Predicting the future price movement of actively traded commodity, bond, stock markets – really any market for that matter – can be very difficult endeavor. Indeed, sometimes it borders on a fool’s errand. However, focusing on something we do know – we have maintained for a very long time that our Federal Reserve along with other central banks around the world have had the habit of maintaining interest rates consistently too low. One of the reasons this is bad is because in general, when interest rates are artificially low, too much bad debt is created and worse yet – underlying currencies become devalued. Some of our worst fears appear to be looming on the horizon from this perspective with dangerous looks from inflation numbers. The short answer is we don’t know how high interest rates are going. Running a fiat currency system is a difficult prospect – so let’s take a look at some of the workings behind the scenes that may help us understand more of what’s going on in our capital markets…

When you are in charge of a debt based monetary system like the one we have, a very important consideration is how much demand you have for your currency. Remember ALL of our money originates from debt – our money is borrowed into existence. If everyone in the world paid off all of their debt – there would be no money. Sit with that for a while…Even the cash in your pocket is on the debit side of the Federal Reserve’s balance sheet – the Fed essentially owes you something for the cash you have. CASH IS A DEBT INSTRUMENT TOO! So, intuitively when interest rates are low, it is easier for borrowers to take on debt therefore much more is created. More debt is taken on by governments, businesses, individuals – essentially everyone will take on more debt with low interest rates because the payments to service the debt are lower.

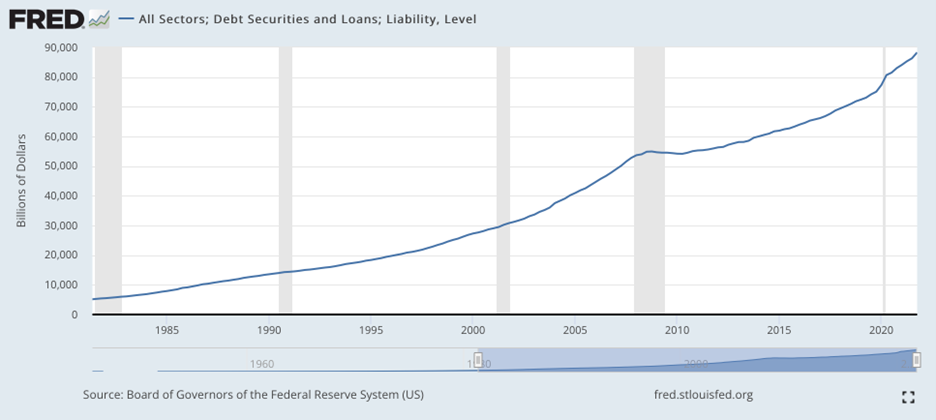

Interest rates have been coming down since the early 1980’s and the total debt outstanding – government, corporate and personal – embarked on quite a rocket launch. Take a look…

Yes, you are reading that correctly – total debt was about $5 trillion in 1980 and after 40 years of declining interest rates we are almost to $90 trillion. As bad as that may seem – and as dangerous in a rising interest rate environment as it is – it isn’t all bad. Back to our previous point, an important part of a currency maintaining is value is demand for said currency. Well with all of that debt out there, someone needs to acquire dollars to pay for the debt service.

Counterintuitively, continually lowering interest rates can have a deflationary effect as people have to pay debt back– just check out the last 30 years in Japan. The creation of the debt can be inflationary (that is supplying new money)– the servicing of the debt can be deflationary as there is a demand for money to make interest payments and those payments aren’t being used to consume.

But what does that have to do with our present situation and answering the question of how high interest rates can go? A big part of the answer to that question is loan demand. Because of the higher interest rates business loan and mortgage loan demand has fallen off of a cliff. The Fed doesn’t need to panic raise interest rates to stave off new money supply (loans created– that has already happened). As far as the deflationary effect of servicing debt – that is firmly in place too. Part of the boom in debt that you see on the chart above is a function of old debts being refinanced (instead of being paid off) at lower interest rates – accelerating the boom.

Now with interest rates higher already than they have been in a decade, borrowers will have to pay off debt – a deflationary force. Then we get to the nasty part about debt default and that is another deflationary force (if it happens in the private sector.) As we have said in this post many times there is a lot of bad debt in our system and if it starts defaulting it could cascade into a serious deflationary environment. In our view, from here the financial markets can’t handle much higher interest rates because as addicted as we have become to low rates, removing them would create serious withdrawal – something will soon break…

The inflation numbers that came out last Friday were a big shock to the whole system. Expectations were for May inflation numbers to be subsiding but in reality, it came in at 8.6% – the highest year over year number in 40 years! So now the Fed is in a conundrum and the financial markets know it. We don’t believe that combating inflation simply comes down to the Fed raising interest rates. We have always had a problem with one entity setting the cost of money (interest rates) for the entire globe. Now the complexity of the system illustrates exactly why. Many things going on right now only get worse with the Fed aggressively raising rates but we fear that is exactly what they will do.

Here are some inflationary forces in our world right now that raising interest rates will not fix:

- First and foremost – of course – the price of oil and natural gas. When you look into details of Friday’s CPI numbers, energy is BY FAR the biggest problem. This is partially because of Russian sanctions – but also many Western Governments are forcing green energy legislation before a viable supply has been created. Plus, research and development in the oil and gas space has been put on hold as no one wants to commit capital in a space the government has its boot on the throat of. Speculators know this and crude oil-based investments have been bid up in financial markets as a “safe haven” and are essentially the only asset class that hasn’t sold off in recent months. This is creating a “perfect storm” of higher prices in the energy world.

- Food costs – much of the production of food is dependent on energy prices as is its distribution. On top of that, natural gas and potash are key ingredients to fertilizer of which Russia is one of the world’s largest suppliers. Raising interest rates will not grow more food.

- Lockdowns in China due to Covid bottling up production and distribution of many consumer goods. We have no control over when these forces subside.

- Supply chain breakdowns due to many different factors including government intervention of varying types and, of course, energy costs. Raising interest rates will only make this worse.

- Low labor market participation rates due to a complex combination of issues including unintended consequences of government Covid intervention.

- Frightened consumers have bid up some consumables to avoid scarcities if socio-economic conditions worsen.

- Being a landlord is a difficult endeavor in benign economic times. Not only are economic times not benign now, but in recent years governments including federal, state, county and municipal have drastically complicated issues. Thru its post Covid asset purchases, the Fed spurred a wild boom in real estate prices that flowed through to higher rent prices. Now mortgage applications have fallen off a cliff, and mortgage-backed securities traders observe that this last Friday was the worst day in mortgages since 2008. Not good. The single-family home and rental real estate market has hit a wall and the only thing higher interest rates would do now is additionally limit the ability of homebuilders to create new supply that has been hampered for decades by government regulation.

World-renowned economist Milton Friedman famously said that inflation is everywhere and always a monetary phenomenon. If that were true, the Fed should aggressively continue to raise interest rates because inflation is running hot. However, we respectfully disagree with Dr. Friedman. Monetary (and fiscal) policy has been wildly too loose for a very long time -that is true – but right now we feel that government intervention is a bigger problem. The yield curve is already inverted – 5-year yields are higher than 10-year yields – and the economic slowdown is ALREADY HERE. We fear that the Fed aggressively raising interest rates into this (and continuing the runoff of their overly inflated balance sheet) will break something. If something in financial markets does break, the Fed has proven in the past that they will quickly change course and pour more easy credit on the game. Wash, rinse, repeat.

To return to the original question of how high will interest rates go – we would be surprised if they go much higher at all than they are today on the longer end of the curve- 10 year. The Fed is meeting this week and will certainly raise short term rates. That is already priced into all asset markets. Thoughts are that they may raise .75% or 1.0% in response to Friday’s inflation numbers. That may not be priced in and if the Fed does raise that much we may see more selling of already depressed asset markets. One sliver of good news we can report is that the U.S. dollar is not depreciating vs other currencies! But volatility in financial markets is becoming the norm.

Stay tuned…