by Greyson Geiler | April 13, 2020

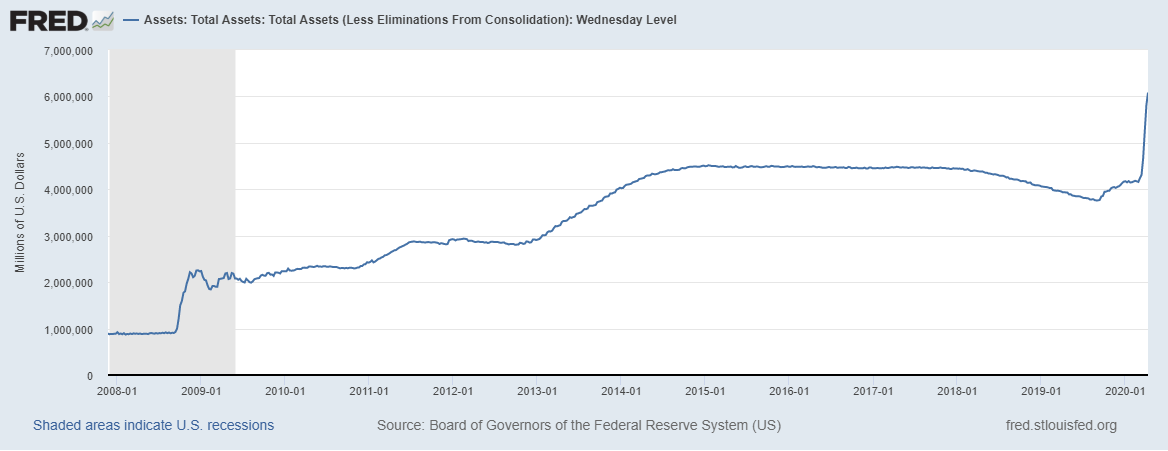

After a torrid week of gravity defying gains in the world’s stock indexes last week, we see a dose of reality hit the markets for open this week. That reality will be the earnings season that is kicking off and the question is really just how bad earnings will be. Everyone realizes that big corporation earnings will not be the 9% quarter over quarter increase that some predicted a few months ago. But will it be as bad as the 33% lower that Goldman Sachs predicted a few weeks ago? Estimates, predictions and suggestions are wildly varying – even coming from the same prognosticator. Wall Street’s formerly biggest bear, Morgan Stanley equity strategist Michael Wilson, flipped his position like a burger by becoming one of the market’s biggest bulls, saying that he is a “buyer of dips” since “2400-2600 on the S&P 500 will prove to be very good entry points for those with a time horizon of 6-12 months.” Even with such awful earnings predictions from Goldman, one of their analysts, David Kostin writes that the combination of unprecedented policy support and a flattening viral curve have dramatically reduced downside risk for the U.S. economy and financial markets and lifted the S&P 500 out of bear market territory. Our favorite dichotomy is from Oaktree Capital’s Howard Marks writing that it’s time to stop playing defense, just days after saying the worst is still to come for asset prices. Navigating these positions posted by “experts” does look like the whole system is wildly unpredictable. In all these analysts’ defense, however the actions of the Fed and the Treasury are completely unprecedented. The Fed announced last week that it will be buying up assets of all types from markets all over the world (including junk bonds.) Trying to estimate totals of what will be on the Fed’s balance sheet by the end of this crisis is folly – but from 10,000 feet we can say that it will dwarf what was purchased in response to 2008. Take a look…

Some of the “assets” that the Fed is purchasing are U.S. Treasuries (yes, this is MONETIZING our debt) because some of the foreign purchasers of our debt have been shying away. The federal government’s deficit for the first half of this budget year totaled $743.6 billion, up 7.6% compared with the same period last year and well on its way to topping $1 trillion even before the impacts of additional spending for the coronavirus pandemic. Considering the $2.2 trillion that Congress just passed, the budget deficit will top $2.5 trillion this year. The bill, the biggest economic stimulus package in United States history, was passed unanimously by the Senate on Wednesday and by voice vote with near-universal support in the House on Friday. It includes direct $1,200 cash payments to many Americans; $150 billion to help the healthcare industry; $500 billion for state and local governments and companies; and $350 billion in loans and assistance for small businesses. A debt jubilee is looming for many emerging markets (simply forgiving U.S. $ based debt) and possibly for the $1.5 trillion in dollar-based student loans. The system is hemorrhaging…

So, the Federal Reserve and the Federal Government are providing unprecedented support for the economy as the corona virus slowdown is gripping the world economy. The numbers pending in earnings season are going to be bad and that won’t recover overnight or in the next quarter. However, the prices we see of many asset prices – stocks, bonds and commodities included are decoupled from reality as there is so much central bank and government involvement. We expect things to remain extremely volatile in the near term and will invest accordingly.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | April 6, 2020

With news organizations reporting nearly nothing save the coronavirus updates, most of the world is on hold waiting for indications of a timeline for the pandemic to subside. India, China, France, Italy, New Zealand, Poland, and the UK have implemented the world’s largest and most restrictive mass quarantines. Most of the entire population of the world is on some sort of a lockdown from their respective governments. While “lockdown” isn’t a technical term used by public-health officials, it can refer to anything from mandatory geographic quarantines to non-mandatory recommendations to stay at home, closures of certain types of businesses, or bans on events and gatherings – according to Lindsay Wiley, a health law professor at the Washington College of Law. As far as travel bans, according to Pew Research, 93% of the world’s population now lives in countries or territories that are the subject of travel restrictions. Now rumors are circulating that there will be Federally mandated bans imposed on travel WITHIN the U.S. The biggest questions now of course are: how long does this last, and how bad will the societal/economic damage be? Is there any light at the end of the tunnel?

As far as the first question of timing, basically when will the civic and economic restrictions begin to be lifted in various key countries, Deutsche Bank provides some estimates largely based on the experience of the lockdown and reopening in China’s Hubei province. Many are suspicious of the data coming from China; however, this is obviously ground zero for the entire pandemic and can provide a base model in order to make guestimates from. After all, the worst parts of pandemics of this nature are the unknowns.

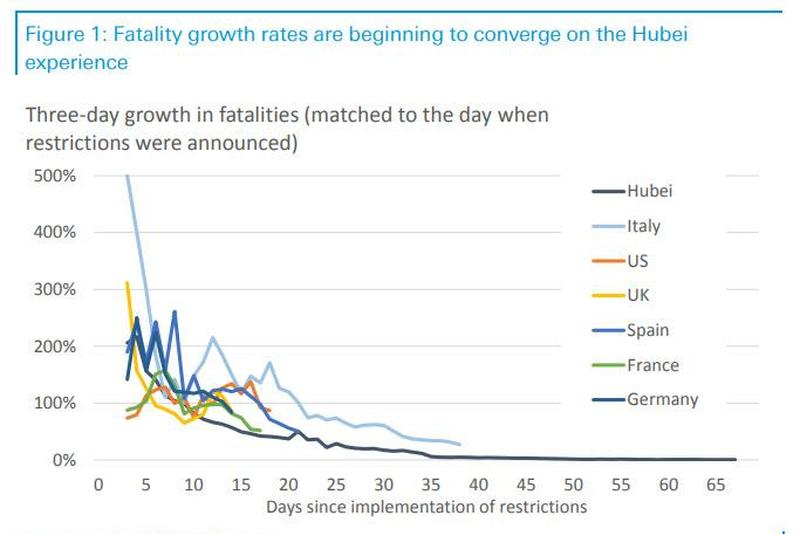

As DB notes, one way to look at how other countries are converging on the experience in Hubei province, China is shown in the following chart. As the German bank explains, it uses “a three-day comparison in order to filter out the noise from sudden jumps and drops when figures were relatively small. We also start each time series at the point at which restrictions were introduced to attempt a closer comparison. We then show all the countries individually against the Hubei experience.”

At first glance, it appears that the fatalities are falling faster in China than in other countries. However, according to DB that does not invalidate the comparison. First and foremost, China implemented restrictions earlier, quicker and in more Draconian fashion as the process of infection rolled out. As mentioned earlier, it is likely that China is fabricating some of this data as well as to appear in greater control of the outbreak than reality shows. In addition to this, the other countries compared in this chart have a greater proportion of their populations “at risk” – meaning primarily elderly. It must be noted that there can be a 14-day lag between restrictions and outcomes, and President Trump only urged social distancing on 16 March (while our time series starts at 12 March when New York implemented restrictions). In addition to that, different states in the U.S. have implemented restrictions at different times. Despite this, data is now indicating a convergence with China now that the lockdowns have been implemented in most states.

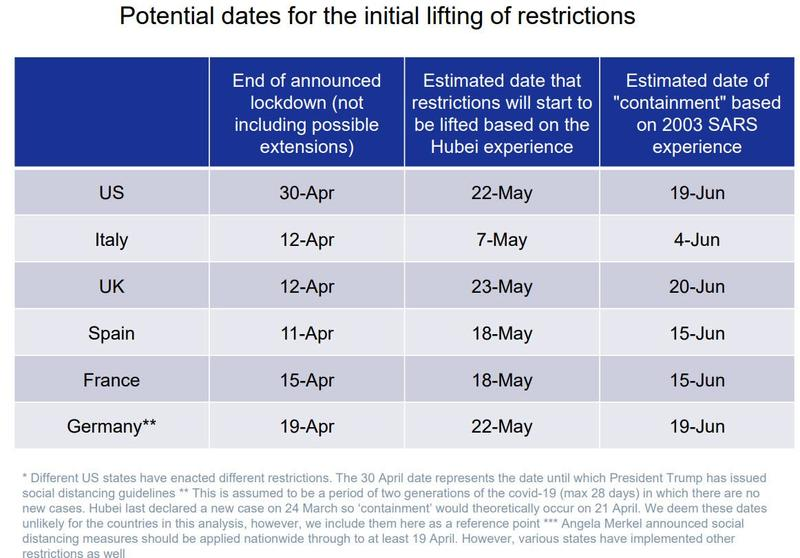

So, then we get to Deutsche Bank’s chart suggesting when restrictions may begin to ease…

Of course, a chart like this is loaded with caveats and is at best an educated guess, but it does start to visually shape this pandemic into something intellectually manageable rather than just a giant gray area. The biggest caveat, of course is that this is assuming there isn’t a relapse into increased infection numbers like what we may be getting in China right now.

Governments across the globe are doing a balancing act between imposing restrictions according to scientifically backed need for societal preservation and the civil liberties of citizens. Finally, even if Deutsche Bank is right and the lockdowns are lifted sometime in late May/early June, any loosening of restrictions would have to be accompanied by a ramping up of testing, according to Martin Lohse, professor of pharmacology at the University of Würzburg.

When we try to answer the question about how much socio-economic damage will be done, we run into even more uncertainties. On one hand we see economic numbers falling off a cliff with businesses shuttered all across the country and unemployment applications skyrocketing. On the other hand, we see bazookas of stimulus both fiscally from the federal government and monetarily from the federal reserve. In the middle we see the interpretation of what is going on represented by the price of the asset markets between stocks, bonds, commodities and real estate. The S&P 500 at about 2500 represents essentially 100% confidence that structural corporate earnings power remains solid. That level is 21x trailing 10-year average S&P 500 earnings of $122/share – for a point of reference, in 2009 we bottomed at 10x trailing S&P earnings. Right now, with businesses shuttered we are skeptical that the market confidence is well founded. Even if restrictions were completely lifted by the end of April across the developed world, we expect “getting back to normal” to take several quarters as supply chains are damaged, loans aren’t being paid, employees aren’t being trained among many other issues. In addition to that, we expect some things to simply return to a “new normal” that isn’t what it was just this last January. A good example of that is commercial real estate. Many companies are realizing that they will not be requiring the degree of office space that they were paying for before the crisis. That will obviously not be good for some real estate companies, but there may be other unintended consequences that we cannot foresee right now. That is why many companies will simply remove “forward guidance” of their earnings altogether from the upcoming quarterly reports. Companies such as Visa, Twitter, Target, Domino’s Pizza and Deere have already withdrawn their guidance for 2020. That is on top of expectations that the S&P 500 earnings for the first quarter will be down 5.2% y-o-y according to FactSet. UBS reduced its whole-year S&P 500 2020 earnings estimate to $140 per share from $170 per share.

Of course, these markets are not perfect scales for the value of underlying assets – essentially the fed’s actions have removed the remnants of normal market price discovery. Eventually we do expect some normalcy to return to markets, in the meantime however we are planning on seeing some extreme volatility as no one knows how much damage is being done to the economy and the news good or bad can push markets quickly one way or the other.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | March 30, 2020

The rollercoaster ride of the stock market has hit some unprecedented levels recently. From the high print of late February, U.S. stock indexes sold off 30 something percent – in one month. The situation overseas has been worse with Euro Stoxx nearly 40% off its high and some emerging market indexes even worse. The corona virus has turned the world economy completely upside down. Of course, the only question now is – how long will this last?

Economic numbers are awful – and by some statistical measures of course we are already in a recession. When you look at some of the numbers, even the word depression is an understatement. “It may be the largest contraction of GDP on record in a specific quarter,” said Gregory Daco, chief U.S. economist at Oxford Economics USA. He expects a 12% contraction, and some are even suggesting 15%. In our estimation this is complete conjecture right now. Expect earnings reports around the corner to be horrible. Whether a company’s numbers were already drastically affected by the virus or not will not matter. They will all report that the virus is to blame. In addition to that many companies will simply remove all guidance going forward – because no one knows how this is going to roll out. In our opinion, this will add to the exiting volatility as the market hates nothing more than complete unknowns.

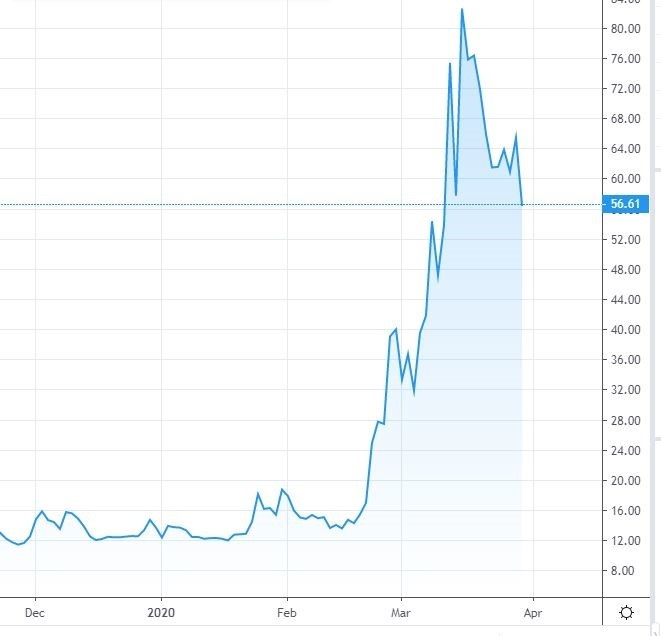

Here is a look at the VIX chart as of the writing of this post…

The VIX is a measure of volatility in the stock market – some even refer to it a chart of fear. It is calculated by a ratio of put options vs. call options which basically means that when this chart goes higher, market participants are afraid and are buying insurance to protect against the value of their stock accounts going down. There is a significant rebound in the stock market over the last week as the panic selling has abated and government stimulus is pouring in. Of course, the economy is largely on lockdown still without any end in sight. Government leaders as of today are extending versions of this shutdown out to the end of April and in some situations into June.

We are still waiting for the numbers and news to start getting less bad. Right now, we are still on the front side of the parabolic curve in virus cases that is rocketing higher. Some of the numbers from overseas appear to be evening out or even declining – Italy for example may be over the hump, but that is offset by some resurgence indicators in China and South Korea. In addition to renewed concerns in Asia, numbers out of Russia of corona virus cases are only just now being reported and lockdowns are just beginning. Russia seems to be woefully unprepared for this epidemic, and although that might not have a large direct effect on our economy, it is an indication that the corona virus scare is not even close to being done.

The entire financial world is expecting a retest of the recent lows in the stock market. In the meantime, the bounce off of those lows is large – again precipitated by unprecedented bailout packages from the world’s central banks. Things will start to calm down in the weeks and months to come, but in the meantime stay safe and don’t get caught on the wrong side of this volatility.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | March 16, 2020

The world has seen asset market turmoil over the last few weeks fueled by panic over the coronavirus situation. The fear is largely driven by the virus’ capacity to transmit quickly with little person to person contact as neither the death rate nor the death toll are daunting to this point. Businesses are closing and or asking employees to work from home. Schools, sporting events and gatherings of most any sort are closing or postponing in order to let things settle down. The result in financial markets has been a panic buy in safety (U.S. Treasury notes and bonds) and panic sell and pretty much everything else. Most major stock indexes around the globe are in bear market territory (more than 20% off of their high price.) The volatility index VIX is at its highest level since 2008.

Central banks around the globe are responding with stimulus to stave off the economic downturn that is happening – here are actions just within the last few days…

- Bank of New Zealand cuts short term interest rates by .75% to record low .25% – Says asset purchases will be next

- Canada cuts overnight lending rate to .75% from 1.25% in emergency action – Canada will establish credit support program to provide additional C$10 billion to businesses and stimulate the economy

- German Finance Mininister Scholz: Germany will have no limit on credit program form companies and Germany will spend billions of Euros to cushion economy. A safety net will be set up for “virus-hit” companies.

- PBoC (China) cuts Required Reserve Rate for some banks this morning, releasing $79B of liquidity

- ECB’s (European Central Bank) Villeroy—“We can distance ourselves from the capital key to purchase more of some countries’ debt if required”

- European Union President Von Der Leyen unveiled emergency measures to tackle the economic fallout, including flexibility on budgetary and state aid rules; 37 Billion Euro fund for coronavirus support

- Italy may spend up to 16 Billion on stimulus

- BoJ (Japan) ups bond buying overnight in unannounced move (offering to buy $1.9B), while sources story says that QE interventions will grow (e.g. Commercial Paper, ETFs, Corp Bonds)

- RBA (Australia) added $5.5B of liquidity through daily repo ops, largest since at least ‘13

- South Korea banning short selling for 6m; Italian CONSOB bans short selling; Spain’s CNMV banned short sales on 69 stocks which fell over certain amounts yesterday; UK’s FCA temporarily prohibits short selling in certain instruments; French watchdog also investigating short selling ban.

- Norges Bank (Norway) cuts rates 50bps to 1%, is prepared to ease further; cuts countercyclical buffer to 1% from 2.5% with immediate effect

- Riksbank (Sweden) lends 500 Billion crowns to safeguard supply of credit while Ingves states can buy local govt and corporate bonds and “can do currency intervention & cut rates if we think it’s needed.”

Last but certainly not least, here in the U.S., the Fed slashed benchmark interest rates by 100 basis points to a band of between 0% and 0.25%. This underscored the growing fears of the worldwide recession, the surprise announcement came just days ahead of the Fed’s scheduled March monetary policy meeting on Tuesday and Wednesday — and less than two weeks after the Fed had also unexpectedly cut rates by 50 basis points to a range of 1.00-1.25%. But wait, there’s more – the Fed also committed to $700 Billion in asset purchases which are predominately treasuries and mortgage backed securities. They also slashed reserve requirements for thousands of banks to zero. Terms on lending at the “discount window” and on dollar swap lines have also been eased. Some question the wisdom of firing so many bullets so quickly – suspecting that more Fed action will be necessary in the ensuing days and weeks. Was this too much too soon from the Fed?

Right now, uncertainty has spilled over into panic. Liquidity, meaning the ease of getting in or out of investments, has dried up and intraday volatility is wild up and down. Historically, events like this have led to opportunity and when the dust settles, we suspect this event will be the same. Of course, the question is when. Looking at Hong Kong as an example, they are about eight weeks into the situation where they really started shutting things down. They are beginning to get back to normal there – and the outbreak really never got out of hand. Hopefully we can tighten things down and get a similar outcome here in the states but stay safe and stay tuned.