by Greyson Geiler | September 19, 2022

Financial markets had a rough week last week and there are indicators causing market participants to brace for another bad week coming up. Last week we talked about the inflation numbers that were to be released by the Department of Labor. The average trade guess was lower than the numbers turned out. Meaning the marketplace was anticipating inflation numbers to be calming down and that is not what happened. So now the market has to assume that the Federal Reserve will be obligated to continue raising interest rates to stave off inflation. Higher interest rates mean lower bond prices. Lower bond prices over time means lower stock prices. The stock market in general had a terrible week last week and all eyes are on the FED to see if they may actually move short term interest rates by a full 1.0% higher rather than the .75% that market observers have been assuming. So many have changed investment strategy to risk off.

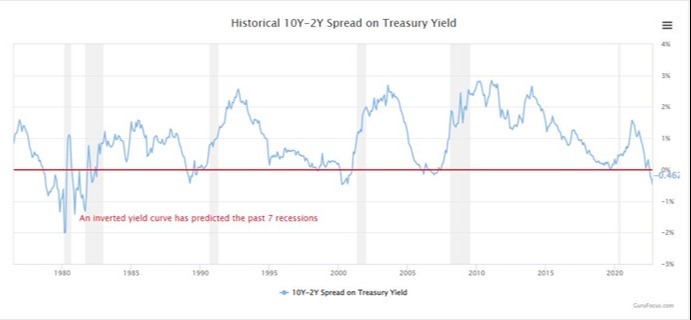

Now we have an inverted yield curve, and it looks like that is going to get much worse. Take a look at a historical chart of the 10-year interest rate minus the 2-year interest rate of treasuries…

This chart is courtesy of Gurufocus.com and it shows that the yield curve inversion is a pretty good historical indicator of recessions. Of course, the drastic inversion of the yield curve in 1981 that was orchestrated by Paul Volcker initiated a recession in the early 80s. That was Volcker’s response to reigning in the inflation of the late 1970’s. Inflation has been quite benign since then…until now.

This time around we have an order of magnitude more debt in existence which drastically magnifies the effects of higher interest rates. Again, the Federal Reserve kept emergency liquidity measures in place well after the conditions of the economy and markets warranted it. Now we are paying the price and they are going to raise rates further into an already inverted yield curve and a recession that is already in place. Some of the economic numbers – check FedEx recent guidance on their company performance – are starting to come down quite hard. That will get worse with the Fed continuing to hike rates.

The concept that with all of the world’s socio-economic problems existing today, the Fed can cure inflation simply by raising interest rates is quite naïve. One of the issues that we are facing right now is a supply side problem whether we are referring to gas, semiconductors, wheat, automobiles, housing or other things. Clearly the blunt instrument of higher interest rates will deter investment in new production and make the situation worse.

On the demand side of the equation, the Fed is getting its way by initiating a recession. This will stamp down on inflation and hopefully the higher interest rate game doesn’t keep going until something breaks. Our guess is that The Fed will have to pivot to a softer monetary strategy in short order to avoid a true detonation of the debt bubble. However, in the meantime, tighten the belt and reel in some risk if your portfolio is stressing you out.

Regards and good investing…

Greyson Geiler

by Greyson Geiler | September 12, 2022

The energy situation plaguing Europe right now is no surprise to anyone as it has been front page news for months now being associated with the Russian invasion of Ukraine. From 20,000 feet, the reality of the situation is that Europe on a broad scale depends on Russia for about 40% of its total energy needs. That energy has been cut off and there is not any smooth transition to alternative sources. This winter is going to be difficult for Europe – the only question is how bad will it get? European leaders seem oddly indifferent to the obvious coming challenges and blaming Putin is about as far as most discussions get. We don’t see many efforts for solutions and some of the green advocates are pleased by the dysfunctionality of the European energy markets. We have seen reports of Germans out in the woods cutting down trees for the coming winter. The only good news there is that at least something is being done…

Now we have to ask the question of the fallout from Europe to the U.S. if the situation gets really bad overseas. Will America feel the brunt of the European energy crisis? The quick answer to that is no one knows for sure. When you look at the situation in Europe, you have to understand that the energy issue -being at the core of the economy – could have repercussions not yet accounted for – and things could get crazy with rolling blackouts, economic shutdowns, food shortages, price controls, and even freezing and starvation. We are not being alarmists and predicting these things, but the conditions are in the pot and again, considering the interdependency of the worlds’ economy, one has to consider the potential destabilization of the U.S. economy.

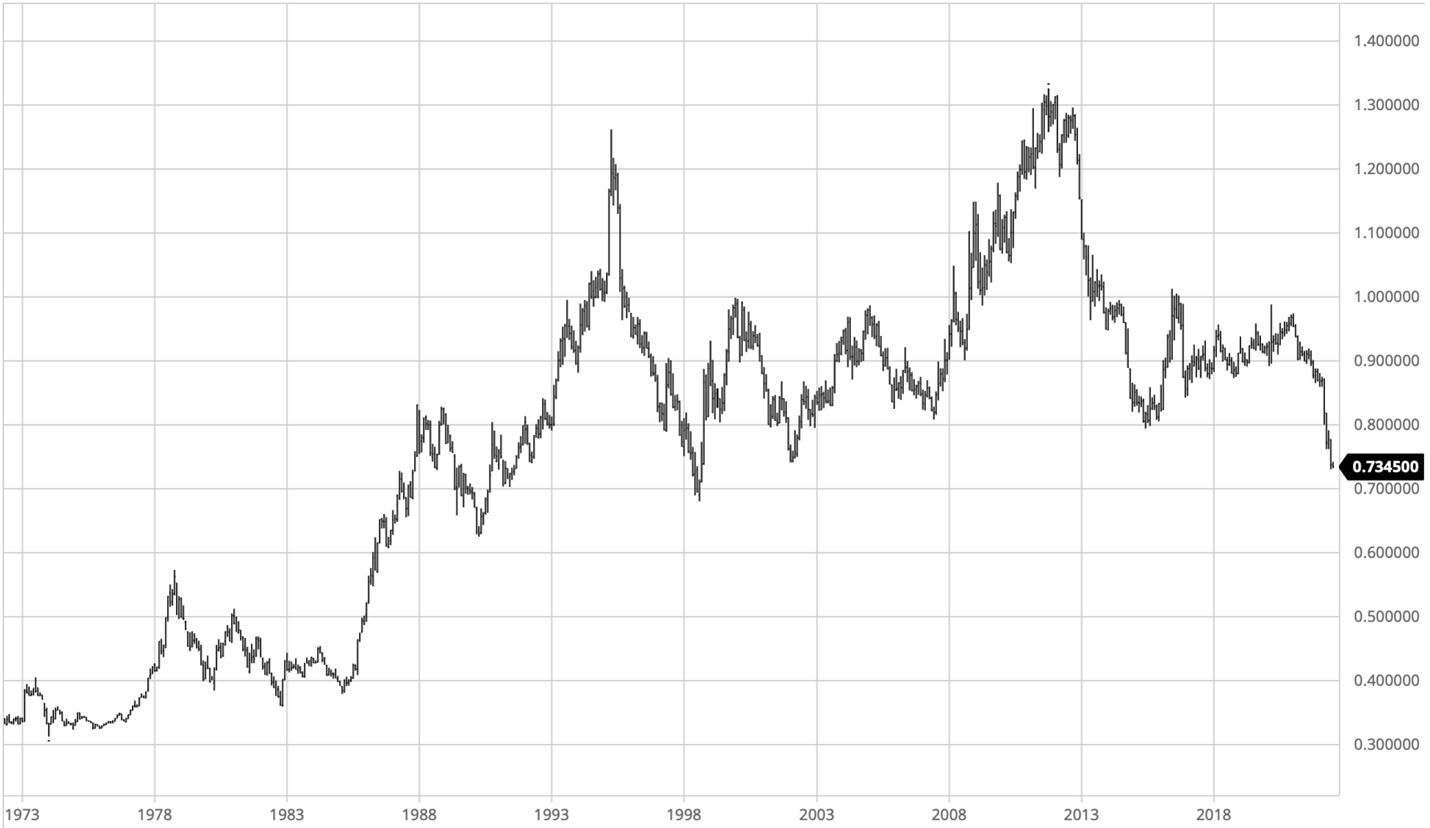

We are always looking at the financial markets for clues of how the fundamentals of the world’s economy are moving along. Of course, one indicator that we have frequently referenced is the weakness of the Japanese Yen on the currency stage. That will continue to be a concern of ours because it could cause big disruptions to the world’s money flows. Along that same vein, this week we take a look at the Euro vs the U.S. Dollar…

The Euro has been in the news recently because, as you can see on this chart, it traded at a discount to the U.S. Dollar for the first time in more than a decade. Of course, some of the systemic concerns that we listed above are what is driving the Euro to its recent weakness. We have always thought that the fundamental structure of the Euro was on a faulty foundation and recent weakness is a concern and supportive of our analysis. However, we do not see imminent doom in this chart or corresponding fundamental data coming out of Europe. Obviously, this could change quickly – especially if an early wave of cold air out of the Arctic highlight’s European energy challenges – but for now financial markets are holding together surprisingly well.

On the domestic front, crude oil has come down in price below $90 per barrel which has been a pleasant surprise. Our financial markets are boosted by foreign assets coming to our shores and the major stock indices are showing remarkable resilience. Coming up this week we have the inflation numbers out of the DOL. The average trade guess is about 8% so inflation is clearly coming down and the labor numbers which are of upmost concern when considering inflation are softening without a doubt. How the FED will manage getting the inflation genie back into the bottle and within their 2% target remains to be seen. The good news is that weaker economic numbers have caused pressure to come off of our asset markets. But let’s be careful betting on “bad news is good news” on the economic front. Our fears are that some of the inflation numbers coming down is due more to demand destruction rather than supply increasing. Clearly that is not very positive going forward. What that means on the investing front is we feel that this is a good opportunity to readjust portfolios if you feel you have had too much risk. Again, much of the pressure has come off of asset markets and we agree with raising cash by selling assets for investors that may have needs for funds in the near to medium term. The challenges in Europe do have the potential to escalate and spill over to the U.S. – so we need to prepare accordingly.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | August 15, 2022

A common theme in our weekly posts is haranguing about the financial profligacy of our monetary authorities – the Federal Reserve – and from time to time we will extend some extra criticism of the Bank of Japan. This week we are extending our focus out to the situation in the European Union.

Periodic debt meltdowns/write-offs/jubilees – whatever you would like to call it have been a part of civilization since records began. The Old Testament has stories of rulers emancipating slaves, debtors and indentured servants. Historically it was commonplace and from a practical perspective it was probably necessary for rulers to keep stability in their societies. Some societies even developed cyclical timetables when debts would be alleviated…

In modern times we have no shortage of examples of debts going bad and some of the repeat offenders are almost comical. Our favorite example – since its liberation from Spain in the early 1800s, Argentina has defaulted on (or restructured) its debt NINE TIMES!! The most ridiculous part was in 2017 – after eight of the nine defaults – the Argentinian government sold a ONE HUNDRED YEAR BOND (about $10 billion worth) and it was over-subscribed which means that there was more money chasing the issue than there were bonds offered. The interest rate went off at about 7%. The investing world was starving for yield, and they took a leap of faith – and they have already paid the price. The bonds are now being restructured and valuations have been cut in half. Not a shocker…

For a now third-world debt issuance like Argentina, reasonable people can agree that it needs to be buyer beware – I couldn’t believe that they had actually pulled it off!

But when we get to Western Europe and the United States, we are talking about the world’s reserve currencies and one would hope that there is a very, very low risk of default or restructuring. The monetary system of the world is obviously built off the U.S. dollar. However, according to the IMF, after nearly 60% held in U.S. $, more than 20% of the holdings of the world’s central banks are denominated in Euros. Many other countries are fighting it out for a very distant third place at around 5%. Take a look…

Sadly, the debt situation in Europe today is FAR WORSE than it was in 2012 when there was an actual debt crisis. Case in point are Greece and Italy. In 2012 they were at the epicenter of an international financial meltdown as bad debt was teetering over the edge of the abyss and beginning to look like a “Minsky Moment” (no time to explain, we have to ask you to look that one up.) In 2012, Greece had a sovereign debt at about 150% of their GDP and Italy was about 126%. Fast forward to post-Covid-crisis 2022 and those numbers are more like 235% for Greece and 175% for Italy!! So, if the 2012 numbers were enough to ignite a crisis, how did we get so much further down the road of indebtedness without a complete Armageddon? We will oversimplify the answer and we will say it is the European Central Banks. The profligate governments of Greece and Italy (and others) have clearly been issuing bonds at a blistering pace – and the only buyer during Covid has been the ECB. Interest rates have been managed and the interest rate on Greek debt versus the European standard German debt hasn’t really been that different (2.29% on a 10-year note.) The ECB has amassed a mountain of member-country debts and they claim they are going to pull their bids. The million-dollar question is how do Greece and Italy sell their bonds now in a world-wide rising interest rate environment? The ECB is going to be forced into a very similar situation that we have described the Bank of Japan to be in. They can support the price of bonds (and keep interest rates down) or they can protect the value of their currency – but not both. If we aggregate Spain and Portugal into this analysis, the numbers get worse, and the entire Eurozone has government debt alone that aggregates to 100% of Eurozone GDP. Good economic history work from Reinhart and Rogoff shows that 90% of debt to GDP ratio is where things started to break down historically. That means that we should have expected restructuring on some of the world’s debt some ten years ago… and BTW – Interest rates are rising.

We don’t have time to go into the many facets of the European structure that render it less resilient than America from a political and more importantly monetary standpoint. For this post, just trust that we are reasonably accurate with that. Going forward, in the developed world it feels that Japan and Europe are in a race to the bottom – the price of their currencies relative to the U.S. $ on world markets will be the de facto color commentator on how the race is going. Race to the bottom means that they will keep printing money, ignoring economic reality and kicking the can down the road until a true meltdown occurs. China – with their Olympus Mons of debt – is the dark horse of this race…

Capital is flocking to America from overseas at a steady pace. We believe that that trend will STRENGTHEN rather than abate – so this is not a doomsday post from an American perspective – but we will still tell you to not sell your gold. If you don’t own any, buy some.

Life for the bottom 50% of the world has gotten better at a pace over the last 20 years so ridiculous that we can’t even find enough superlatives for it. But the story is different for a lot of the developed world largely because of unrealistic lifestyles financed by credit and exacerbated by absurd government spending policies.

It is sad that in our continued analysis of the world’s economy, we liken the US situation to being the prettiest girl in the leper colony – but that’s really what we see.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | July 11, 2022

Contrary to popular belief the U.S. dollar is not losing its world reserve currency status. The demise of the U.S. dollar has been a popular in the financial media for more than a decade. That is understandable considering the creation of so many currency units over so many years. Indeed, complaining about the profligacy of the Federal Reserve is a consistent theme in our weekly posts.

The world is awash of paper currencies and bad debts – a situation that won’t end well. But for as critical as we have been about the Federal Reserve, we have said consistently that the Bank of Japan is the worst performer of the currency printing game. We have declared the Japanese Yen as the “canary in the coalmine” – essentially an indicator that the game of attempting to print wealth out of thin air may be on thin ice.

Well, the proverbial canary isn’t looking so robust. Look at a long-term chart of the Japanese Yen…

The Japanese Yen is knocking up against 25-year lows against the U.S. Dollar and the Euro and the British Pound are in a similar situation. At least some of it makes sense – The 10-year interest rate on Japanese government bonds is .25%. In the U.S., the ten-year rate on government bonds is 3.1%. Obviously, those with the wherewithal to invest in both would prefer the US bonds. The Bank of Japan is setting the price of their 10 year bond and they are buying from existing investors – and they are buying a lot of bonds. The BOJ now owns some 542 trillion Yen ($3.95 T) worth of Japanese government bonds which now comprises more than 50% of the total JGBs outstanding – which is about $8 trillion total. The sellers of all of these bonds end up with a pile of Yen and those are becoming a bit of a hot potato internationally (as evidenced by the above chart.) At the end of the day, the Japanese central bank will be able to defend the price of the bonds or the value of the Yen – but not both. Tensions are running high, and some observers wonder if the $1.3 trillion in U.S. government bonds that the BOJ owns may start getting sold off to defend the price of the Yen. The situation is getting pretty dire, and we expect there may be unintended consequences of whatever the BOJ does as they have really boxed themselves into a corner. Stay tuned.

Back home our U.S. financial markets are clearly getting supported by foreign capital coming to our shores as a safe haven. The dollar has rocketed higher vs. other currencies and alternative assets of cryptocurrencies and even gold have taken it on the chin. The fact that our asset markets are holding together very well – at least for now – is quite impressive. Past the short term, however we don’t have confidence that the higher interest rates we are seeing now will be sustainable.

Multinational corporate earnings will be adversely affected by the stronger dollar and some of the economic reports in the U.S. have drastically cooled from just a few months back. Drastically higher interest rates in the mortgage world have put the skids on the housing market boom. Higher corporate bond rates are putting the skids on stock repurchases among other things.

This is while the Fed is trying to reduce its balance sheet of nearly $9 trillion in assets. Although the Fed’s balance sheet total has barely been reduced since their highest holdings in April, there will be a negative effect on asset markets going forward if the reduction continues. The U.S. dollar is the oil that greases the wheels of the entire world’s economy, and those wheels may start squeaking very loudly in short order. For now, our markets are holding together quite well with the Fed tightening things up a bit. Of course, that may not continue, and we do believe there will be volatility continuing forward. As always, the wildcard is the timing of the Fed loosening monetary policy to stave of adversity – it’s one thing they do know how to do.

Regards and good investing!

by Greyson Geiler | June 13, 2022

Predicting the future price movement of actively traded commodity, bond, stock markets – really any market for that matter – can be very difficult endeavor. Indeed, sometimes it borders on a fool’s errand. However, focusing on something we do know – we have maintained for a very long time that our Federal Reserve along with other central banks around the world have had the habit of maintaining interest rates consistently too low. One of the reasons this is bad is because in general, when interest rates are artificially low, too much bad debt is created and worse yet – underlying currencies become devalued. Some of our worst fears appear to be looming on the horizon from this perspective with dangerous looks from inflation numbers. The short answer is we don’t know how high interest rates are going. Running a fiat currency system is a difficult prospect – so let’s take a look at some of the workings behind the scenes that may help us understand more of what’s going on in our capital markets…

When you are in charge of a debt based monetary system like the one we have, a very important consideration is how much demand you have for your currency. Remember ALL of our money originates from debt – our money is borrowed into existence. If everyone in the world paid off all of their debt – there would be no money. Sit with that for a while…Even the cash in your pocket is on the debit side of the Federal Reserve’s balance sheet – the Fed essentially owes you something for the cash you have. CASH IS A DEBT INSTRUMENT TOO! So, intuitively when interest rates are low, it is easier for borrowers to take on debt therefore much more is created. More debt is taken on by governments, businesses, individuals – essentially everyone will take on more debt with low interest rates because the payments to service the debt are lower.

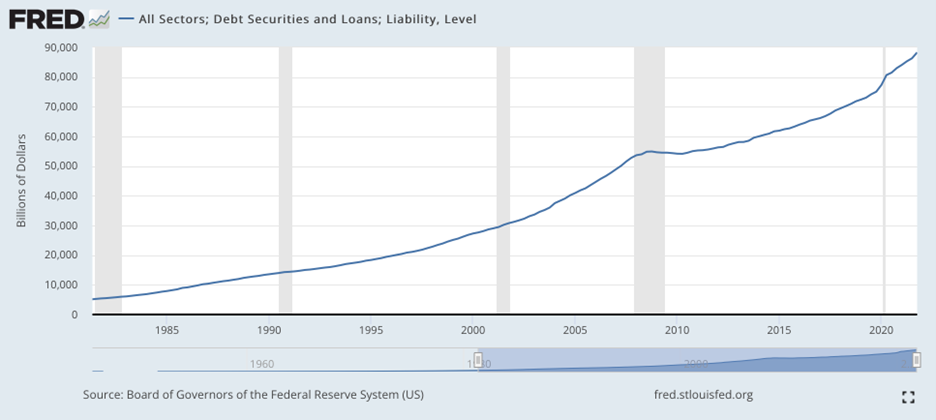

Interest rates have been coming down since the early 1980’s and the total debt outstanding – government, corporate and personal – embarked on quite a rocket launch. Take a look…

Yes, you are reading that correctly – total debt was about $5 trillion in 1980 and after 40 years of declining interest rates we are almost to $90 trillion. As bad as that may seem – and as dangerous in a rising interest rate environment as it is – it isn’t all bad. Back to our previous point, an important part of a currency maintaining is value is demand for said currency. Well with all of that debt out there, someone needs to acquire dollars to pay for the debt service.

Counterintuitively, continually lowering interest rates can have a deflationary effect as people have to pay debt back– just check out the last 30 years in Japan. The creation of the debt can be inflationary (that is supplying new money)– the servicing of the debt can be deflationary as there is a demand for money to make interest payments and those payments aren’t being used to consume.

But what does that have to do with our present situation and answering the question of how high interest rates can go? A big part of the answer to that question is loan demand. Because of the higher interest rates business loan and mortgage loan demand has fallen off of a cliff. The Fed doesn’t need to panic raise interest rates to stave off new money supply (loans created– that has already happened). As far as the deflationary effect of servicing debt – that is firmly in place too. Part of the boom in debt that you see on the chart above is a function of old debts being refinanced (instead of being paid off) at lower interest rates – accelerating the boom.

Now with interest rates higher already than they have been in a decade, borrowers will have to pay off debt – a deflationary force. Then we get to the nasty part about debt default and that is another deflationary force (if it happens in the private sector.) As we have said in this post many times there is a lot of bad debt in our system and if it starts defaulting it could cascade into a serious deflationary environment. In our view, from here the financial markets can’t handle much higher interest rates because as addicted as we have become to low rates, removing them would create serious withdrawal – something will soon break…

The inflation numbers that came out last Friday were a big shock to the whole system. Expectations were for May inflation numbers to be subsiding but in reality, it came in at 8.6% – the highest year over year number in 40 years! So now the Fed is in a conundrum and the financial markets know it. We don’t believe that combating inflation simply comes down to the Fed raising interest rates. We have always had a problem with one entity setting the cost of money (interest rates) for the entire globe. Now the complexity of the system illustrates exactly why. Many things going on right now only get worse with the Fed aggressively raising rates but we fear that is exactly what they will do.

Here are some inflationary forces in our world right now that raising interest rates will not fix:

- First and foremost – of course – the price of oil and natural gas. When you look into details of Friday’s CPI numbers, energy is BY FAR the biggest problem. This is partially because of Russian sanctions – but also many Western Governments are forcing green energy legislation before a viable supply has been created. Plus, research and development in the oil and gas space has been put on hold as no one wants to commit capital in a space the government has its boot on the throat of. Speculators know this and crude oil-based investments have been bid up in financial markets as a “safe haven” and are essentially the only asset class that hasn’t sold off in recent months. This is creating a “perfect storm” of higher prices in the energy world.

- Food costs – much of the production of food is dependent on energy prices as is its distribution. On top of that, natural gas and potash are key ingredients to fertilizer of which Russia is one of the world’s largest suppliers. Raising interest rates will not grow more food.

- Lockdowns in China due to Covid bottling up production and distribution of many consumer goods. We have no control over when these forces subside.

- Supply chain breakdowns due to many different factors including government intervention of varying types and, of course, energy costs. Raising interest rates will only make this worse.

- Low labor market participation rates due to a complex combination of issues including unintended consequences of government Covid intervention.

- Frightened consumers have bid up some consumables to avoid scarcities if socio-economic conditions worsen.

- Being a landlord is a difficult endeavor in benign economic times. Not only are economic times not benign now, but in recent years governments including federal, state, county and municipal have drastically complicated issues. Thru its post Covid asset purchases, the Fed spurred a wild boom in real estate prices that flowed through to higher rent prices. Now mortgage applications have fallen off a cliff, and mortgage-backed securities traders observe that this last Friday was the worst day in mortgages since 2008. Not good. The single-family home and rental real estate market has hit a wall and the only thing higher interest rates would do now is additionally limit the ability of homebuilders to create new supply that has been hampered for decades by government regulation.

World-renowned economist Milton Friedman famously said that inflation is everywhere and always a monetary phenomenon. If that were true, the Fed should aggressively continue to raise interest rates because inflation is running hot. However, we respectfully disagree with Dr. Friedman. Monetary (and fiscal) policy has been wildly too loose for a very long time -that is true – but right now we feel that government intervention is a bigger problem. The yield curve is already inverted – 5-year yields are higher than 10-year yields – and the economic slowdown is ALREADY HERE. We fear that the Fed aggressively raising interest rates into this (and continuing the runoff of their overly inflated balance sheet) will break something. If something in financial markets does break, the Fed has proven in the past that they will quickly change course and pour more easy credit on the game. Wash, rinse, repeat.

To return to the original question of how high will interest rates go – we would be surprised if they go much higher at all than they are today on the longer end of the curve- 10 year. The Fed is meeting this week and will certainly raise short term rates. That is already priced into all asset markets. Thoughts are that they may raise .75% or 1.0% in response to Friday’s inflation numbers. That may not be priced in and if the Fed does raise that much we may see more selling of already depressed asset markets. One sliver of good news we can report is that the U.S. dollar is not depreciating vs other currencies! But volatility in financial markets is becoming the norm.

Stay tuned…