by Greyson Geiler | October 26, 2020

The numbers of infected cases across the globe is coming back in another wave as the Northern Hemisphere starts to turn cold. This isn’t a surprise, of course. When looking at historical pandemics often subsequent waves turned out worse than the first. There are some legitimate questions about how the numbers of Covid cases were being tabulated especially considering drastic differences between states depending on the political party of their governors (see previous post at https://andorracapital.com/progress-of-economic-reopening/). However, everyone agrees that overly filled hospitals are a problem – and that may be where we are going. Currently, there are more than 41,000 COVID patients hospitalized in the United States, a 40% rise in the past month and this second wave is spreading out to more smaller towns with fewer resources, which can translate to less effective care. In Kansas City earlier this month, ambulances were reportedly turned away from hospitals that ran out of room. Field hospitals are currently opening in Salt Lake City and Milwaukee. That is obviously a concern that financial markets appear to be responding negatively to.

More volatility is getting dialed in to financial markets as the idea of a stimulus agreement between Pelosi/Schumer and McConnell. It appears that there is little to no possibility that an agreement will be reached before the election. Although most market observers assume that there will be a stimulus agreement after the election, of course no one knows exactly how that will look. Checking back to 2016 there was much more consensus among market pundits about the effective results of the election. EVERYONE was predicting that Hillary would be good for the stock market and The Donald would be bad. This time around we are all over the board. Many see a Biden victory as a positive for the market, but then just recently JPMorgan head of global equity strategy, Dubravko Lakos-Bujas says “an orderly Trump victory as the most favorable outcome for equities (upside to ~3,900.)” This contradicts a Bank of America analysis that a Democratic sweep of Congress/Senate and the White House would be the most positive for the stock market. The point is not to identify who is right or wrong – the point is that there is not a consensus between analysts. That reality lends for more volatility in front of the election, and the market has been ping ponging up and down on many issues including earnings reports that are very inconsistent. Other market movers are news of the polls, vaccinations, European states contemplating a return to lockdown, stimulus agreements, military conflicts overseas, etc..

We are looking at some of the hard data and the recovery is at least pausing. Economic data from across Europe is softening. Even the white-hot U.S. real estate market appears to be cooling off. New home sales were expected to rise only a modest 1.4% MoM in September (vs +4.8% MoM in August) but things were notably worse with new home sales tumbling 3.5% in September (and August’s bounce revised down to +3.0%.) So, we will see how the recovery continues – and when we get stimulus. Sadly, it is difficult to have a whole lot of confidence in the economic recovery without more government stimulus.

One thing to keep an eye on in the meantime is what is happening in the corporate bond world. Bankruptcies are rising and representing almost total losses to some bondholders. As ZEROHEDGE has warned us in the past:

Instead of recouping, say, 40 cents for every dollar owed, as has been the norm for years, unsecured creditors now face the unenviable prospect of walking away with just pennies — if that.

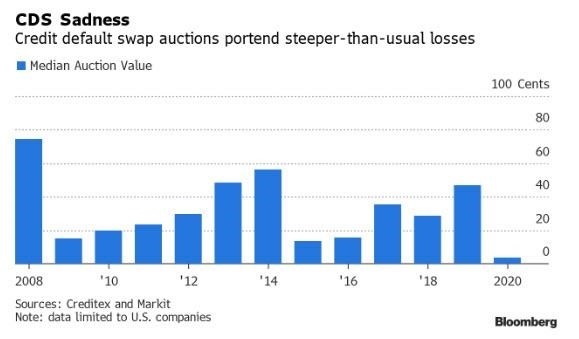

The following chart of median CDS auctions finds record low recoveries for bondholders:

Right now, according to Barclays, the median value for companies’ cheapest debt in credit derivatives auctions this year is just 3.5 cents on the dollar, a record low and far below the 23.4 cent median for 2005 through 2019. Of course, much of this is thanks to the Federal Reserve and artificially low interest rates allowing companies to issue oceans of mispriced bonds for decades now. But it is also partially due to creditors not taking the risk seriously enough amid a frantic search for some sort of interest yield. As we have consistently discussed in this post, the debt load that America – and really the whole world for that matter – is not sustainable long term and watching the bankruptcies coming up will be an important indicator of whether or not the markets can adjust and start pricing this debt more appropriately.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | October 12, 2020

Right now, the stock market is ping-ponging up and down on the news of whether or not the White House and Congress can agree on the next stimulus package. While the future of the economy being dependent upon more “stimulus” from the government is disconcerting, the performance of the U.S. stock market is nothing short of impressive as well as it has held together. Some of the U.S. stock market performance is undoubtedly resulting from foreign money-managers feeling safer in the American markets – as we mentioned last week. But for the market to be holding near all-time highs with the election pending is interesting to say the least. Some market observers are more confident of stimulus from Washington if Biden wins therefore, they say stock market is predicting Biden. Some are saying the market would fear regulation if Biden wins therefore, the stock market is predicting Trump. We won’t even venture a guess which side will win, but our comment has to do with the confidence of the market. As we mentioned last week, historical empirical evidence implies that the stock market doesn’t care between Republican and Democrat president administrations in the Whitehouse. However, the one thing the stock market DOESN’T like is uncertainty. That is the shocking part. The market is so strong with so much drama in the news about how people wont even trust the results of the election. Of course, the stock market could be wrong, BUT IT SEEMS TO BE PREDICTING A DECISIVE WIN – WHETHER BY TRUMP OR BIDEN. The market also seems to be saying that the results of the election will be generally accepted! Whew! Let’s hope the market is right and whoever is in the Whitehouse we can get back to work!

One thing that could derail the strong stock market in the near term is a weak U.S. earnings season that kicks off this week with a number of financials reporting. We will hear from Johnson & Johnson, JPMorgan Chase, Citigroup and BlackRock tomorrow. Then on Wednesday, we have UnitedHealth Group, Bank of America, ASML, Wells Fargo, Goldman Sachs and United Airlines. Thursday sees releases from Morgan Stanley and Walgreens Boots Alliance. And on Friday we’ll get earnings from Honeywell International and BNY Mellon

The coming week is fairly quiet with regard to financial data and world central bank reporting/commenting. On the data side, we will start to see some hard data from the U.S. for September, with the release of the CPI, retail sales and industrial production figures. China will also be releasing their trade balance for September, and we’ll also get the Euro Area’s industrial production for August.

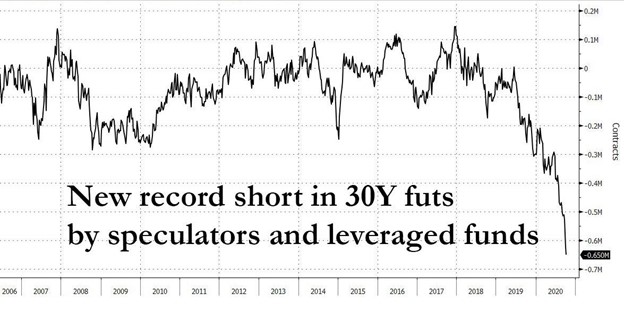

One last thing to mention is long term interest rates. Looking for near term surprises that could derail the stock and bond markets other than the election, one has to address the yield curve. We recently mentioned in this post that it appears long term rates have bottomed. However, this week we want to mention that just because long rates have bottomed doesn’t mean they are imminently going higher. Strangely enough, the speculative trading community does not agree with us. Take a look at the “Commitment of Traders” report showing how negative trading funds have gotten on the price of treasury bonds (meaning they think long term interest rates are going higher.)

This is a new all-time record BY QUITE A WIDE MARGIN. So, the most overcrowded trade in the marketplace right now is traders that are wagering long term interest rates go higher. In our experience in the financial world, when everyone is betting one way, look to the other.

We have repeatedly complained in this post that the Federal Reserve should not be the arbiter of short-term interest rates – a free marketplace should be. At least the longer end of the curve is still more influenced by a free market than the short end is. Traders are loading the boat thinking these long rates will go higher – we think they will be disappointed, and the good news is that stock and bond rallies won’t get hampered by higher rates.

Regards and good investing!

Greyson Geiler

by Greyson Geiler | October 5, 2020

The upcoming week should be fairly quiet for the financial markets with China on holiday until Friday and the Vice-Presidential debate on Wednesday being the highlight event in the U.S. The only interest rate decision from the G20 central banks will be from the Reserve Bank of Australia on Tuesday and that should prove to be a benign no-rate-change decision. As far as economic data, the main highlight will be the release of the services and composite PMIs from around the world. Those will be out in the beginning of the week but expect China’s on Thursday after holidays. The second wave of the virus has affected the services sector across Europe with the PMI falling into contraction below 50 at a 47.6 reading. Germany and France are both in contraction with PMI readings at 49.1 and 48.5 respectively.

Looking at just the U.S., the key economic data releases this week are the ISM non-manufacturing index on Monday and initial jobless claims on Thursday. In addition, minutes from the September FOMC meeting will be released on Wednesday. There are numerous scheduled speaking engagements by Fed officials this week, including Fed Chair Powell on Tuesday and New York Fed President Williams on Wednesday.

Comparing the Eurozone to the U.S. shows quite stark differences. The Eurozone unemployment would be close to 11% if we used the same calculation as the United States. The OECD estimates that unemployment will rise above 10% in the eurozone before year-end as furlough schemes end. Here in the U.S., unemployment numbers have come down considerably from the height of covid lockdowns to less than 8%…

Civilian Unemployment

Many question the math of how the unemployment rate is calculated, so we may be artificially optimistic on these numbers. However, the comparison between the Euro Zone and the U.S. clearly shows a more resilient economy for us domestically. We are not the only ones who can identify this in the financial world. Many fund managers overseas are investing in the American markets which has helped buoy our indexes in these troubling economic times.

Going forward of course one has to put the election on the radar as a major source of volatility. The vast majority of investors — 93% — believe the presidential race will affect the stock market, according to a recent survey from Hartford Funds, an asset manager. Moreover, 84% said they expect that will impact their investing habits. Interestingly, most investors intuitively believe that a Republican presidency leads to better stock market returns. However, when you remove some of the outlying events since 1933, there is virtually NO difference in stock market returns whether the White House had a Republican or Democrat in office. This time around, people believe that with a Trump victory energy and small cap stocks will do well. If Biden wins infrastructure and health care may outperform. At the end of the day it is more likely that big differences – depending on who wins the White House – would be short term in nature. But in this day and age anything can happen – so stay alert!

Regards and good investing!

Greyson Geiler

by Greyson Geiler | September 28, 2020

The stock market as defined by the S&P 500 has pulled back 10% recently, the NASDAQ more like 14%. Many regard this as a well overdue pullback and now staring at a number of challenges, the markets may have a difficult time rallying to new highs in the near term. First and foremost the election is starting to loom. Here in our posts, we don’t get political to one side of the spectrum or the other. For the most part, that is due to our disdain for politicians in general, but with this election especially, there seems to be a justifiable unrest on both sides of the isle. Our opinion is that it will represent more volatility in markets although we are not really sure which direction for which candidate. So we will take the easy way out and just warn for caution in general with regard to election effects on the market.

Part of the political unrest is amplified by the vacancy in the Supreme Court. Although vacancies have opened in an election year 29 times historically, this is an extreme circumstance and understandably has many on the left very uneasy.

Then, we have the situation with the next iteration of the Cares Act. The first go around in March was only $2.2 trillion in “fiscal stimulus” so naturally, many are waiting around for Round 2. Of course Congress and the Senate can’t agree on who gets what (shocker) so that doesn’t appear to be progressing any time soon. Some of you may be reading this thinking “good – we don’t need to hand out any more free money” to which we would normally agree. This time around is pretty interesting, however with as many unknowns as are left hanging out there. Will student loans have to be repaid? Will landlords be able to evict those that haven’t paid according to the rental agreement (the moratorium expires in Dec.)? What will bankrupt states and municipalities do with many of their bills coming due and unemployment benefits not financed? What will those out of work do now that the unemployment checks are running out? Lots of questions without answers and Morgan Stanley’s public policy strategist, Michael Zezas is saying that there is only a 33% chance that any version of the Cares Act 2 will be passed by November 3rd.

Additionally, North America is now running into the fall season and another round of the Covid may put a damper on economic recovery expectations. We really don’t have an opinion of exactly what will happen with economic lockdowns because of a potential resurgence of the virus. That is completely up in the air – but we do add it to our list of concerns.

Next up on our list of concerns for the stock and bond markets is that it appears long term interest rates have bottomed. The ten year treasury note interest rate cratered between March and Sept from about 2% to about .5% – really a 75% reduction in interest rates! That has at least helped fuel the rally in stock prices as it has obviously defined the rally in bond prices. It appears that without another serious economic fallout from a resurgence of the virus or some other factor, long term interest rates may have hit a bottom (ten year treasury back to .65%)

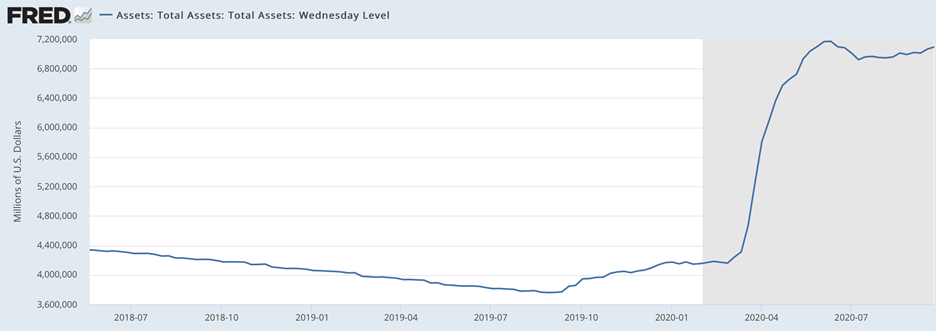

Last but certainly not least is the uncertainty of what sort of asset purchasing the Federal Reserve will do. The Federal Reserve has been a vacuum cleaner of mortgage backed securities, treasury bonds and yes even corporate bond (junk bonds too) ETFs in the last six months. Take a look at what they have in total on their books…

Three trillion dollars worth of assets got stacked onto their books within a month of the corona virus outbreak. Never mind whether or not the FED has the authority or mandate to do so – they did it. The question now is how/when/if these asset purchases continue. Intuitively, one would think the FED would try to let markets stand on their own now that some normalcy has returned. However, one can now be relatively certain that the FED will backstop any significant pullback in asset prices for the foreseeable future. The 200 day moving averages of the major indeces (Dow, S&P, NASDAQ) will certainly be defended (asset managers buying stocks at these levels to support prices) if we continue the pullback to those levels. Stay tuned!

Regards and good investing!

Greyson Geiler

by Greyson Geiler | August 31, 2020

Last week at the Federal Reserve “meeting” in Jackson Hole (actually done remotely via Zoom) much of the discussion revolved around the Fed “mandate” of institution/initiating/managing 2% inflation. We put quotes around “mandate” because the purpose of the Federal Reserve continually changes over time and we can find no record of Congress ever legislating that the Fed should have an official inflation target. From the Richmond Fed’s own website, we found this gem…

Since 1977, the Federal Reserve has operated under a mandate from Congress to “promote effectively the goals of maximum employment, stable prices, and moderate long term interest rates” — what is now commonly referred to as the Fed’s “dual mandate.”

We’re not really sure how the initial part of that statement constitutes a “dual” mandate considering there are three variables listed or where it has been written that the Fed should compile a balance sheet of $7 trillion by actively buying assets including corporate junk bonds. But regardless of our opinions, the FED keeps marching along and changing the rules as it sees fit. January of 2012 is when the Federal Reserve under the supposed leadership of Ben Bernanke initiated its 2% inflation target. The Fed decided that an effective inflation rate for the basic consumer economy as defined by woefully inaccurate measuring systems would be 2% (of course after “hedonic” adjustments which are yet another arbitrary calculation.) Why 2% inflation you ask? Well, that is a good question and it has never been answered. Our opinion is because it can’t be answered – a 2% inflation target is completely arbitrary and, in our observation, absurd. We thought that it had been settled – centrally planned economies, prices – well, pretty much centrally planned anything is not a good strategy. We will never be convinced that a room full of academics (most Fed governors don’t spend much time working in the real economy) can set prices of anything in a more effective and accurate manner than the hundreds of millions of participants in free markets. Centrally planned economies over all human history proved inefficient and susceptible to meltdown. Alas, the central planning in the world’s largest economy – the US – has recently shifted into overdrive.

So now our fearless leaders at the Fed have decided that a 2% inflation target should be shifted to some sort of a running average of 2%. Meaning that because inflation by their measure hasn’t constituted 2% for many years (thinking inflation has been benign makes us think they haven’t bought any bonds or stocks recently – or had any health care expenses – or had any kids that need to go to college – or bought any vacation homes or…) that going forward we can tolerate higher inflation in order to catch up. We don’t want to go too far off on a tangent describing how stupid that is, but here is some quick economics 101. Deflation happens in free markets. Especially in markets with such rapidly changing technologies like we have now, there will be some SERIOUSLY misallocated resources that, in a deflationary wash-out will get effectively reallocated. Well, our fearless leaders at the FED were out sick when that was discussed in Economics 101 for freshmen, so they have determined that deflation should not happen and inflation should in fact be 2% per year (or higher if we need to catch up.) The Fed’s primary mechanism to initiate inflation is to pin short-term interest rates to zero. That encourages families, companies and every level of government organization to load on more debt – which has been proven to be deflationary and perpetuates the problem. Consider this, because of these interest rate manipulating mechanisms of the Fed (rather than letting the marketplace determine interest rates) the number of “zombie” corporations in America has rocketed higher. Nearly one in every five publicly traded U.S. companies is a zombie, according to data compiled by Deutsche Bank Securities.

Meaning, 20% of our publicly traded companies are losing money. They only survive and are able to continue destroying capital because they have enough cash flow to warrant borrowing more money at these absurdly low interest rates.

Recently we ran across some writings of Rabobank’s Philip Marey and found this point spot on…

The much deeper problem for the US economy is the asymmetric impact of Fed policies on households and businesses. The Fed’s monetary and regulatory policies have contributed to a form of capitalism where the rewards are going to the 1% and the risks are borne by the 99%. The current crisis response has made it painfully clear again that the Fed’s policies benefit high income individuals and large corporations, while small businesses and low income individuals bear the burden. While the Fed likes to see itself as part of the solution to America’s economic problems, it should ask itself whether it is also part of these problems.

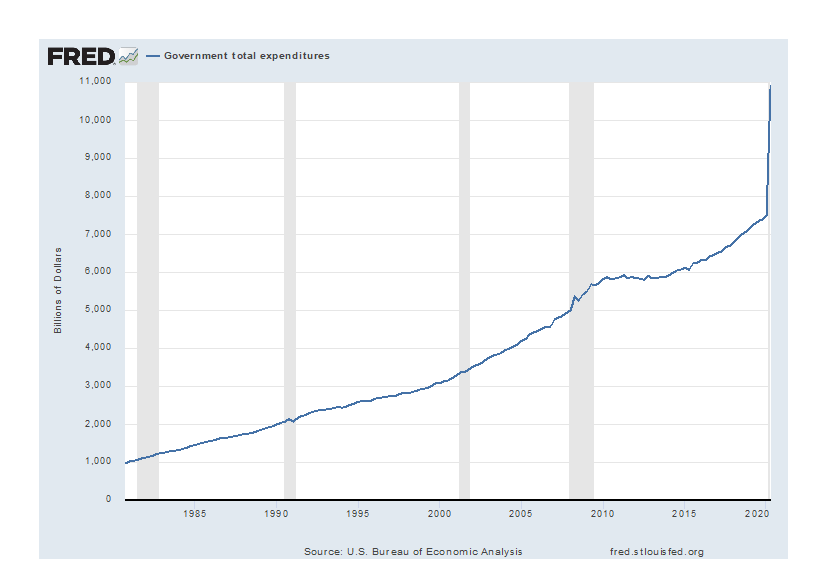

So if things aren’t bad enough on the monetary side of things, then let’s take a quick look at the fiscal side of things. No one knows for sure, but it appears that the Federal Government’s deficit this year will be approximately $4 trillion – and total debt will print over $27 trillion by the end of the year. So we don’t lose a sense of proportion here, in the ENTIRE HISTORY OF AMERICA UP TO 1980 the aggregate debt of the United States was $1 trillion. We have blown out 4 times that much in eight months. Government spending has gone “hockey stick” – take a look…

To be fair, the chart you are looking at is not just Federal government spending – but state and local as well – but government spending now constitutes roughly half of our economy. Karl Marx is giggling in his grave…

Figuring out what this means for investors like us going forward is where the rubber meets the road. It is very scary that so much of the economy is dependent on continual government support – of course we don’t know how long that can last. However, we don’t want readers to draw the conclusion that we think the stock market is going to melt down soon. What the Fed is telling us, basically that they won’t raise interest rates anywhere in the foreseeable future – is very supportive of the stock market. The problem is that the economic support of the stock market isn’t really there (especially when you consider covid relief funding coming to an end) and with the risk of the election coming in November – which we don’t think ANYONE really has an idea what will happen market-wise around that. Some stock exposure is fine, some cash for upcoming opportunities is fine. Find places to sell bonds and bond funds as the rewards of owning don’t match the mounting risk and as we always say – don’t sell your gold.

Regards and good investing!