by Greyson Geiler | December 22, 2020

A consistent theme in our weekly post has been a concern over potential weakness in the U.S. Dollar. This anxiety is largely due to the performance of the Federal Reserve which has been dismal for decades. They have simply provided more dollars whenever economic conditions worsen – and they have not sufficiently pulled the reigns back when the economy has done well. Often times they tell the public one thing and have conversations with financial institutions that paint a different picture. They continually couch this irresponsible duplicity in fancy monetary jargon – but the end result will be a mess of inflation and monetary confusion. Now the dollar is near the lows of the last several years. Take a look…

The dollar index that is being measured here is a calculation of the value of the U.S. Dollar vs. other currencies of the world. The index is very over weighted against the Euro, however and the chart you are looking at is using a currency mix of nearly 60% Euro. The Yen, British Pound Canadian Dollar and other currencies collectively make up the remainder. Obviously, the spike higher in February and March was a run to the “safety” of the U.S. Dollar. We have had quite a move in the opposite direction and this needs to stay on our radar.

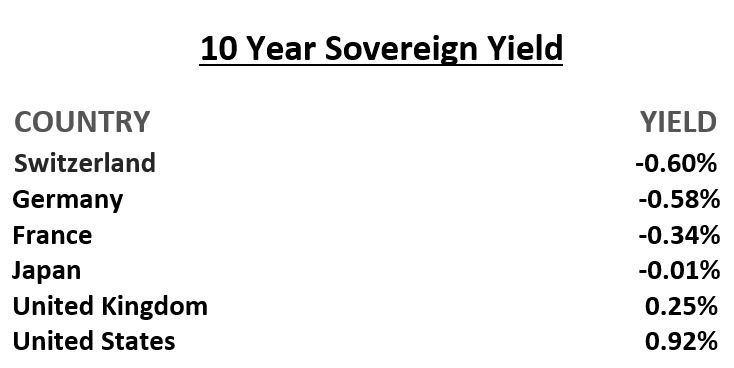

Determining the future of currency valuations is notoriously difficult. It involves many different factors and on the fundamental side those factors include capital flows, trade and investment flows, interest rates, relative growth and inflation. Focusing in on just one of those factors, interest rates, it seems quite an anomaly that the Euro is rocketing vs. the U.S. dollar when ten-year interest rates are negative over much of the Euro.

Even though interest rates are so much stronger in the U.S., many expect the dollar weakness to continue. Many believe that the world is over-invested in the U.S. and as the vaccinations improve business conditions worldwide the over emphasis on America will unwind. That theoretically, could bolster the current selloff in the dollar. In the meantime, in the European Union, their central bank continues to “Mediterraneanize” the currency. This means that austerity is out the window and the ECB continues to pump more Euros into the system (an additional 500 billion just last week.) We have historically postulated that the Euro is a flawed currency by design and that it will be relegated to the dustbin of history before the U.S. Dollar is. Of course, that is conjecture, but we do think that the selloff in the dollar is overdone. We will be surprised if it makes a significant move lower from here – but we will keep it on the radar – if we are wrong, we worry that that could mean serious things for the U.S. economy.

That brings us to the alternatives to the dollar. Just like we suggested with the Euro, the rest of the world’s paper currencies are enduring a veritable blizzard of central bank money printing. In addition to printing money, central banks are meddling in markets from top to bottom. They are setting interest rates across the whole yield curve, choosing winners and losers in credit markets and now they are spewing talking points that they are going to save the environment and initiate social justice for the less fortunate in our world economies. Of course, the merits of such ambitions are irrelevant, for even if they were pure as the driven snow, they are not under the jurisdiction of the central bank and country treasury departments. The whole thing smells a bit of desperation on the part of monetary authorities and does not instill confidence in the long-term future of our world monetary systems. The worlds sovereign debt numbers are far worse than we have ever seen, and it has become quite obvious that the “marketplace” of bond investors and providers will never again set the rates of interest. This has fostered a ROCKETLAUNCH in the price of cryptocurrencies that you may or may not heard of. Bitcoin is the kingpin of the cryptos and many are postulating that the price of it could go to several hundred thousand dollars per bitcoin. While we do not expressly advocate cryptos, those with the wherewithal may want to dip a toe in the water. It seems to us that at very least the value of bitcoins may continue higher for a while simply because some of the most powerful money people on the planet have said it will be so. Past that we are rather cynical of the cryptos, but the marketplace knows more than we do, and it is saying that cryptos are here to stay.

Of course, there is the age-old alternative to paper currencies that is gold. Gold has had an interesting year in that it is more than 20% higher on the year, yet still almost 10% off it’s all-time high that it reached this summer. Our opinion of gold stays steady. Gold is not an investment; it is money and can be held as insurance against profligate governments. Everyone should own some. If you can get a yield on that gold, then it becomes an investment, and you can always buy gold mining companies for short term to medium term investments which we do encourage. Many other commodities have been left underproduced and underinvested in. If the world economy does reinvigorate in 2021 we will have some amazing rallies in commodities from agriculture to energy and everything in between. These rallies will be especially pronounced if the U.S. dollar continues lower.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | December 7, 2020

Worldwide stock and bond markets continue to defy gravity in the wake of a resurgence of the Corona virus. Economic numbers are mixed to weak and as government stimulus has waned in recent months – but the stock indexes are full steam ahead. Interest rates remain very low and mortgage rates are keeping bids under a rocketing residential real estate market. Markets are very optimistic about the vaccine possibilities for the first part of the year as well and appear to be ignoring any of the political turmoil that is still plaguing the headlines.

One of the developments of the last month that is concerning to us is the weakness of the U.S. dollar. Many of the pundits are attributing this to a removal of the risk premium that was built in to the dollar as the pandemic ravaged the globe. That doesn’t pass the smell test with us – first and foremost because the selloff has gone way further down than where the rally started – and the pandemic is still setting records. Also, the way stocks are rallying does not imply that people worldwide are pulling their assets back out of our markets. This dollar weakness hasn’t gotten to disaster levels by any stretch – but with our interest rates higher than much of the developed world the selloff is counterintuitive. This needs to stay on the radar…

One thing that concerns us about the rally in the stock market is the one-sidedness of the market. Meaning, money managers across the board are confident and bullish. It is very reminiscent of late 2018 when the bullish sentiment was extremely high as well. We are certainly not predicting the Christmas meltdown in the markets that we had that year, but there are parallels that raise concern. One thing that is even more extreme now is that the volatility- trading hedge funds have pared back their short positions to effectively an all-time low. This is by some measures as collectively bullish as an investing community as we ever have ever been…

That certainly doesn’t mean that the market is going to sell off tomorrow, but it does make you wonder how smart it is to pile a bunch of new money into the market from this level. One thing that many of the investors with heavy stock overweighing their portfolios are reiterating right now is the backstop of central bank asset buying they expect to protect their downside risk. In fact, asset managers all over the globe have taken this from the don’t-ask-don’t-tell expectation behind the scenes (probably originated as “The Greenspan put from 1987”,) to a verbally stated rationalization. Valentijn van Nieuwenhuijzen, who helps to manage NN IP’s 295 billion euros ($356.09 billion) of assets, told Reuters Global Investment Outlook Summit, 2021 “Central banks will be super committed,” he said. “With massive output gaps, I doubt that over a 3-5 year horizon there will be any change in the picture of debt levels or inflation.”

Courtesy of Morgan Stanley we see a chart of the expectations of the balance sheets of the major world central banks going forward. We will be surprised if by Dec-22 their position isn’t MUCH larger…

We are not the only ones that can see the over extension of near-term bullishness, but most expecting a pullback consider it a buying opportunity. Morgan Stanley and JPMorgan’s advice is to mind the sharp imminent correction but to promptly buy the dip, i.e., “any equity correction in the near term would represent a buying opportunity as in our opinion we are only in the middle of the current bull market.”

The trend is your friend and at this point the trend is toward a Santa Claus rally. But much of this rally is on the central bank policies on the front end and expectations of a central bank safety net if anything goes wrong. Keep in mind, our fearless leaders in Washington DC are negotiating dumping another $1 trillion or so in “stimulus” when the market is pinned to an all-time high. These highs could certainly get higher. That seems like fiscal madness from a historical perspective, but so many of the historical measuring sticks of asset valuation are relatively useless with so much government/central bank meddling in asset markets. As Mark Twain so famously said – history doesn’t repeat but it often rhymes. Don’t expect this time to be exactly the same as historical bubbles – but also don’t think the piper will never have to be paid.

Regards and good investing!

Greyson Geiler

by Greyson Geiler | November 23, 2020

We have the Thanksgiving holiday this week and many market observers seem ready for the break. We have seen such outrageous political headlines for quite some time now, that we are certainly not the only investors tired of reading that the world political/economic situation is in “uncharted waters.” Even world leaders are checking out for the near term – this is courtesy of Michael Every from Rabobank…

For example, we just had the virtual G-20 “held” in Saudi Arabia…and did anyone actually notice? Even media like Bloomberg, which would bleed G-20 if punctured, notes ‘One of the starkest moments…came when U.S. President Donald Trump skipped a session on the pandemic to hit the golf course. Just as telling was how many other leaders seem checked out.’ Putin arrived late, Spanish and French leaders were caught looking at their phones, and Boris Johnson looked ‘uncombed and reading from his notes’. Indeed, while ’many leaders are relieved to have Joe Biden take over as U.S. president… they think four years of ”America First” cannot be easily undone, according to officials present.”

Specifically, to the markets, we are now seeing management shops like Morgan Stanley doubting the rally in stocks. The bank’s chief U.S. equity strategist Michael Wilson – is bullish over the next 12 months seeing a 10% increase in the broader market, yet bearish into year end, expecting another corrective “drawdown” in the S&P500. Some other things are emerging that are of concern for the near term in stocks as well. We are seeing some worrying signs in the credit world. According to credit-ratings agency Standard & Poor’s (“S&P”), 129 U.S. companies have defaulted on their debt so far this year… the most since 192 defaulted in 2009. On top of that, so far this year S&P has downgraded the credit of more than 2,100 companies, including more than 1,000 in the second quarter. That is already more than any year on record. This tells us clearly that we’ll see many more defaults in the months ahead. Today, the default rate for U.S. corporations is around 6% – up from 3% at the start of the year. It is clear that this number is headed higher when you look at the “weakest links.“ Weakest links are companies with already-poor credit ratings (“B-” or lower) that are on negative credit watches or with negative credit outlooks from S&P. The number of weakest links in the U.S. IS NOW MORE THAN 400 COMPANIES!! That’s nearly double the 235 weakest links in March 2009 during the last financial crisis and the default rate for the weakest-link companies is around five times higher than the overall default rate. S&P forecasts that the high-yield default rate will rise to 12.5% by June 2021. That would be the highest default rate since the Great Depression in 1932. S&P’s current “pessimistic” forecast projects the default rate to reach 15.5%. A 12.5% default rate means another 240 companies will go bankrupt over the next year. A 15.5% rate means more than 300 companies will go under – which is obviously a staggering number. When you look at how big the corporate debt pile has gotten over the last few years – the discussion has different context.

Of course, the situation looks dire – like we are going to be walking into big problems with corporate debt. But the variable that we can’t quantify in this equation is what the Federal Reserve will do. They backstopped a lot of corporate debt after the “pandemic” hit. The FED has already purchased a lot of corporate bond ETFs and it has the capacity to buy some $250 billion more. We find it hard to believe that the FED would back away and leave these debt markets to themselves if panic started to hit. Obviously if that did happen there would be enormous damage to the bond and stock markets. So, for now, investors seem content with the idea that the FED has their back. We will keep the sketchy corporate bonds on our radar and continue to evaluate.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | November 16, 2020

Pfizer has hit the headlines over the last two weeks with news of a vaccine for the corona virus. The effectiveness of the vaccine for the “general population” appears to be 90-95% which is a grand-slam home run. Intuitively this will relieve many of the fears of a resurgence of the “pandemic” now that North America is heading toward winter. The stock market has responded accordingly by heading toward new highs on confidence that economic shutdown will not be “necessary.” Interestingly, long term interest rates are slightly higher in the last few weeks which at least indicates that the economy is finding its legs after the shutdowns. To that point, consider this: earnings season is nearly over, with around 90% of the S&P 500 companies having reported now. Around 84% have reported a positive surprise on earnings and 72% have reported a positive surprise on sales. Of course, we have to take this with a grain of salt, because Wall Street has developed a game of lowering expectations in front of a report so you can claim you beat said expectations. But there still is a surprising resilience in the American economy that outperforms – especially Europe- much of the rest of the world right now.

The presidential election, reminiscent of 2000 Bush vs Gore, hasn’t been settled yet and we don’t know when that will be resolved. Of course, who is in the White House will have some effect on specific portions of the markets we watch every day and speculation on that makes tabloid publications tick. However, in the grand scheme of things historically, whether the White House is occupied by a Republican or Democrat has ALMOST NO EFFECT on the overall trend of the markets. Speculation on the social effects (rioting, violence, boycotts etc.) of Trump or Biden winning is exactly that at this point – speculation.

This week is full of economic news and on the central bank front, we’ll hear from a number of speakers including ECB President Lagarde, Bank of England Governor Bailey and Fed Vice Chair Clarida. The main policy decisions will be coming from emerging markets, however, including the Central Bank of Turkey, the South African Reserve Bank and Bank Indonesia, who are all announcing their decisions on Thursday. We are not sure if these will be large decisions – but Thursday is definitely on our radar.

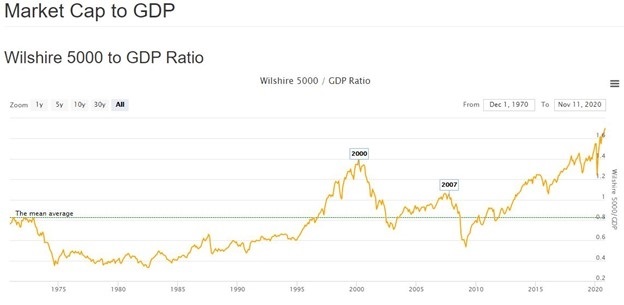

With the support of the Federal Reserve asset markets as defined by stocks, bonds and real estate have defied gravity through the “pandemic” of Covid-19. As we stated above, the economy is performing remarkably well, all things considered. But the market is waaay overbought by historical measures. Take a look at the “Buffet Indicator” which measures the total value of the stock market in comparison to the total GDP of the economy…

This shows a market richly priced even in comparison to the bubbles of 2000 and 2007. Keep in mind, however that overbought markets can continue to get more overbought. We don’t see that the Federal Reserve will back away and stop buying assets or raise interest rates which could halt this overvaluation of assets. But understand that the “rubber band” is getting stretched and there needs to be some sort of reset – when and how that comes to pass is anyone’s guess. But with all of the uncertainty on everyone’s front burner right now, the fact that things are more than holding together gives us some confidence that rallies will continue. Things that could change the investing landscape are, of course wild changes in the election results or central bank decisions – so STAY TUNED!!!

Regards and good investing,

Greyson Geiler

by Greyson Geiler | November 2, 2020

Of course, the election is first and foremost on the minds of most Americans and especially investors. However, the coming week will be much more than just the election. It is a “huge week” for investors with a Fed decision, 128 companies in the S&P reporting earnings, October payrolls, ongoing pandemic lockdowns, and a much more economic data as well.

As we have written with regard to the election, there is no consensus this time around whether a Trump or Biden victory would be better for the financial markets. However, if there is a “blue wave” meaning a Biden Presidency and Democrats getting a majority in the Senate, most observers agree that would be bullish for stocks. The reasoning behind this is an expectation that there would be little resistance to new stimulus measures. Over 90 million have already voted which is 67.7% of 2016’s total and it doesn’t appear to us that there is an obvious outcome. We said a couple weeks ago that the financial world seemed pretty calm which looked like the market, if nothing else, was confident that the winner would be declared on Nov 3rd. Now that appears to be off the table with an aggressive selloff in stocks last week. So now it doesn’t look like anyone really knows what is going to happen.

Later this week, on Thursday, both the Federal Reserve and the Bank of England will be announcing their latest monetary policy decisions. Starting with the Fed, the central bank is expected to remain in a holding pattern this meeting but may lay groundwork for action at future ones. Undoubtedly there will be discussion of the necessity for fiscal stimulus in addition to the monetary stimulus the banks have already provided. For the Bank of England meeting also on Thursday, most economists expect a dovish committee, with the November Monetary Policy Report highlighting further downside risks to the UK and the external growth outlook. They also see the majority of the MPC voting for additional stimulus, with £60bn added to the Bank’s Asset Purchase Facility. The latest lockdown could easily see this increased or see the probability of greater action.

With regards to economic data, the final October global manufacturing PMIs continue today in addition to the U.S. ISM reading. Then, services and composite PMIs on Wednesday and Thursday. Also, on Wednesday, we will see October inflation data for the Euro area. The week will end with U.S. October payrolls and unemployment data on Friday.

We also have a big earnings week with a total of 128 companies in the S&P 500 reporting by Friday, along with 96 companies from the STOXX 600. In terms of the main highlights, today we’ll hear from Siemens, Clorox, Estee Lauder, PayPal Holdings and SBA Communications. Then on Tuesday, we’ll get releases from BNP Paribas, Bayer, Ferrari, Johnson Controls International, Humana, and Eversource Energy. Wednesday then sees reports from Danske Bank, Consolidated Edison, Vestas Wind Systems, QUALCOMM, MetLife, Allstate Corp and Public Storage. Then on Thursday, releases include Bristol-Myers Squibb Co, Zoetis, Linde, AstraZeneca, Regeneron Pharmaceuticals, Microchip Technology, Electronic Arts, American International Group and T-Mobile US. Lastly, on Friday, there’s Hershey, Allianz SE, CVS Health Corp and Marriott International.

Source: Deutsche Bank, BofA, Goldman

A notable peculiarity that has emerged in the markets is the difference in opinions of the speculative funds. The aggressive traders are quite bullish on tech stocks, yet bearish on the long bond. We mentioned a couple weeks ago that the speculative funds were really selling bonds on the long end of the curve expecting interest rates to go higher. We also mentioned that we didn’t see the logic in interest rates going a lot higher at this point. Since that time, the funds have ADDED to their position expecting interest rates to go higher and it is now a new all-time record.

With all the “stimulus” the Federal Reserve has provided, we find it difficult to believe that they will stand aside and let the 30-year treasury bond market sell off. When the funds have already sold so much, we are wondering now how many sellers are left – we think there will be some buyers coming into the market! The Federal Reserve has no choice but to continue to manipulate interest rates down – if they don’t, it will be a dark winter.

Regards and good investing!

Greyson Geiler