by Greyson Geiler | June 8, 2020

For years we have been writing about the expansion of debt that has been taken on world-wide by countries, companies, and individuals. That trend of debt accumulation has exploded higher in the last few months in response to the economic shutdowns around the globe. The Treasury Department said weeks ago it will borrow $3 trillion this quarter alone. That is nearly six times the previous record, which was set in 2008. The Congressional Budget Office expects the federal budget deficit will hit $3.7 trillion this year, up from $1 trillion in 2019 WHEN THE ECONOMY WAS DOING WELL! So now our national debt has rocketed through $26 trillion with no end in sight. The rest of the developed world is performing similarly with debt accumulation – examples include Italy with debt totaling 160% of its GDP and Japan at a completely absurd 280%. Fed Chair Jay Powell says that now is not the time to worry about debt, so U.S. corporations have responded by loading up $1 trillion more in debt in the first five months of the year. That is the fastest pace on record. An obvious question is who is buying all this debt that is being issued? The answer of course, is the Federal Reserve and other central banks around the globe.

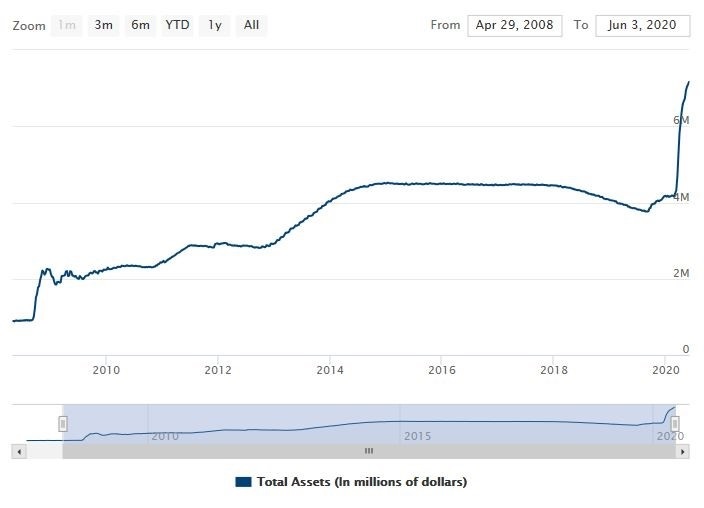

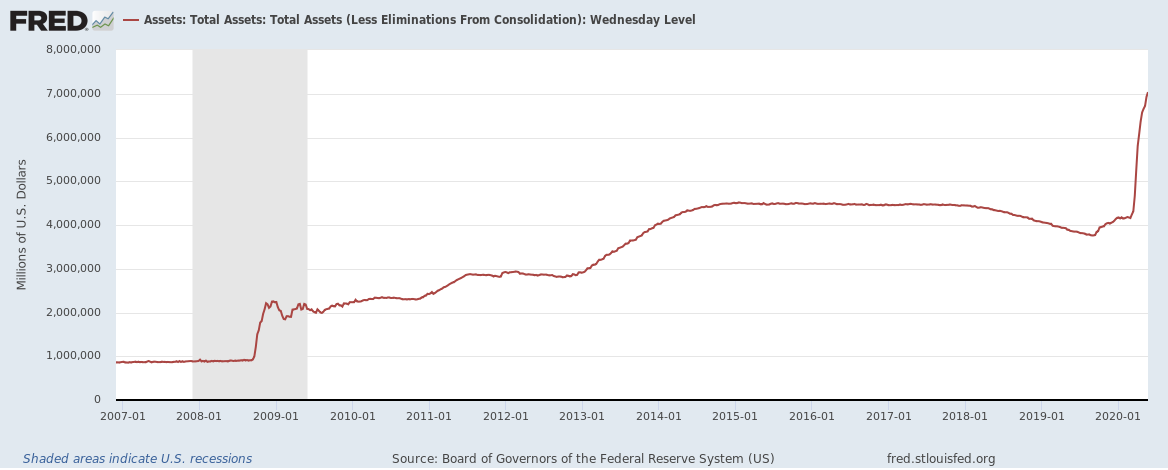

The Fed’s balance sheet has rocketed to $7.165 trillion at a completely surreal pace. Now the Fed has expanded its functionality to not just lender of last resort, but also buyer of last resort.

In the near term all the “stimulus” that is being provided has launched the stock market higher. There is a huge disconnect right now between the prices of asset markets and the economic reality underneath. While we are certain that the economy will rebound smartly from the recent shutdown, a return to the pace the economy set at the beginning of the year will simply not happen in the next couple quarters.

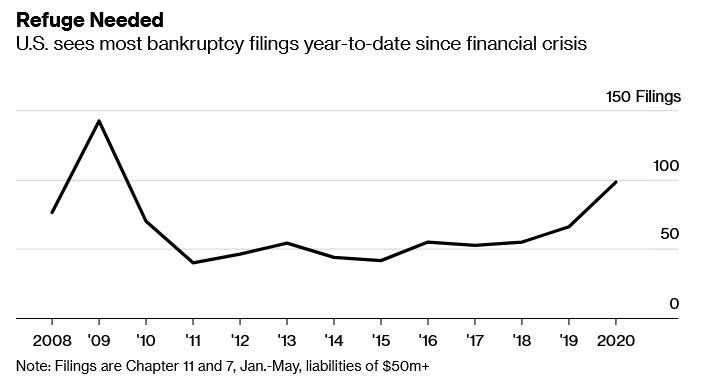

Economists have long understood that excessive debt numbers start to weigh down on business activity as time goes on. When will all this debt start to matter to our economy? It appears that the fallout is beginning in bankruptcy court…

In May 2009, 29 major companies filed for bankruptcy, according to data compiled by Bloomberg. And year-to-date, there have been 98 bankruptcies filed by companies with at least $50 million in liabilities – also the highest since 2009, when 142 companies filed in the first four months.

…and it’s not just bankruptcy. Investment grade corporate debt being downgraded to junk has already surpassed $150 billion which is a new all-time record and it is only June. Comparing to previous recessions, the total may approach the $450 billion range by the end of the year. The Fed has expanded its range of assets that it intends to buy to include some of this junk debt – but probably only in the $30-40 Billion range – so there will surely be some serious fallout. Remember a lot of the owners of this debt have to sell what is downgraded to junk and numbers this large could overwhelm potential buyers. Certainly, there will also be fallout in the government pension world where, even before the crisis some estimates guessed pensions are $4 trillion underfunded. State and local government revenues have collapsed in recent months and this is not a problem that will just go away.

The monetary and fiscal stimulus that our fearless leaders and money printers have provided starts to run out in June and July. There will likely be more measures enacted, however the timing is still up in the air. Right now, the stock and bond markets don’t appear to be worried and prices will likely continue higher in the short term.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | May 26, 2020

Risk on is the name of the investing game right now with the S&P 500 back above the 3000 level and the ten-year treasury yields sneaking back up over .7%. Bad economic reports and flare-ups political between the U.S. and China have quickly been shrugged off as “priced in” and every glimpse of promising results from vaccination studies are aggressively bought. Although a Bloomberg survey of current business conditions is literally the worst ever, a similar survey of expectations of better business ahead is at the highest level ever. Of course, everyone is acknowledging that the backstop the FED has provided is the de facto driving force for asset markets. The FED has been on a buying binge (they have even bought junk bond ETFs) to support markets and their balance sheet has rocketed over $7 trillion ($7.037 trillion as of last Wednesday.)

Stock markets worldwide, in fact have picked up considerably as other central banks are following suit – flooding the markets with “liquidity” as the fundamentals of the world economy take the biggest hit in history. Foreign governments are also following suit with free-money handouts/bailouts just as in the U.S. As an example, the Bundesbank in Germany just authored a $10 Billion bailout of Lufthansa. There is quite an obvious disconnect between stock prices and current economic reality. Time will tell whether the gap is corrected by an economic resurgence or by lower asset valuations. However, there is still a tremendous amount of economic damage to contend with over the months to come. For the second quarter, GDP estimates in the -30.5% (NY Fed) to -41.9% (Atlanta Fed) tracking range. Whether the realized contraction of the U.S. economy is simply dismissed as priced-in or if it shocks risk assets off their upward trajectory will largely be a function of investors’ interpretation of the Fed’s reaction-function to additional weakness as the post-pandemic landscape comes into focus. Right now, investors are depending on the Federal Reserve not having come close to exhausting its toolbox. What specifically the FED will focus on is speculative and timing is questionable, but the FOMC has a strong incentive to keep something in reserve once V-shape recovery ambitions are fully abandoned.

The magnitude of this economic contraction is so extreme that there is not any historical context. The speed and power of the March contraction in asset prices has left us looking for a benchmark for valuation as the majority of corporations are not guiding going forward and the concept of Price-to-Earnings ratios, for example, are completely ambiguous. The rebound in markets will undoubtedly overextend and although we don’ t know where that over-extension is price or time-wise, we are sure to see some risk priced back in to the market as the economic switch isn’t magically turned back on in June.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | May 11, 2020

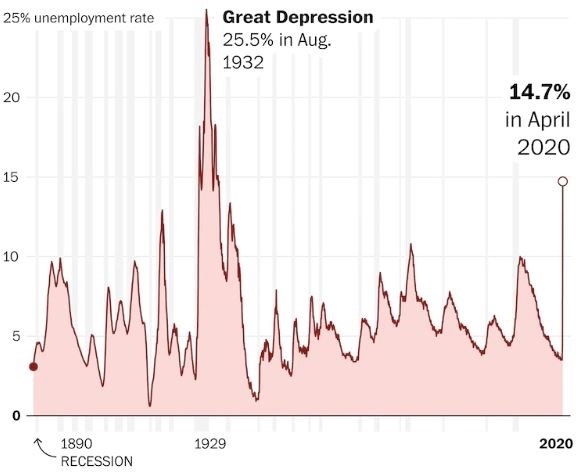

If you are looking at a chart of the U.S. stock market indexes, you may think that the Corona Virus challenges are behind us and we are back to a full-steam-ahead sort of economy. The fundamentals of the economy, however, show a completely different story. The Atlanta Fed’s GDP Now is estimating a -34.9 percent Q2 GDP print, which is 3.5x the largest quarterly decline in the post-WWII economy. When you add in the unemployment numbers it looks surreal. Friday’s April U.S. payrolls report showed 20.5 million jobs lost when in an ordinary downturn 200,000 might be considered bad; the drop in March alone was larger than that seen during the worst of the global financial crisis. We face a global future of mass unemployment (now 14.7% in the US and 13% in Canada) and this is being stacked on top of a mountain of debt – government, business and personal. The Labor Department stated the unemployment rate would have been about 20 percent if workers who said they were absent from work for “other reasons” had been classified as unemployed or furloughed. The official 14.7% figure also does not count millions of workers who left the labor force entirely and the 5 million who were forced to scale back to part time.

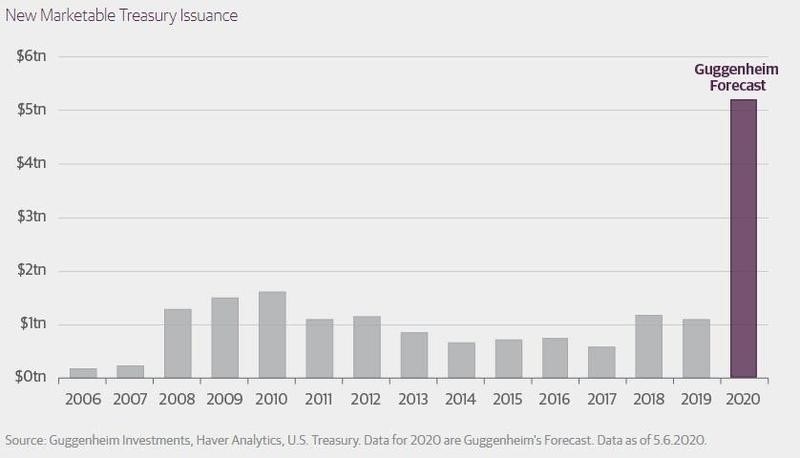

The Treasury recently sold a supersized Three – Year auction coming at a record high amount of $42Bn vs $40Bn last month. The yield was also record low at .23%. The “bid to cover” ratio was very high as well – meaning many more attempts to buy these notes than there were notes available to buy. Why all this demand for these very low-yielding notes? Because all the buyers know that they can turn around and sell these purchases to the Federal Reserve for an arbitrage profit as the Fed monetizes our debt.

The U.S. Treasury will have to issue on the order of another $3 Trillion this year and that is from programs/legislation/handouts that we can see right now. These numbers are likely to go much higher, and the investing world cannot absorb all this debt. The Fed will have to continue stepping in with “QE” and continue purchasing Treasury debt. This is dangerous in that it props up the prices of these treasuries to a staggering level with ENORMOUS new volume. Without the Fed buying there would be a meltdown in the price of the government bonds which would likely spill over into every investment class imaginable. As Scott Minerd at Guggenheim Investments put it:

Every time we get ourselves into a recession, the total debt of the U.S. economy rises relative to gross domestic product (GDP) to new and higher levels. This is not sustainable in the long run, even if we are able to push interest rates into significantly negative positions on a sustained basis.

We are all government-sponsored enterprises now…

The economic numbers will of course begin firming up in the next few months as people start to get back to work. However, if history is any guide, the unemployment numbers are likely to be in the 10% area well into 2021. Other challenges are popping up as the whole world is struggling with the recent shutdown. Our government is issuing new threats to the Chinese and that is being reciprocated – so the situation appears to be deteriorating. Saudi Arabia is in a world of economic trouble with the crazy-low price of oil, and the sustainability of them continuing to price oil in U.S. monetary terms may be in question. Of course, the election looming in November could throw a huge wrench into the works of an economic rebound no matter how you look at it.

The government debt numbers are off the charts, but in the meantime, the stock market is doing well, and the economy is starting to reopen. There is an ocean of investment account cash waiting for a retest of the lows of March to buy in – so that retest probably will not happen. However, we do suggest keeping some investable cash available as there WILL be opportunities going forward without chasing the market higher – and of course, don’t sell your gold.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | April 27, 2020

Tumultuous market trading has settled down over the last couple weeks with the VIX (volatility index) settling well back below forty. However, this week we will be bombarded with the peak week of Q1 earnings as well as announcements from the Federal Reserve and ECB on policy decisions. The BOJ has reiterated a no holds barred type policy of asset purchasing already. “This coming week will be huge from a macro data perspective and the extent to which the global economy has been floored by Covid-19,” said Simon Ballard, chief economist at First Abu Dhabi Bank. Starting with earnings, DB’s Jim Reid notes that the first quarter earnings season hits a climax this week, with a third, or some 173 companies in the S&P 500 reporting, along with a further 95 in the STOXX 600.

Overall analysts expect a decline of nearly 15% in first-quarter earnings of S&P 500 companies. In actuality, so far, this earnings season that is more like a decline of 24% – with profits for the energy sector estimated to have slumped 68%. While 65% of U.S. companies that have reported beat estimates (vs 50% in Europe and Japan), this represents the worst margin in a decade. The U.S. credit card companies are a must to watch as we expect severe deterioration in credit quality among U.S. consumers and will be a good leading indicator on the health of the consumer. The remainder of earnings season will have to perk up to meet the “only” 15% drop expectations. As far as the earnings going forward, 90% of those reporting have removed forward guidance adding uncertainty.

This week sees a number of high-profile releases of economic data that will be of interest to market participants. The first look at Q1 GDP readings will be closely watched, with the U.S. reporting on Wednesday (BofA expects real GDP to plunge 7% in 1Q,) and the Euro Area following on Thursday. Attention will also fall on initial jobless claims which are likely to increase another 3.5M for the week ending April 25. That would bring the total for the past 6 weeks to 30 million workers laid off!! That is nearly 23% of the entire U.S. workforce. We will also see reports of ISM manufacturing numbers and consumer confidence. Core inflation numbers will likely be little changed…

Everyone wants to know if the bear market is over and the all-clear signal can be raised for stock investing. We are quite surprised at the fact that the S&P 500 trades just 17% below its all-time high amid the largest economic shock in nearly a century. However, below the surface of the market, the median S&P 500 constituent trades 28% below its record high. This 11-percentage point gap is one measure of market breadth and is caused by the Big 5 (MSFT, AAPL, AMZN, GOOGL, FB) now account for more than 20% of the S&P 500. That is a new, all-time-record which rings of past market peaks rather than corrections. A broader market participation would make for a more comfortable market rally. Another concern from a technical standpoint about the market rally is declining trading volumes as the market goes rebounds. This is generally an indicator the rally may be running out of steam.

And finally, here is a picture of the state of the energy markets – a chart of crude oil. This is the most important commodity in the world and the driving force behind all the world’s economies. We have mentioned many times in the last few years that the price of crude oil drastically declining would concern us about the condition of the world economy. That has obviously happened, and we are concerned. The impact of commodity pricing over the last two months is breaking supply chains of all sorts of goods and services – the full implications to the total economy no one yet knows. Enjoy the week!

Regards and good investing,

Greyson Geiler

by Greyson Geiler | April 21, 2020

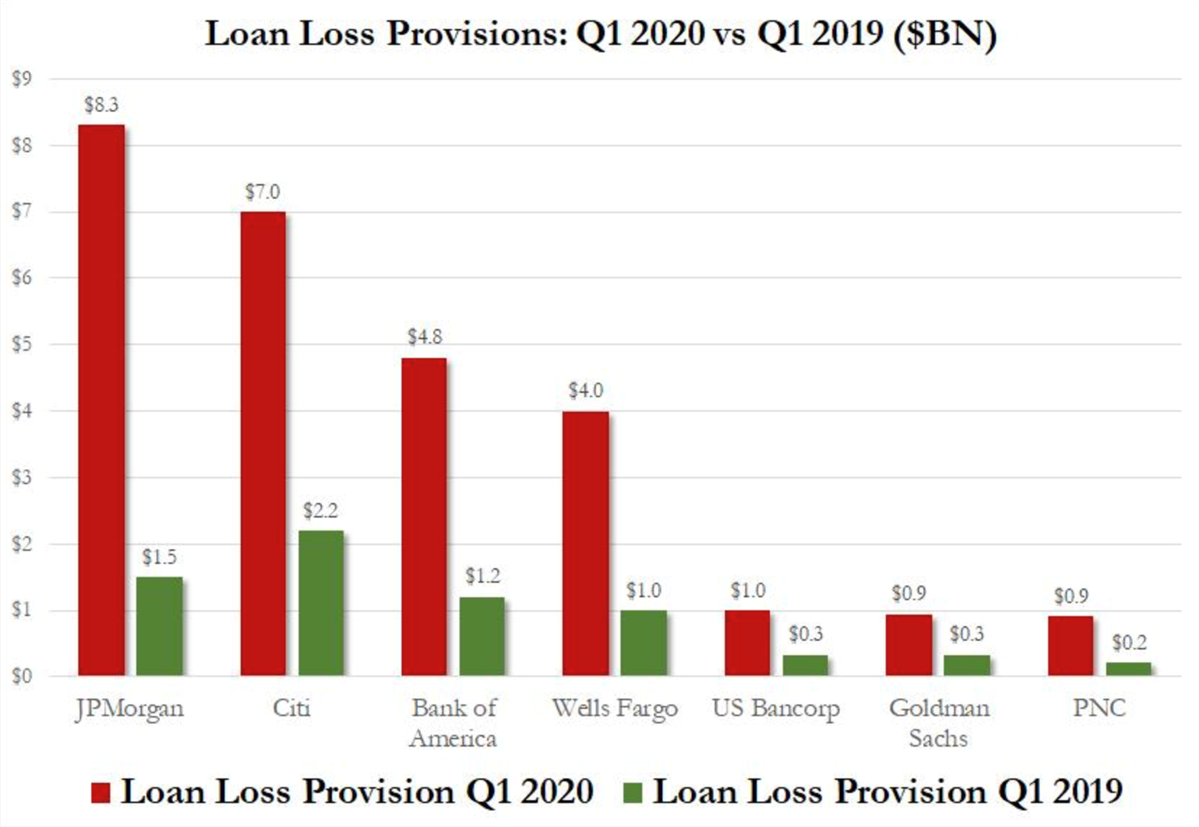

The turmoil in financial markets has been epic to say the least over the last two months. The coronavirus has effectively halted the world economy – and after the longest expansion in U.S. economic history, U.S. banks are officially bracing for impact. Now that we have seen all the big banks’ quarterly earnings and reports, the most interesting part is the loan-loss provisions that the banks are taking on in preparation of accelerating defaults…

To put this in context, so far the Big 4 banks have reserved an additional $24BN in Q1 for future loses. Of course, no one knows exactly how big those future losses will be, but if 2008 was used as a baseline, banks will have to take another $75-$100BN in reserves on loans that default. This would wipe out years of profits that weren’t saved for times like these, but instead for stock buybacks!

Going into 2020, conventional wisdom was that the U.S. banking system was over-capitalized and on firm financial footing. If that $100 Billion in losses comes home to roost, the Fed will undoubtedly be sticking the American taxpayer with the bill and it will be déjà vu all over again.

In the corporate bond world, we are talking about much bigger potential problems. The lowest tier of investment grade bond world (BBB) has ballooned to some 30% of the whole corporate bond market. Many fear massive downgrades in many of these issues which would stress the high yield (junk bond) market to domino defaults. For perspective, in 2008-09 the default rate on HY was about 15%. Now we have investment bank analysts predicting worse. Bank of America for one, thinks that things are to get dire, and don’t think much of the Fed bailouts so far writing that the Fed’s “bold, surprising” announcements “do nothing to address the ultimate credit risk – nonpayment, downgrades, and fallen angels, nor should they, and we thus remain comfortable with our existing views on expected default rates, which we estimate at 9% over the next 12mo.” However, it will only rise from there as B of A continues to make the argument that “default rates are unlikely to reach their peak levels in the next 12 months, given their historical tendency to rise only gradually following a turn in a given credit cycle. Issuers generally have a runway to deal with maturities, revolver capacity to tap, covenants to waive, and levers to pull to preserve cash by cutting employment and capex.”

As a result, B of A is sticking with its 21% cumulative default rate in HY once the credit cycle turns…

The junk bond index that we have put on the radar for readers to view as an indicator of credit cycle stress is JNK. Right now, that index is only roughly 10% off of its 52-week highs, being supported by Fed purchases and expectations of more. But there is a serious disconnect between the pricing in the high yield bond (and stocks for that matter) world and economic reality. For indicators of how that gap will narrow, we keep an eye out for defaults. in Retail, J.C. Penney elected not to make its $12 million scheduled interest payment this week, and has entered a 30-day grace period, with a default now inevitable. At the same time, Neiman Marcus Group was downgraded by S&P to CCC-/Neg O, with the rating agency viewing a restructuring as “more certain in the near term.” Other defaults included Frontier which also filed for Chapter 11 bankruptcy protection this week, while satellite provider Intelsat skipped its scheduled interest payment ($125 million). Finally, in Energy, offshore driller Diamond Offshore elected not to make its coupon interest payment. The defaults are where the rubber really meets the road and it appears that those may begin accelerating shortly. This will be a crazy week event- wise as Q1 earnings will step up a notch with 88 S&P 500 companies reporting and Europe joining the fray with 64 companies. – stay tuned…

Regards and good investing,

Greyson Geiler