With the worst of the Covid issue seeming to be in the rear-view mirror, and the Federal Reserve (and the rest of the world’s central banks) continuing to provide more “liquidity” than is reasonably necessary, we begin to look at what is coming down the pike that we need to worry about from an economic and financial market perspective. Asset prices have been rocketing higher ever since the March 2020 meltdown and look like a unicorns-and-ice cream depiction of the state of our world. So, what could derail the “everything bubble” which is what some doomsdayers have labeled the present state of our economy and financial markets? Considering where there may be rough waters ahead from an overhead perspective looks something like this…

Our biggest concern is of course the predicament of the “stimulus” that is being poured on the world’s monetary system by the central banks. There are many problems and unintended consequences of this sort of meddling by the central banks, but the most obvious is simply the mountains of debt that have been accrued. Government entities, individuals and corporations have all stacked up unprecedented amounts of debt due to the artificially low interest rates and the reigning in of natural market forces that would force liquidation and default. We could argue all day about what caused the real starting point of this debt deluge, but it is obviously accelerating at this point and that is becoming unnerving. Can the world central banks allow markets to stand on their own? We suggest that there would be unprecedented carnage of the central banks quit their injections of “liquidity” – but will they slow down? Inflation is heating up and the FED in particular, is starting to have a tough time justifying keeping the pedal to the medal. If they did back off it may take quite an economic hiccup and aggressive selloff in asset prices to bring them back to the table. Of course, they would have to come back in and “save the day” as they have taken so much control and responsibility. When would that happen? How much of a temper tantrum will the market throw when the FED takes its foot of the gas? How much “stimulus” will the markets/economy require next time around or during the next “crisis”? These questions make the financial markets more like a casino than they should be…

Next up on our list of concerns is political turmoil. The biggest ball getting tossed around in Congress is of course a $3.5 trillion “infrastructure” bill which, pass or fail could mean a lot to financial markets. Fearing more treasuries hitting the market (our government would have to issue a lot more debt,) the 10-year treasury yield has snuck back out to almost 1.5%. That interest rate isn’t a backbreaker now but what if more fiscal “stimulus” gets voted in and more treasuries hit the market pushing rates further? Other political fighting largely looks like theater, but if too many vaccination restrictions get mandated, we could see big economic pullbacks as that is a very polarizing concept. Another serious political concern that could really throw a curve ball to the economy and asset markets is the issue of corporate and personal taxation. We believe in general that tax rates will go higher, but the specifics seem wildly unorganized right now and this could turn out to be much different than any current expectations. Stay tuned…

Of course, we have to worry about China with the recent real estate and debt domino worries from Evergrande Group. The Chinese government has recently been quoted as saying they will “protect consumers” but we still don’t know exactly what that means. Some financial pundits are worried that this could still trigger a contagion reminiscent of Lehman Brothers from 2008. Markets have really calmed down with regard to this, but we certainly aren’t sure that we are out of the woods yet. China has been a disproportional driving force in global growth since the 2008 meltdown and a new debt crisis there would be hugely detrimental to the world economy.

Asset price (stock, bond, and real estate market) valuations are a concern. Overbought markets get more overbought, so trying to time the demise of a long running bull market is a fool’s errand. Bubbles don’t really collapse under their own weight, but when we have historical valuations at the sort of highs we have now, one fears that long term gains from this starting point won’t look so good. Many of the historical indicators, P/E ratios, Price to Sales ratio, Warren Buffet’s stock market capitalization to GDP ratio, corporate debt to GDP ratio – all are at or near historical highs. Again – this doesn’t mean we need to run for the hills and sell everything, however this needs to be on the radar…

Business hiccups with supply chain problems and declining margins. This is a 10,000 ft concern without real specifics. Some industries – shipping for example – are still struggling from some of the supply chains broken by the virus crisis. Some companies just can’t find the proper materials and labor to get their projects done. The intricacies of these issues are industry specific, but across the board margins are tightening on companies from every angle including corporate taxation and increasing wage/salary pressures. This could turn into some serious headwinds for the earnings of companies and dampen the justification of valuations and current lofty levels.

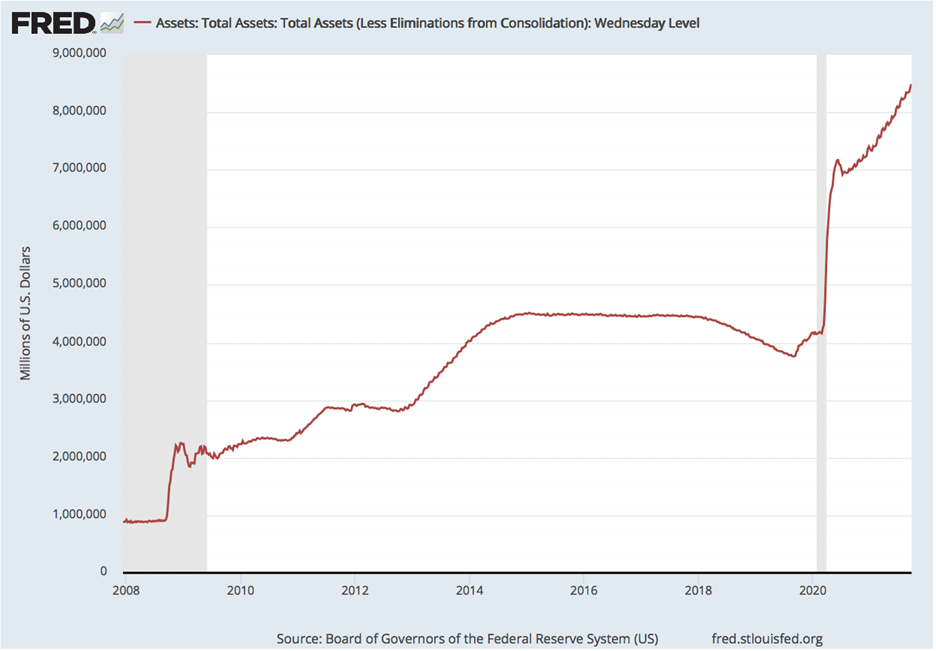

This is our worry list for now- so for our chart of the week we have the Federal Reserve’s balance sheet. This is an accounting of all of the assets they have sucked up in our financial markets over the years. One private entity (that has yet to be audited) owning this volume of assets is obviously ridiculous, but no one knows how much more ridiculous it can get before some breaking point is found…

Eight and a half trillion dollars – and counting? Wow…

One of the justifications for the creation of the FED (in the year 1913) was for it to be a lender of last resort in emergency and stave of economic/financial crisis. Now they are developing into the lender of first, middle and last resort for a comically financially profligate government. Because interest rates are so low, free markets won’t lend as much money to this government on a long-term basis that they “need.” Their balance sheet reflects buying all this debt from our government (and other assets of dubious valuation.) Historically this has been labeled “monetization of debt.” We’re not sure what people are calling it now, but it seems to us that the FED is actually creating rather than preventing financial crisis. The cure has become worse than the disease – surprise, surprise…

Clearly this won’t end well. However, we still don’t see imminent doom – but we will keep looking!

Regards and good investing,

Greyson Geiler