by Greyson Geiler | June 6, 2022

One day the U.S. stock indexes are up big in a 2% rally and the next day they give it all back. The markets are watching the news and bad news is good and good news is bad. That is how backwards the whole situation is. If the economic news is good, then the Federal Reserve will have to raise rates more quickly so investors should sell stocks. Conversely, if the economic news is bad, then buy stocks because it means the Fed won’t have to raise rates as much. Of course, this is an oversimplification of what’s going on in our markets, but this backwards thinking is one of the driving forces moving our markets right now.

Most of the big investment companies have thrown out their warnings of economic storm clouds on the horizon. Jamie Dimon the high-profile CEO of JP Morgan Chase used the term “hurricane” for what he sees coming at our economy and markets. Dimon cited Russia’s invasion of Ukraine, inflation and higher interest rates. To that string of negatives, we can add a pronounced deceleration in world growth forecasts and a Chinese economic performance so anemic that it could lag behind the U.S. for the first time in almost two generations.

In our opinion, there are quite mixed economic numbers that show a muddy picture filled with many unknowns rather than an obvious economic recession. An obvious example of this bad retail sales numbers from Target, Amazon and Walmart – yet the last employment numbers from the BLS were very strong. Year over year wage increases are quite good at 5.2% but yet the individual saving rate as a percentage of income is very low. Take a look…

That chart doesn’t instill confidence in the future of the economy, but hopefully at least some of the lack of savings is due to some commodity price increases that may abate in coming quarters. Right now, many people have already braced for some version of an economic slowdown varying in opinion from a mild recession to a total Armageddon. Assets have been sold, expectations lowered, expansion plans delayed, etc. Certainly, Jamie Dimon doesn’t wait until AFTER he tells the market a hurricane is coming to sell stocks and tighten up his portfolio. The point being that many times when estimates look so bad, things tend to get better. When so many investors are sitting on so much cash looking for a home, there is always resistance to markets selling off precipitously. Obviously, there will be a price to pay for the ridiculous fiscal and monetary stimulus provided by our “leaders” during Covid. But no one knows what the timing of that will be – and of course, the big unknown, is how much the Federal Reserve actions accelerate the slowdown. If the Fed keeps raising rates and selling assets back out onto the markets which they bought them from over the last 2 years, eventually at some point something will break. Of that we are certain. We don’t see much different from previous cycles of Fed generated booms and busts, except maybe how much of a hair trigger the Fed has to lay off tightening and go back to easing monetary conditions. If it feels too much like a Russian roulette for you, raise some cash on the current rally – but don’t sell your gold…

Regards and good investing,

Greyson Geiler

by Greyson Geiler | May 23, 2022

The technical definition of a bear market is a rather arbitrary label that comes from the S&P 500 20% or more off its high print. We got there last week. A similarly arbitrary definition of a recession is two quarters of negative GDP growth. Many economists think we are going by the time numbers come in for quarter two this year. Whatever label you put on it, things are looking pretty rough. Gas prices are up, food prices are up. Stock prices and real estate prices are finally down. That’s the reality of asset markets – of course the million-dollar question is – where do these prices go from here? Is this just a pullback as the world economy gets back on track after the corona virus and lockdowns that have continued in Asia? Will the Ukraine/Russia conflict be resolved so people can get back to work?

One lingering question is if the economy is so good and things are running so hot that the Fed has to raise interest rates, then why is the market slumping so severely? Or is the market slumping because the Fed is raising rates and removing its stimulus? We are regularly skeptical of the Fed – even the concept of the Fed – but that is what we have to deal with.

So one of the indicators that we mentioned a few weeks ago was the differential between junk bonds and treasuries. In short, this is the difference in interest rates that higher risk corporations have to pay to borrow money vs the no risk rate that the government has to pay to borrow money. We mentioned that the spread was remarkably low. This is an important indicator of the credit market – which tends to lead the stock market – and things looked surprisingly good. However, over the last few weeks the strength of junk bonds has deteriorated and not so in treasuries. So, the spread between the two is stretching out to the point we are taking notice. Here’s a visual of that “spread” over the last few years.

Again, this spread shows when credit markets are getting nervous about the future economic strength, and we are seeing some concerns. This high yield/treasury spread was higher in late 2018 but not much. This returns us to the question of what the Federal Reserve will do in the near future. Market participants are predicting another .50% hike in short term rates by the Fed at their meeting in June. But some economic numbers are coming in much lower than just a few months ago. New home sales and permits to start have come WAY down. Employment data has dropped quite dramatically according to recent surveys. Big box retailers (think Walmart) have had a CRAZY whipsaw in inventory to sales ratios. One year ago, there was very little inventory and good sales after retailers were coming out of COVID lockdowns. Now we have had a rocket launch in inventories and a decline in sales. Consequently, shipping rates are dropping quickly. Is this a DEFLATIONARY force exerting itself? Will the Fed look at new data between here and June and maybe reconsidering its aggressive hike plan? Have the credit markets priced in the hike already and would firm up if the Fed did ease off its hiking? The Federal Reserve – even to their own admission – drastically overstimulated the credit markets and the economy. The Fed is backed into a corner trying to make sure credit markets and asset markets can be cooled off without being crushed. They now say that a soft landing as they are pulling back some of this stimulus may be beyond their control. Great…

The stock market has been down seven weeks in a row for the first time since 2001. Friday looks like at least a short-term bottom to us as things have gotten overly negative. We expect a relief rally. Going forward, we can only guess as to the actions of the Federal Reserve – so preparing an investment strategy based on what they will do is not a good idea. Of course, we hope the Fed doesn’t ignore economic data and blindly raise rates until something breaks – but we doubt they will DRASTICALLY change from their tightening schedule unless something does break. (a quick guess is that they only raise rates .25% in June, but we will see.) So, if the movement of markets is keeping you up at night, raise some cash on the relief rally adjusting your portfolio to less risk. But we have been saying that for weeks now https://www.sesweb.net/blog/canary-in-the-coal-mine

When credit markets show that they are on firmer footing we will have more confidence with risk on – but there will likely continue to be volatility.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | May 9, 2022

Fears of a global recession are abundant. Last week the Federal Reserve raised short term rates by .5% – more than any one move for more than two decades – and asset markets rocketed higher only to sell-off. Some market observers were saying the stock market would be at all-time highs within a few days and that the Fed would have to raise rates even faster. Then the market had the most aggressive sell-off since March 2020. There are no two ways about it – we are in a very wild macro-economic environment, and it is very hard to predict.

The slowdown in China is in plain sight. Major cities have been completely shut down and smaller cities are seeing a rise in Covid rates. The port of Shanghai has historic backlogs and one can only hope that the worst is behind us. But obviously with China it is very difficult to tell.

Europe is slowing down for sure also and the Russia-Ukraine conflict is of course, front and center. The European financial managers are trying to raise rates and return to more normal policies considering the surging inflation. However, the longer the conflict with Russia goes on, the worse the prospects for reasonable energy prices and the economy as a whole. The second half of the year is not looking good.

The economy in the U.S. has been the most consistent globally coming out of the Covid retraction although it did contract in Q1. Now the question is how flexible the Federal Reserve will be in its tightening campaign. Recent employment data was encouraging, however, surely some consumer spending numbers will reel in with the precipitous rise in food and energy. Throw on top of that the mortgage rates averaging more than 5% on a 30-year fixed rate for the first time in more than a decade and one has to think that the housing boom will cool off significantly. Without a doubt, risks of a recession are still rising – but only time will tell…

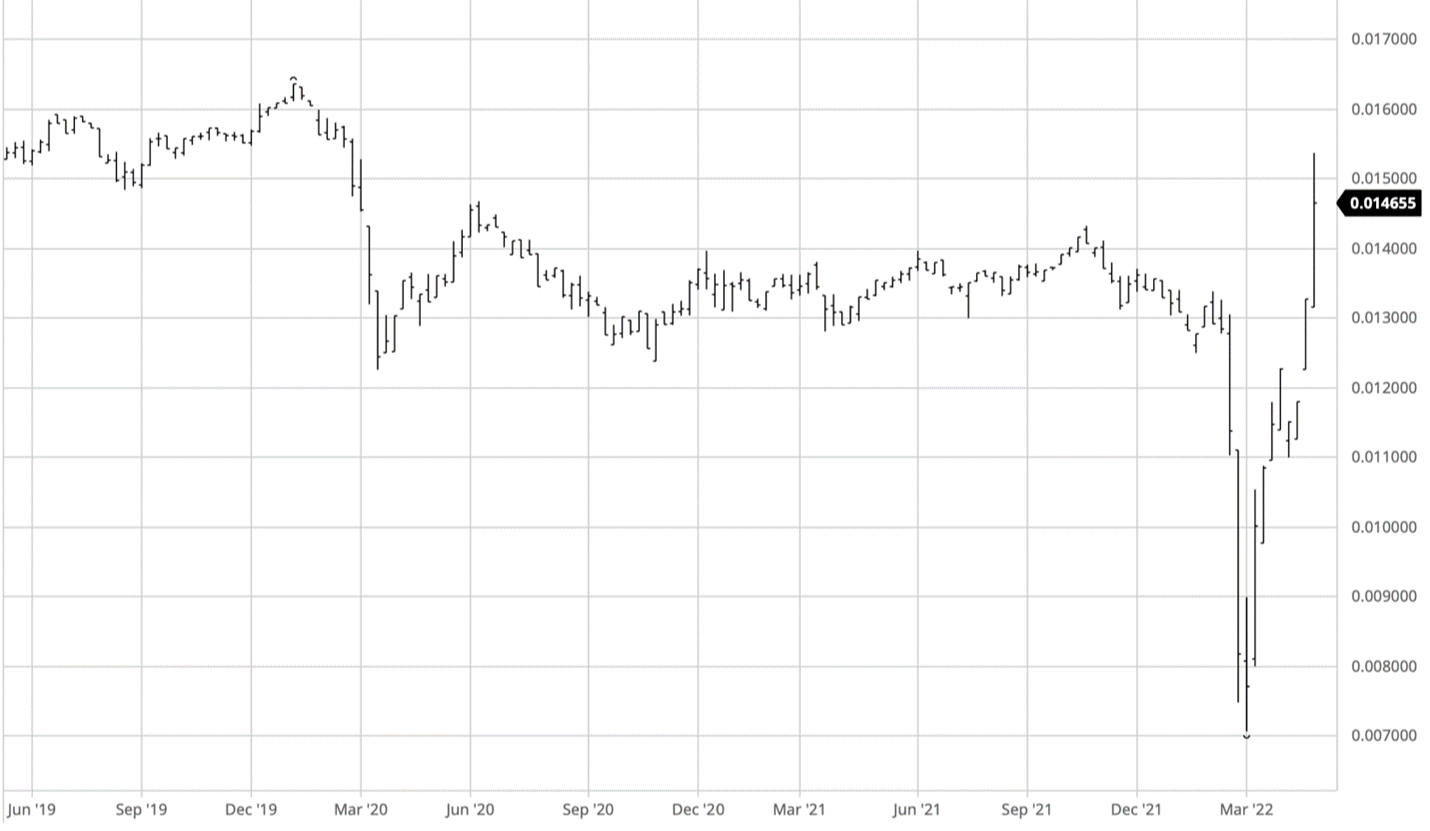

One thing we find quite curious in the financial world is the only two currencies that are higher vs the U.S. dollar in the last year. The Brazilian Real and the Russian Ruble. Whaaaaat? The Russian Ruble is higher vs. U.S. dollar over the last year? It is – take a look…

So, if the Russian economy is falling apart because of the sanctions after their aggression into Ukraine, how is this possible? The answer is complicated, but some of the rest of the world is buying rubles in order to purchase oil and gas. Going forward there is talk of the Russians having an internal currency system that is based on a basket of commodities. We aren’t sure how that is going to roll out yet, but stay tuned…

Regards and good investing,

Greyson Geiler

by Greyson Geiler | May 2, 2022

All eyes in the financial world will be on the Federal Reserve come Wednesday when the policy statement will be released. Expectations are for a .50% rise in short term rates and the announcement of the dates of the Fed’s contraction of its balance sheet. As we mentioned last week, the outlook of a scorching economy that the Fed needs to reign in precipitously with aggressive interest rate hikes is waning. Some economic numbers are even deteriorating to the point of bordering on recession. An example of that would be employment numbers tumbling to its weakest since Aug 2021. Strangely though, some manufacturing numbers were a pleasant surprise upward. The data from 1st quarter earnings from big companies was disappointing, but the 2nd quarter appears to be starting on firmer footing. At the end of the day, there is nothing obvious to say that the Fed should not raise rates, and of course the Fed has been banging hawkish drums for weeks now as they are responsible for much of the inflation that we now see. No matter what we feel of the wisdom of raising rates, we are betting that the Fed will raise rates and the only possibility we see is they may only raise .25% – but that is unlikely.

Once again, take a look at a chart of the price of the U.S. Dollar vs. a basket of other currencies…

That chart doesn’t make us think that inflation is going to run wild even after supply chain disruptions calm down. Like we mentioned last week: sesweb.net/blog/canary-in-the-coal-mine

Asset markets have priced in this rate rise – so now the question is, where do they go if the Fed does as expected and raises interest rates .50% on Wednesday? Here we are going to share an analysis from Goldman Sachs. Scott Rubner provides research for the top clients of Goldman and here is his 11-point checklist of why he thinks the worst of asset markets’ selloff is done for now…

- U.S. Corporates return back to the open window on Monday with dry powder. Rubner calculates $5BN of demand per day, every day until mid-June. U.S. corporates are the largest buyer of equities in 2022 and have authorized record YTD (AAPL = $90bn; GOOG = $70bn; MSFT = $60bn; FB = $50bn, etc).

- Pensions flipped to buy given the recent outperformance of bonds vs stock. This should carry over into next week.

- S&P Index gamma turned negative on Thursday for the first time since March.

- Synthetic Short Gamma through CTA and Vol-Control strategies supply will fade over the next week (Thursday’s move will lower some of the supply expectations and Goldman’s estimates will dramatically change next week).

- Liquidity is simply not available to try to cover liquid macro. As we noted on several occasions last week sesweb.net/blog/canary-in-the-coal-mine, top book liquidity in the S&P 500 futures is $2.8M. This ranks in the 1st percentile in the last 10-years. This is as low as it gets.

- Sentiment is the most bearish since the market crash lows in March 2009. Rubner says that he has done “more bearish zoom calls these past two weeks, than I can recall.” The bears (AAIIBEAR) published a reading of 59.40 today. This was the highest level since March 5th 2009 (70.27). S&P500 rallied 8.54% in March 2009 and 9.39% in April of 2009. That was the generational market bottom.

- Money Market Inflows Logged a massive +$60B inflows last week, which was the largest weekly inflow since Covid 2020 (and typically another fear gauge).

- For the fixed income watchers, Goldman’s CTA models show some impressive demand. Goldman has +$20B of bonds to buy in a flat tape, but +$117B of bonds to buy in an up tape, and $37B of bonds to buy in a down tape. This should ease some of the pressure on long duration equities and largest construction of market cap.

- Goldman’s Prime Desk notes that hedge funds exposure is dismal. Gross and Net Exposure are currently at 2-year lows. And vs the past 5 years, Gross ranks in the 21st and Net ranks in the 38th. US TMT Megacap L/S ratio declined by -48% in the past 1-month. (~right before earnings)

- Everyone is short: Short leverage (with options) ranks in the 98th percentile in the last 5 years.

- New month = New Inflows. There should be some decent inflows to start May per normal rebalancing cycle in retirement accounts.

There is a lot of trader-talk in that analysis but to put it simply, most everyone thinks the stock and bond markets are going down. Sentiment is at 5-year lows and volatility is high. GENERALLY that means – along with some of the other points Rubner puts together – that a relief rally at least is due. There are many, many challenges to the world’s asset markets as are all over the news wires. We aren’t suggesting that things can’t get worse. But we are suggesting that for now the bulk of the damage has been done. Invest accordingly!!

Regards and good investing,

Greyson Geiler

by Greyson Geiler | April 25, 2022

Predictions of monetary/economic doom are prevalent in the financial news media right now and as much as we complain about the actions of central bankers worldwide, it would be hypocritical of us to poo-poo those fears. The Federal Reserve alone poured trillions of $ of “liquidity” onto markets over decades but quite acutely since the advent of the Covid-19 “pandemic.” Asset markets have responded with a boom in prices. From real estate to stocks, bonds and commodities there have been sharp appreciations with some calling our present situation the “everything bubble.” Inflation fears and numbers in some respects have rocketed higher leaving many wondering why the FED had kept “emergency policies” in place so long including zero short term interest rates and asset purchases on the open market of $120 billion per month. Now the FED is going “hawkish” meaning they will tighten monetary policy and mop up some of this liquidity and it has engendered fears of bubbles popping and economic doom. We have said for years that of the world’s developed market central bankers, the Japanese were the worst offenders, and they should be watched as a canary in the coalmine so-to-speak. In other words, the game of adding and subtracting “liquidity” in the world’s monetary system as the central bankers see fit has never appeared to be good long term strategy to us. Japan might be a good indicator when that game may start to unravel.

The situation in Japan is one of a mountain of debt at ridiculously low interest rates. Total government debt is pushing 300% of GDP (remember, Japan is the third largest economy in the world,) but the central bank owns about half of it and some of it is still at a NEGATIVE interest rate. The interest paid by the Japanese government pencils out to be only about 1% of GDP. It’s an amazing trick if it stays intact. In the last couple weeks, however storm clouds are forming on the horizon. With interest rates rising worldwide, imagine being a Japanese bond investor. Inflation and bond yields are going up everywhere and you are holding Japanese Government Bonds that are yielding somewhere between almost nothing and less than nothing. Historically this actually made some sense because of the consistent deflation in Japan – but that is obviously not the case now. So, bond investors are nervous, and the Bank of Japan has had to publicize that it will backstop the 10-year JGBs at .25%. This means that they won’t let the price of the bonds go below what would represent a .25% yield. Of course, they must print more Yen to buy those bonds and backstop that price and here is where the dilemma presents itself. The value of the Yen is crumbling (20-year lows vs. the dollar) and the BOJ is realizing that it can’t do both; limit the interest rate rise on the 10 JGB and protect the value of the Yen.

Some Japanese investors are selling their bonds to the BOJ and buying U.S. treasuries (where the ten-year yield is more like 2.75%) in order to protect their purchasing power. If the U.S. Federal Reserve continues on its “hawkishness” and interest rates continue higher in the U.S., this could certainly be a catalyst to something breaking in Japan as more bond selling occurs and possibly domino into other parts of Asia. Remember, the futures markets are pricing in more than a 2% rise in short term interest rates in the U.S. – so something has to give. Will the Fed stick to its guns and keep raising rates to fight inflation and cool off the economy? It sure looks to us that the inflation fears are overdone and estimates of how many times the Fed will raise rates is DRASTICALLY overestimated. As of the writing of this post, the commodity board is blood red. Crude oil is getting smashed well back below $100 per barrel and gold and silver are trading below where they were when Russia invaded Ukraine. The stock market has sold off and BONDS have stabilized – even rallying back a bit. The U.S. dollar is MUCH firmer against a basket of foreign currencies over the last few weeks as well. Of course, we are referencing a very small window of time and a snapshot observation, but the markets really do not look like we have runaway inflation that the Fed is going to have to accelerate interest rate raises into. If the Fed does start accelerating short term interest rates higher, we will be even more worried about our little canary in the Japanese coal mine.

We have many earnings reports and economic data that will be coming out this week which could certainly move the markets. However, much of it will be backward looking rather than forward. Some of the more forward-looking indicators are not showing a robust economy. B of A’s weekly shipper survey “at near freight recession level” is one example and a big decline in existing home sales in the U.S. is another. This doesn’t indicate a big need for higher interest rates. Also – some of the causes of price spikes are clearly not a monetary phenomenon. Supply chain disruptions have been bad – and now in some cases may get worse with some of the lockdowns in China. A satellite image of the shipping vessels waiting to get into the port of Shanghai makes our recent Longbeach logjam look like a child’s play. This has caused shipping of some items to STOP and consequently, price rises will be inevitable. Raising interest rates will not solve this problem and will possibly create new problems to add to our stack. Don’t forget the Russians are still in Ukraine and there is new talk of sanctioning China. There may be other issues for the world economy that haven’t really manifested yet. Raise cash if you need to but hopefully your portfolio is balanced enough to endure some volatility – just remember we may have a lot more. We have many problems with the Federal Reserve and the monetary structure they are managing in general – but we are not in the camp that the Fed won’t pause if asset markets really start taking on water. We are buying the dip in the price of birdseed…

Regards and good investing,

Greyson Geiler