talked about the inflation numbers that were to be released by the Department of Labor. The average trade guess was lower than the numbers turned out. Meaning the marketplace was anticipating inflation numbers to be calming down and that is not what happened. So now the market has to assume that the Federal Reserve will be obligated to continue raising interest rates to stave off inflation. Higher interest rates mean lower bond prices. Lower bond prices over time means lower stock prices. The stock market in general had a terrible week last week and all eyes are on the FED to see if they may actually move short term interest rates by a full 1.0% higher rather than the .75% that market observers have been assuming. So many have changed investment strategy to risk off.

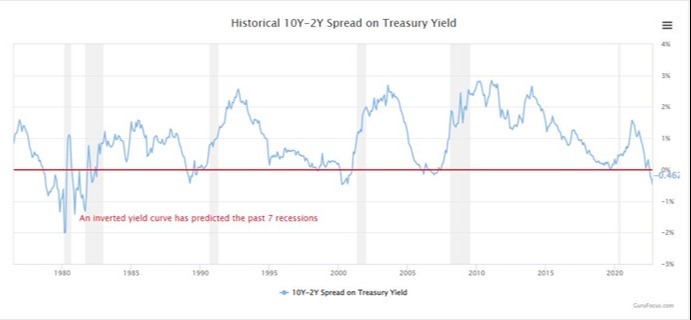

Now we have an inverted yield curve, and it looks like that is going to get much worse. Take a look at a historical chart of the 10-year interest rate minus the 2-year interest rate of treasuries…

This chart is courtesy of Gurufocus.com and it shows that the yield curve inversion is a pretty good historical indicator of recessions. Of course, the drastic inversion of the yield curve in 1981 that was orchestrated by Paul Volcker initiated a recession in the early 80s. That was Volcker’s response to reigning in the inflation of the late 1970’s. Inflation has been quite benign since then…until now.

This time around we have an order of magnitude more debt in existence which drastically magnifies the effects of higher interest rates. Again, the Federal Reserve kept emergency liquidity measures in place well after the conditions of the economy and markets warranted it. Now we are paying the price and they are going to raise rates further into an already inverted yield curve and a recession that is already in place. Some of the economic numbers – check FedEx recent guidance on their company performance – are starting to come down quite hard. That will get worse with the Fed continuing to hike rates.

The concept that with all of the world’s socio-economic problems existing today, the Fed can cure inflation simply by raising interest rates is quite naïve. One of the issues that we are facing right now is a supply side problem whether we are referring to gas, semiconductors, wheat, automobiles, housing or other things. Clearly the blunt instrument of higher interest rates will deter investment in new production and make the situation worse.

On the demand side of the equation, the Fed is getting its way by initiating a recession. This will stamp down on inflation and hopefully the higher interest rate game doesn’t keep going until something breaks. Our guess is that The Fed will have to pivot to a softer monetary strategy in short order to avoid a true detonation of the debt bubble. However, in the meantime, tighten the belt and reel in some risk if your portfolio is stressing you out.

Regards and good investing…

Greyson Geiler