by Greyson Geiler | August 10, 2020

Stephanie Kelton, a professor at Stony Brook University recently turned up the apple cart in normal economic/monetary thinking with her book The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy. Kelton also has served as chief economist on the Senate Budget Committee. In her book Kelton’s basic premise is that there is nothing necessarily wrong with running a deficit and accumulating debt on a sovereign national government level…

“What if the federal budget is fundamentally different than your household budget? What if I showed you that the deficit bogeyman isn’t real? What if I could convince you that we can have an economy that puts people and the planet first? That finding the money is not the problem?”

This post is not a book report – as we have not read and dissected it, however the book has gotten a lot of press and certain tenets of it have spilled over into a lot of our political discourse and into the actions of our Federal Reserve – so it is worth discussing!

According to Wikipedia, MMT is “a macroeconomic theory that describes the currency as a public monopoly and unemployment as the evidence that a currency monopolist is restricting the supply of the financial assets needed to pay taxes and satisfy savings desires.”

First, an obvious comment is how the entire work is packaged from the get-go in the title of Kelton’s book “…the Birth of the People’s Economy.” That rings more of a manifesto than a statistically backed scientific theory – and the fanatical political adhesion to this mantra is chilling. Indeed, the “Green New Deal,” for all of the planet-saving ideals it has that may be worthwhile, it has NO basis in any economic reality. It is truly a fairy tale devoid of authentic strategies to build a bridge between the energy processes we have today to the desired “renewable energy” usage of the future. Yet it is being co-marketed with MMT by some in D.C. that are further left on the political spectrum and getting a disturbing amount of traction (including with the supposedly “centrist” Biden campaign.)

Another observation of MMT is that is seems to gloss over the abundant economic research that shows productivity numbers DECLINING significantly over time as a system loads up on debt. Study after study in the developed world has shown the inverse relationship between growth and debt – MMT doesn’t properly address this. Printing dollars doesn’t help, because dollars are not “money” dollars are debt too (a liability on the Fed’s balance sheet.)

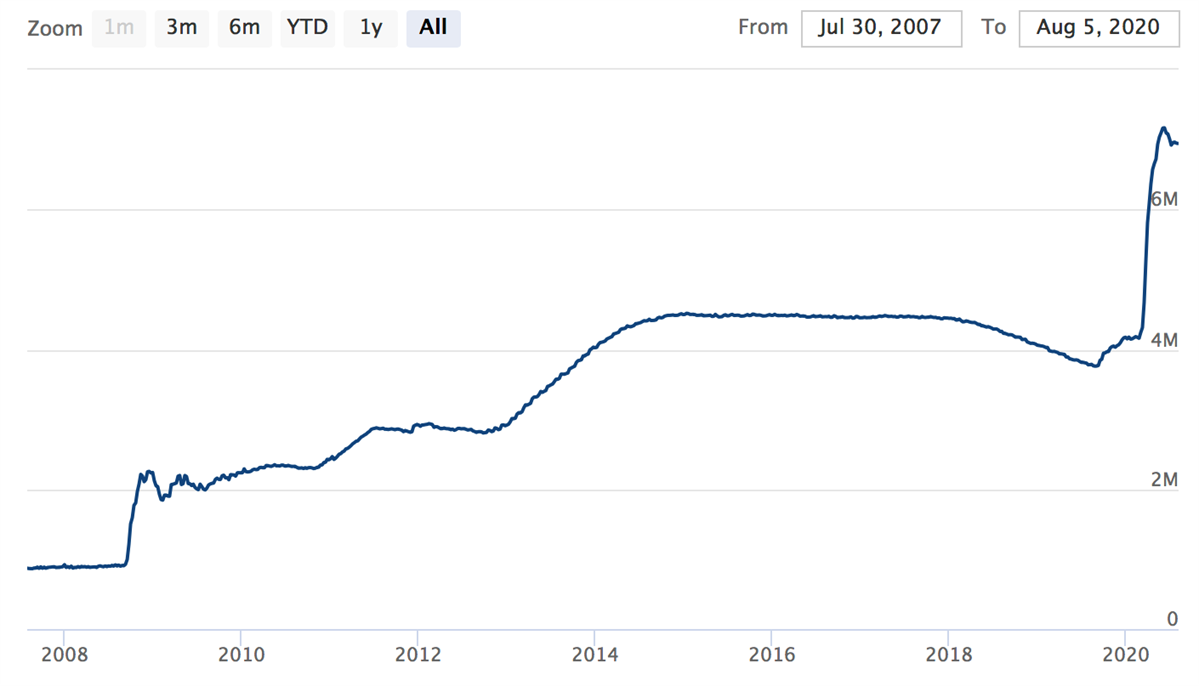

That brings us to the actions of the Federal Reserve in their asset purchases which is just a derivative of the MMT government spending strategy. Ever since the 2008 economic meltdown, the Fed has artificially suppressed interest rates by buying treasury bonds and other debt instruments – now aggregating approximately $7 trillion which is a full order of magnitude larger than just 13 years ago!

The goal posts of the “mandates” of the Fed continually get moved by Congress and by the Fed itself and now the Fed is backstopping a truly staggering amount of our financial system’s debt. Buying junk bonds seems preposterous for the Fed to be doing and that is a common complaint among worried observers. However, that is just the tip of the iceberg. If the Fed’s perpetual bids were pulled back and markets were left to stand on their own two feet, we believe there would be a downward tsunami in asset prices. Of course, the Fed can’t let that happen so the charade goes on – the government/Fed conjure up capital and purchase assets at over-inflated prices, debasing and consuming capital in the meantime in the name of “stimulus.”

The present state of our fiscal and monetary policies in the developed world are an experiment on a scale that the world has never even contemplated before. Modern Monetary Theory is really not a theory, but rainbows and unicorns fantasy of free lunches for everyone – and it is administered by the government. History is replete with different versions of this “theory”, but the government designed and controlled part of it reeks of the Soviet experience in Eastern Europe. Not a good sign…

The good news is that technologies in a wide array of industries are going parabolic, which by its nature is very deflationary. Printing or loaning new “money” into existence isn’t spreading wealth – it’s just spreading more claims upon the wealth that people and business actually do produce. Many of these new technologies are making true wealth creation much easier and, in the process, holding breakaway inflation (other than in asset prices) at bay. Of course, we have no idea how long that can continue if the Fed continues expanding monetary policy to the degree it has recently. So, as always, we will tell you – don’t sell your gold and stay tuned as this continues to be fascinating!

Regards and good investing!

Greyson Geiler

by Greyson Geiler | August 3, 2020

Individual states have all begun to reopen to some degree or the after the coronavirus thrust the country into lockdown starting in March. Nothing moves in a straight line, so now some states are pausing plans to re-open and a few are reversing amid rising case counts. Several are re-imposing restrictions they had lifted earlier — and Arizona is a perfect example of that.

As we have repeatedly mentioned in previous posts, the progress of economic reopening is DRASTICALLY behind the resurgence of the stock market. Of course, much of the bond and stock market rebound is due to “stimulus” from the Federal Reserve and Congress. More of the rebound may be due to expectations of vaccination research which is now going on at a breakneck pace. We hope to see green shoots in the economy, but so far, the numbers aside from a few tech company earnings has been pretty tepid. Our opinion is that the economic recovery will come faster if government gets out of the way…

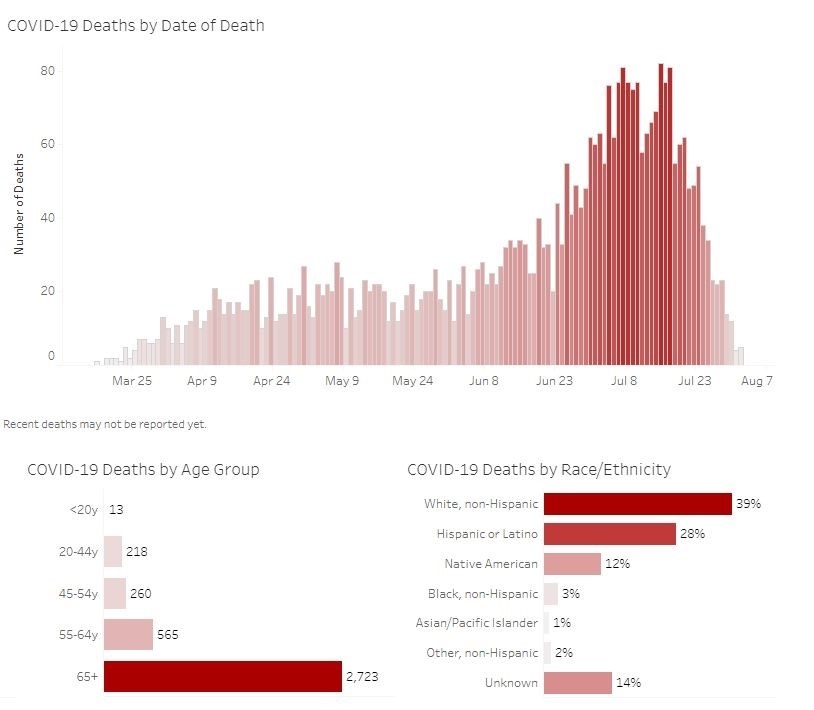

Part of our issue with government making so many decisions is that they are making them with flawed data. We certainly do not view our weekly post as a pollical platform to spread our agenda on one side or another. But we do watch government actions and do our best to assess how that may affect the investing landscape. When you look at the data on which Federal, State and Municipal governments are basing decisions, you do not have to be a mathematician to be suspicious. Here is an example. Reports of the death rate of the covid-19 virus vary DRASTICALLY from state to state. Connecticut is reporting an 8.9% death rate while Utah is reporting .76% (numbers from the CDC.) Is the information telling us that it is ALMOST TWELVE TIMES as dangerous to get the virus in Connecticut as it is in Utah??? Not surprisingly, one governor is a Democrat and the other is Republican. We have no delusions that the governors of states have perfect control of the data that is being dispensed regarding the virus. But when you aggregate the information across the country, Democratic governorship states are reporting almost exactly twice (4.4%) the death rate from those contracting the virus (cases) as the states with a Republican governor (2.2% death rate.) That is not just a statistical anomaly. That represents some fudged data – we just don’t know who is doing it. We are confident that the Covid-19 virus does not have a political affiliation. On top of that there are many anecdotal testimonies to how faulty the reporting of cases and deaths are – but we don’t base our opinions solely on those…

The good news for most of us reading this post – is of all states that have been labeled recent “hot spots” of the virus, Arizona – at least from the data the ADHS is providing – appears to be well past the worst of it. Take a look…

In the meantime, the stock market isn’t backing down. It appears to be looking past the virus and may be heading higher before concerns of the election volatility start taking front stage. All the usual acronyms are coming out in the financial news media. The FOMO (Fear of Missing Out) trade is in full force. Also because of interest rates being pinned to microscopic levels the TINA (There Is No Alternative) trade is being implemented and recently we caught wind of the YOLO trade – or You Only Live Once. So, the markets are telling us it is “risk on” for the near term. If there is a vaccine that shows legitimate promise that comes out in the anytime soon, we are confident that markets would add another leg higher as well.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | July 27, 2020

Everyone knows that there is a disconnect between the positioning of the major U.S. stock indexes and the performance of the economy. The question is whether that gap is going to be corrected by an economic rebound or by the stock market selling off. As far as market expectations of earnings reports for the second quarter, the bar is certainly low. In aggregate, S&P 500 companies are projected to report a 43 per cent plunge in profits for the second quarter and a 10 per cent drop in revenues, according to FactSet. The net profit margin for companies on the blue-chip index is slated to come in at 7.3 per cent — the lowest since the final three months of 2009. However, with the bulk of companies that have reported earnings so far, numbers have generally come in brighter than “expected.” We mentioned in earlier posts, that Wall Street tends to play a game of setting expectations lower than reasonable so that when the bad numbers come, they can be a pleasant surprise. Perhaps reflecting the effects of unprecedented stimulus from Congress and the U.S. Federal Reserve. As of Thursday evening, almost four-fifths of the S&P 500 companies that had provided quarterly updates had posted earnings per share that were above analysts’ expectations and, in aggregate, were reporting earnings 13 per cent above estimates, according to FactSet. Both those numbers are better than the five-year averages. Some of the earnings forecasts for yet to report companies have pushed higher – so the remainder of earnings season will probably be better than the terrible situation many were braced for. Of course, all these better performances could be reflecting the effects of unprecedented stimulus from Congress and the U.S. Federal Reserve. The Fed has bought up assets (bonds and bond mutual funds) in the open market thereby more than doubling the size of its balance sheet to more than $7.5 trillion. Congress has thrown in some humungous “stimulus” packages spending some $3+ trillion – and that will likely go higher! So, it remains to be seen how well the market would stand on its own feet if/when the artificial support is removed.

One thing to keep an eye on is dividend payments which were down a net $42.5bn in the second quarter (among S&P 500 companies) from the same period a year ago, the biggest such decline since the financial crisis, according to Howard Silverblatt, senior index analyst at S&P Dow Jones Indices.

Going forward many companies may still decline to provide guidance as there is so much turmoil muddying the waters. Everything from the Covid-19 virus to riots and protests to an escalation of political conflict with China and the pending election are adding huge unknowns to decision making and therefore forecasts of our economic future.

With that in mind, we look back at the indicators that we have repeatedly reference in this post. The selloffs in crude oil prices and junk bonds have both had a band-aid thrown on them by the FED and to this point have not dominoed into other problems.

The present selloff in the value of the U.S. dollar versus other currencies:

U.S. Dollar Index – September 2020 Contract

This is not yet a five-alarm fire by any stretch – but we need to watch it (and don’t sell your gold.) Keep in mind this index is heavily weighted toward the Euro – so it is not indicative of the value of the dollar universally. This appears to be a relaxing of some of the panic the pandemic brought us – which is good news… but if the selloff continues it will become a concern. The world economy from some perspective will be better with a weaker dollar – there is a ton of debt owed in dollars. The issue would be if the selloff accelerates and dominoes into panic.

Right now, there is no panic in the stock markets and, although they could certainly selloff a bit and consolidate in the short term, we don’t see huge medium-term danger. The Fed and Congress will certainly keep throwing support at asset markets – time will tell if it will be sufficient.

Regards and good investing!

by Greyson Geiler | July 20, 2020

We are now entering 2nd quarter earnings season for all publicly traded companies. This is where the rubber will meet the road for an answer to the dichotomy of tepid economic numbers along with a strong stock market that has launched off its March lows. Everyone knows that the corporate earnings numbers coming up for the second quarter will be terrible. But the estimates will be lowered to the point that the actual numbers will beat the estimates – which will essentially be like putting lipstick on a pig. The most important numbers to watch will be revenue numbers – which are much more difficult for corporate accounting departments to fiddle around with than the “earnings” numbers are. The million-dollar question going forward is how quickly the economy can recover from the recent disaster and justify the rebound in stock prices.

Last week the banks started earnings season of on a good note. JP Morgan’s record revenue had many investors sighing in relief, although their profit was roughly half of a year ago due to a beefing up of their loan loss provisions. Other banks followed suit with better revenue numbers than profits, but some are skeptical the remainder of earnings season will not be so rosy.

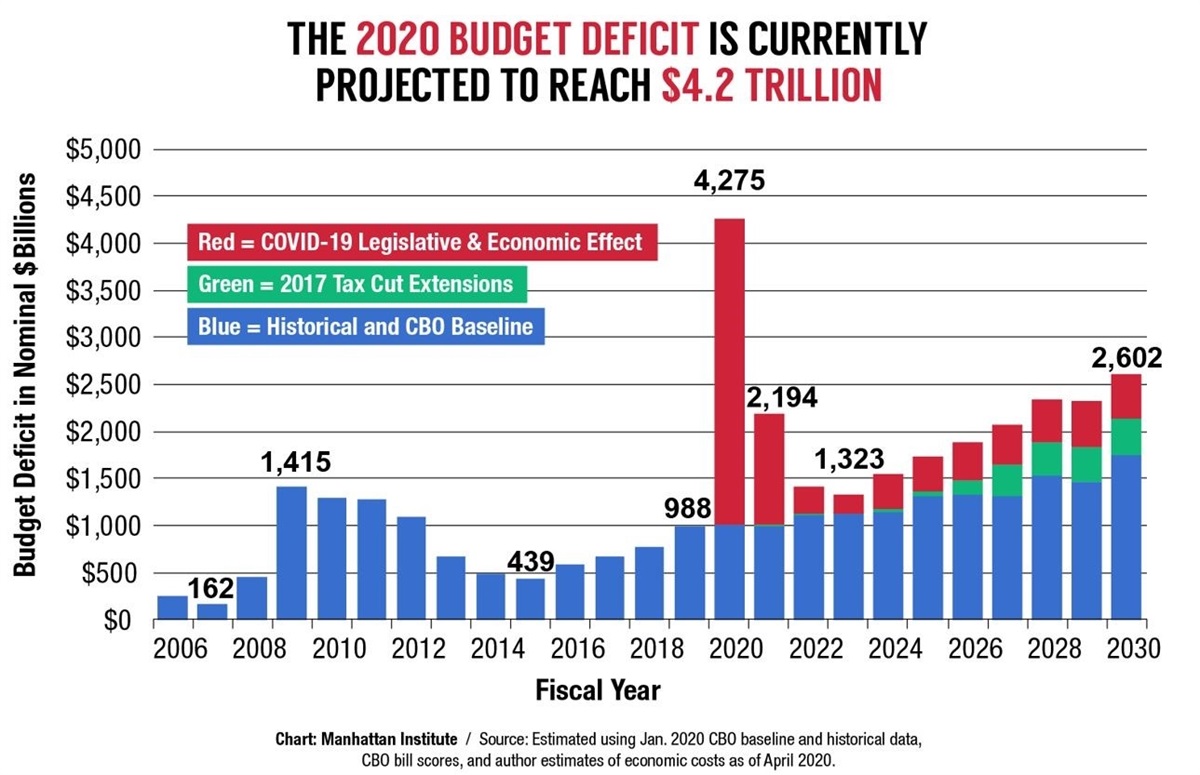

We are relatively certain that Congress will jerry-rig more stimulus packages into the fall as it is quite obviously that there is no “V-shaped” recovery in the economy. What is truly mind-numbing is the deficit that our Federal Government is ringing up this year. From the Manhattan Institute, here is a visual look – and this estimate isn’t even inclusive of some of the new stimulus talk that is circulating DC right now…

Of course, the “deficit” is the difference between the amount of money the government takes in from tax revenues and the amount of money it spends. This year revenues have cratered, and expenditures have rocketed – so we are looking at a Federal Government budget deficit that is THREE TIMES that of 2009 after the last economic disaster. Historically (other than WWII) the government could not have borrowed this much money to spend in a deficit scenario such as this. The investing marketplace would have been overwhelmed and the price of the bonds (all this government debt) would have been much lower, consequently interest rates would be much higher. However, now our Federal Reserve is buying most of these government bonds, so the interest rate that is being payed is miniscule (about .6% on 10-year notes!)

This monetization of national debt frees up the government to spend with reckless abandon because they don’t have to find other buyers for their bonds – and that is what is happening. Benefits and bailouts are being handed out to many and so for the short term asset prices are responding. The stock market has rocketed back to new or near new all-time highs and it certainly appears that will continue until the economy has to stand on its own rather than get supported by the Fed and the government. Earnings season will not show a good economy and with unemployment numbers still about 11% – higher than at the worst of the last recession – the actual economic numbers are not roaring back. The rest of earnings season won’t be pretty, but right now that doesn’t matter to the stock market. As we often say in these posts – don’t sell your gold!

Regards and good investing!

Greyson Geiler

by Greyson Geiler | June 15, 2020

The roller coaster in the stock market continues with volatility last week returning to the type of panic moves as we had in March. Trying to make sense of markets with economic numbers in full out depression territory and a corresponding best 50 day run in the history of the stock market has left many scratching their head. Really markets have been ping-ponging on the news du jour with a backdrop of a FED put – aka the FED is going to backstop everything.

So, the market is performing remarkably well considering underlying economic conditions and now some of the investment houses are starting to extrapolate this performance going forward, which may be indicative of some short-term froth in the market. One notable example is Morgan Stanley equity strategist Michael Wilson flipping from bear to bull by raising his 12-month, June 2021 S&P target to what would be an all-time high 3,350, from the current 3,000: Our new target of 3,350 assumes a multiple of 20x forward 12- month earnings of $168. His numbers don’t make much sense to us, but it is an indicator of some of the market sentiment recently turning bullish.

Some market indicators speak to things being in full bubble status just three short months after the world being in an economic depression. The most obvious example of this is the stock price of car rental company Hertz. The company has filed for Chapter 11 bankruptcy, has bond prices indicating a shareholder equity value of the company of about MINUS $2 billion and they are doing a common stock issuing through Jefferies as we write. This stock issue is raising about $500 million and in their offering documents Hertz attorneys warn multiple times that any investment in the stock could easily become worthless. The stock is still trading over $2.5 per share as we write. This is statistical madness as new stockholders would need something approximating a miracle to avoid total loss – or maybe they just need a bigger fool to buy the worthless stock from them at a higher price. This won’t end well for Hertz, but it also concerns us about the conditions of a market that would support recklessness such as this.

What is concerning for us as we watch the world emerge from a virus-induced hibernation are some of the empirical realities that don’t indicate a V-shaped recovery. The most recent example of this is the Monthly Treasury Statement for May which showed federal withheld income tax receipts falling a record 33% from the comparable period one year ago. The decline in May tax receipts exceeds the 30% decline in April. Monthly tax (gross) receipts have been reported since 1973 and April and May declines are the largest on record. Federal withheld tax receipts are directly related to workers paychecks. The scale of the decline in tax receipts is nearly three times the decline in reported household and payroll employment. The unprecedented gap raises questions about the accuracy of the April and May employment reports which were showing improvements in our employment situation. Time will tell but here is our list of concerns going forward including short, medium, and long-term issues…

- Civil unrest including rioting and looting and rising dissatisfaction with governments

- The rising number of bankruptcies (24 Hour Fitness just filed) – and potential rollup to bank balance sheets creating systemic problems

- Atrocious state and local government finances including drastically underfunded pensions

- Rocketing Federal debt and deficits

- Geopolitical tension – China and Russia are sabre-rattling

- Politics – the outlook for the U.S. November elections has swung away from Trump which, as far as the markets are concerned lends for more volatility – more “unknown”

- Zero-bound interest rates – probably permanent – causing investment confusion

- Rising unemployment and growing corporate insolvency

- A STAGGERING disparity between haves and have-nots that is getting worse

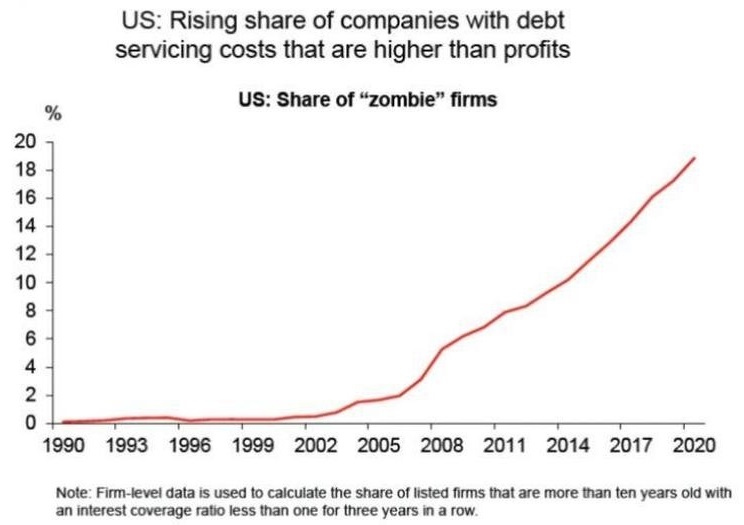

- The rise in the number of zombie companies that will make economic recovery more difficult (see chart)

Zombie companies are those that don’t make enough money to pay down their own debt, so they are dependent upon low interest rates and a continual growth of their debt. This keeps the economy from reallocated misused resources, and it is a daunting problem.

Of course, the Federal Reserve has committed to backstopping all investors in the face of these risks and to this point it has kept markets together very well. The rubber will meet the road when earnings season rolls around again next month, and we will see the 2nd quarter numbers which will be horrific. The market knows that already though, so we are certainly not suggesting panic out of all risk assets. We do, however, feel it is wise to hold significant cash in investment portfolios as we feel there will be more opportunities going forward without chasing markets higher.

Regards and good investing,

Greyson Geiler