There are plenty of financial doomsdayers out there that write ad nauseam about the imminent demise of the US dollar and how everyone needs to pile all their assets into Bitcoin or gold or some foreign currency as a life raft to weather the pending financial/economic Armageddon. This week we are not piling on and adding to the panic. We are going to talk about building assets in an alternative structure that is a new way to even out the risk in our financial planning. However, first we would like to start with why the US dollar IS NOT imminently going to zero…

Understand that the monetary system that the entire world uses was built by the United States post-World War II. The US dollar was then “as good as gold” as it was backed by and could be redeemed for gold. Although that system has been altered along the way – Nixon ended the gold-backing in 1971- much of the same system is still intact. The IMF and the World Bank that were created at the same Bretton Woods meeting post WWII have continued to heavily influence world finances. The US dollar remains the world’s reserve currency. Let’s look a little further into what that means… The dollar is the official currency of 11 countries other than the US, mostly in the Americas and the Caribbean. It is also the quasi-official currency of many countries that have a set exchange rate pegged to the US dollar. It is accepted in many countries as payment where there is no pegged interest rate including many countries in Southeast Asia. It is the medium of exchange for approximately 80% of international trading outside of the Eurozone where the Euro is dominant. US dollar denominated assets make up almost 60% of the world’s central bank reserves – according to the Atlantic Council. In daily currency trades, the US dollar is part of 90% of the transactions. Perhaps most importantly, the US treasury bonds have turned into the dominant asset class in which central bankers around the world hold assets. It is a US dollar dominated world – PERIOD. Everything else – even the Euro – is completely overshadowed by the US $. Right now, there are many people talking about the BRIC (Brazil, Russia, India, China) countries putting together a gold-backed currency – THEY JUST CAN’T TELL YOU WHEN IT WILL ACTUALLY HAPPEN This is wishful thinking at best. These countries don’t trust one another except when they are all resisting the US worldwide monetary bullying. They won’t be able to agree on a depository for gold that could establish a delivery mechanism for a gold-backed currency. They have all built paper currencies that have crumbled within recent memory, and they won’t be able to put together a solid new currency as a collective. But do keep in mind that they are talking about it and will continue making efforts to evolve away from the US $ for international transactions which over time will be detrimental to us.

Our monetary system does have some serious flaws – both in its design and in its execution – that we continually review in this weekly post. America – actually, the entire world – has a Federal Reserve or corresponding central bank that is behaving recklessly stimulating too much then contracting too much engineering repeated boom/busts. Now they are changing rules on the fly and shooting from the hip to bail out banks such as Silicon Valley Bank or carving up a Signature Bank and giving the good parts to Chase. US leaders have forced the Russians out of the international trade system of the US Dollar, and they are forced to find alternatives. On the fiscal side, the financial profligacy of our government is onto absurd levels with budget deficits and total debt rocketing to the moon. Although interest rates are settling down a bit, they are still higher than they have been since before the 2008 meltdown and these increased rates are being applied to a debt load today which dwarfs what we had in 2008. We have an ageing population – a student loan disaster that to this point has only been brushed under the rug and a litany of other problems. No, the US $ isn’t going to zero tomorrow, but we should be looking for an on-ramp for alternatives that can mitigate some of our US dollar risk. The Fed will at some point have no choice but to come back to the table printing more currency units to try to fill the voids they have created in the world’s financial system over the last few decades.

So, what are some alternatives to the US Dollar? Again – we are looking for avenues to diversify and effectively create a hedge for some of our holdings – not looking for a total divestment of the US $. Historically people have talked about other currencies – such as the British Pound or the Japanese Yen. Without rehashing details, we are not fans of looking for another paper currency for the long term. The whole world is dependent on the US dollar and if it falls apart, serious damage will be sustained by the entirety of the world economy. Other paper currencies may be a successful short-term trade, but they are certainly not a long-term alternative.

What about crypto currencies? We have written repeatedly about cryptos and the efforts of world central banks to create their own. That would be a nightmare of totalitarian control, and we can’t stress enough how dangerous a central bank-controlled crypto would be. As far as Bitcoin and those types of cryptos, we are relatively agnostic. However, the price volatility alone in Bitcoin keeps it from being the center of any monetary system or a viable alternative for a significant percentage of your US $ based net worth. That being said, speculate with smaller sums if you choose – just be careful because the BlackRock and Vanguard-type players in the financial world are taking control of the crypto space. That runs counter to the original philosophical goal of the Crypto World, and we worry that the future of crypto may be volatile…

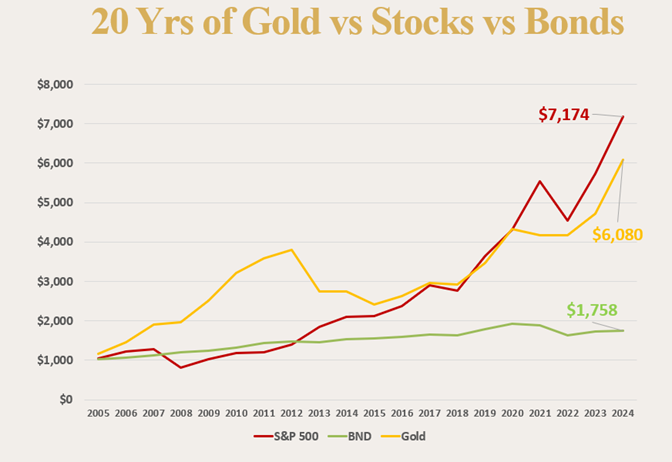

An obvious alternative to the current monetary system is gold considering that is money and has been for more than 5000 years. We frequently talk about gold and encourage the purchasing of it. However, when contemplating the building of a significant portion of our portfolio denominated in gold, there are some concerns that need to be addressed. One of the most frequently asked questions when talking about adding gold to a portfolio is “where should we store it.” The answer to that is certainly not a safe deposit box, so some end up paying for professional storage, which is generally about .25%-.75% annually. That gets annoying and adds up over time. Some prefer to “own” gold through the ETFs on the stock exchanges and that can incur fees as well. Past the storage, some investors are repelled by the doomsdayers and don’t subscribe to the immediate panic. Especially since a lot of doomsdayer guys have been vocal for a couple decades and disaster just hasn’t happened yet. There is also the issue with what type of metal to buy – gold coins that are rare and have numismatic value or just bullion? And what about the liquidity? How does one buy and sell? These are challenges when considering diversifying some of your assets out of the dollar, but let’s take a historical perspective on the long-term financial viability of investing in gold before we worry about some of these details. Here is a hypothetical example of owning gold for the last 20 years. We will compare it to owning the total return of the S&P 500 (dividends included.) We will also add a bond fund that represents a hypothetical holding of US dollars and getting a low-risk yield on those dollars. The results are a little surprising…

$1,000 starting 20 years ago in 2005 in the S&P 500 has grown to $7,174. That’s a pretty impressive return. Not surprisingly, that same $1,000 in our hypothetical bond portfolio would have only grown to $1,758. Interest rates were that miserable for most of the last 20 years. The surprising part is gold kept pace with the stocks remarkably well. For an asset that has, historically zigged when stocks zagged, that is a nice performance for the overall portfolio. For some people this is all they need to see. They want to own some gold, find undisclosed and safe storage for themselves and simply keep it as a rainy-day guarantee in case our monetary system hits the rocks. We understand and encourage that strategy – and for some the discussion can stop there feeling that at least a minimal alternative plan has been covered… Others want to see if there is a way to take things a step further to take advantage of the strength of gold. Of course, gold mining stocks can be a levered-up way to take advantage of gold prices going higher. During the run up of gold in the late seventies some investors raked in fortunes as some of the mining stocks rallied many multiples more than the rally in gold prices. We are not against that strategy; however, we are convinced it is a difficult and dangerous one. Mining is a tough long-term investment, and we look at mining stock ownership as largely a shorter-term trade. There are also ETFs (essentially mutual funds) available through a stock trading account that are gold-mining focused.

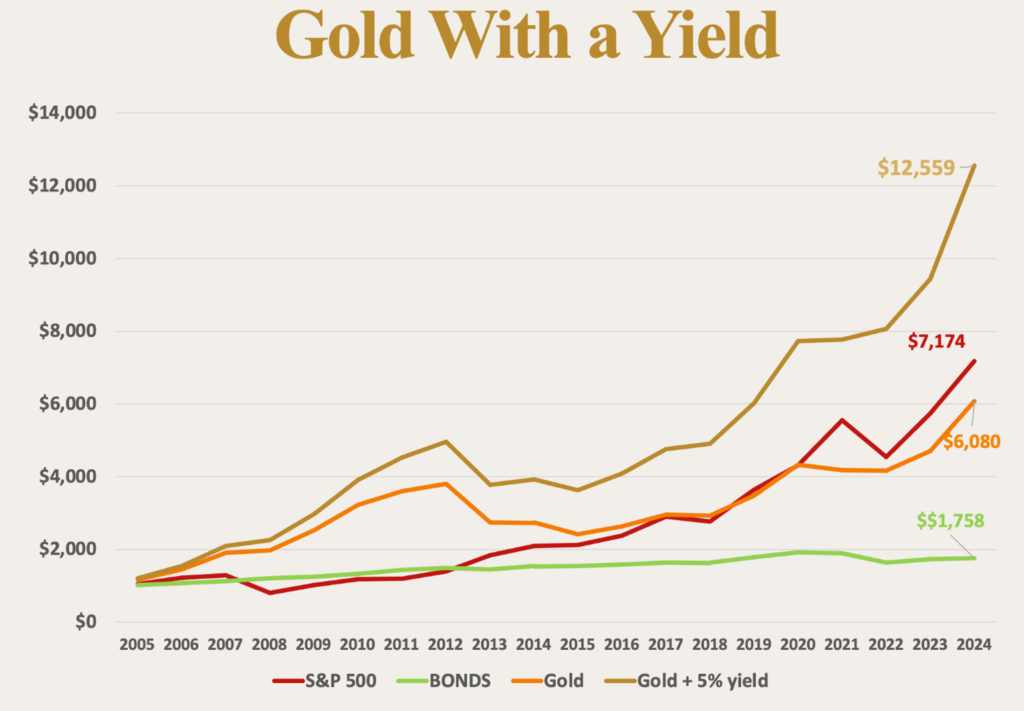

What if there were a way to earn a rate of return on gold much like the bonds we just looked at? What if there were a consistent rate of return on our gold – in gold terms. Take a look at the same comparison chart we just looked at, but with the added assumption that we earned 5% in gold every year on our gold holdings. Not wild interest rate indicating high levels of risk, but just a consistent return in gold on gold… How many US dollars’ worth of gold would we have now?

As you can see, gold with a consistent yield is obviously a compelling concept (somebody call Warren Buffett!!) Gold, with a consistent yield wildly outperformed the S&P 500 over the last 20 years (the chart would be much more dramatic if we had started in the year 2000.) As you can see, the gold-on-gold yield is absurdly better than the dollar-on-dollar yield from the bond world.

Over time gold prices go higher as paper currencies erode in value and if you are getting gold interest on your gold – well, you see the results above. We are not talking about speculative or leveraged positions in gold, but just a consistent 5% yield in gold on gold. But is that available in our financial markets – is it even possible?

There is a growing marketplace of leases and bonds that are denominated in ounces of metal rather than in US dollars or other currencies. Investors deposit gold and silver, and companies borrow the metal for use as capital and pay interest in gold and silver. There are many companies that would rather borrow -and pay interest -in gold and silver terms because they are in businesses that use these metals. This marketplace is booming internationally right now and we at Andorra Capital have created a fund to deploy investments into these metal-based leases and bonds to take advantage of these opportunities. Reach out to us if you would like to learn more.

Regards and good investing!

Greyson Geiler

Market and industry data used in this presentation have been obtained from sources believed to be reliable. However, we have not independently verified such data and make no representation or warranty as to its accuracy or completeness.

Goldrush Yield Fund, LLC is managed by Andorra Capital, LLC, a Registered Investment Advisor. Andorra Capital has a conflict of interest in recommending the Fund to prospective investors. This material is informational only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. The Goldrush Yield Fund is an unregistered private placement and is available solely to accredited investors. No securities commission or regulatory authority has approved or disapproved of the Fund, and there is no obligation to provide investment advice. Investing in the Fund involves risks, including the potential loss of principal. Past performance is not indicative of future results. Any forward-looking statements are based on current assumptions and are subject to change. Investors are responsible for conducting their own due diligence. Please review the Private Placement Memorandum (PPM) for detailed risk factors and consult with legal, tax, and investment professionals before considering any investment. For more information, please contact Greyson Geiler at ggeiler@andocap.com

Financial markets worldwide were met with HUGE volatility last week with trading being halted in the Japanese stocks in particular. The S&P 500 was rocked with the biggest down move in 2 years and the VIX measure of volatility launched to Covid panic levels. By the end of the week markets worldwide had completely calmed down and stock indexes had bounced back. So this brings the question – what was the catalyst of the panic and is everything ok now?

The ”carry trade” is the large driving force of what caused last weeks panic. For years the Bank of Japan has kept interest rates at essentially zero allowing multi-national financial companies to borrow Japanese yen for free. Purchasing assets around the globe – and especially in the American capital markets – is the obvious next step. Traders may buy US Treasuries earning 5% with borrowed money they are paying 0% on. Pretty neat – but there’s more. The value of the Japanese yen vs US $ has been going down for several years. So traders make a margin on the interest rate PLUS they make money as the value of the yen goes down vs the $. Seems like an easy money factory – the problem comes in if the yen rallies back against the dollar. That’s exactly what happened last week. There was a wicked rally in the yen and the “carry trade” got blown out as investors had to close out their positions. There were hundreds of billions of $ that got unwound and the markets responded violently. Here is a picture of how quickly the yen rallied against the US dollar…

Carry traders that had borrowed money in yen terms to buy US tech stocks got wiped out. Things looked so bad on Monday that some people were advocating for an emergency rate cut from the Federal Reserve. Wharton’s Jeremy Siegel embarrassed himself by advocating for an immediate .75% rate cut followed by a minimum of .75% rate cut at the Fed’s September meeting. However, by the end of last week markets had recovered and volatility calmed down. Siegel’s comments didn’t age well and he even had to walk them back at the end of the week. Now of course the question is whether or not the “correction” is over and stocks will continue higher.

Although it is apparent that the bulk of the “carry trade” has been unwound already, we have concerns about the underlying economy that certainly don’t seem to be reflected in stock prices. The labor market is NOT doing well right now – unemployment is on the rise – and the credit markets are showing some worrying numbers. Is the American consumer running out of steam? Has the Fed kept rates too high for too long? Is something broken and will the rate cut in September have any effect? Time will tell…

Don’t forget we have had an inverted yield curve for more than two years. Historically that has been one of the most accurate predictors of recessions – but this anticipated recession just does not seem to manifest. Of course, one of the reasons for that is WILDLY inappropriate government spending (7% of GDP budget deficit for this fiscal year.) That is obviously bad policy but it won’t negatively affect the stock market – rather it is helping support the markets. This pullback in the stock market does not appear to be triggering further meltdowns in our financial markets. As a matter of fact, the yen has started to retrace some of the rally vs the dollar – possibly as traders put the “carry trade” back on– but stay tuned and don’t sell your gold!

Regards and good investing!

Greyson Geiler

Last week was shortened by the holiday and the economic data continued to decline. Financial markets responded with bonds and stocks being bid up in expectation that the Fed would be reducing interest rates soon. Interestingly, June was the first month in four years that there was no central bank on the planet that raised rates! Now we will have to see if the data supports the Fed starting to lower rates. Counterintuitively, bad economic news is bullish for the stock and bond markets…

But an interesting thing to watch is the Mag7 stocks producing the vast majority of stock market performance. That’s right, Apple, Microsoft, Google, Amazon, Nvidia, Tesla and Meta are producing most of the gains and when you see the S&P 500 vs the equal weighted S&P 500…

The divergence you see is the difference between an index calculated with the weighting of the Mag7 and one that has equal weightings across the 500 participants. The S&P would be down on the year if it were not for those seven stocks – and economic data is weakening. That is a concern, but just one indicator…

As usual, now everyone is looking to the Fed to see if they will lower interest rates and keep the party going. The Fed Funds Futures are predicting a 60% chance that the Fed will lower the overnight interest rate by .25% to the 5% to 5.25% range. There is quite a bit of time between now and then so inflation indications will be on everyone’s radar. One of the concerns that we have looking forward with inflation in mind is the recent strength in crude oil – so that will stay on our radar. Massive government spending is causing a “stickiness” to inflation and even Fed Chair Powell is suggesting inflation won’t get back down to 2% any time soon. Maybe the Fed will lower .25%, but don’t hold your breath for drastically lower rates.

The financial markets are obviously pricing in lower interest rates in the near future – at least to a small degree. The short interest in most of the stock market has declined and the VIX – which is a volatility indicator – shows that most people are not concerned about the stock market selling off. That may be a short-term concern. Just a few companies representing the entire growth in the stock market is a medium to long-term concern. Government job openings are more than 100% of growth in the labor market. That’s right – private sector employment is declining. That may be another temporary situation, but if it continues it is yet another long-term concern to pay attention to! Stay tuned…

Last week the Bureau of Labor Statistics reported that in May the US unexpectedly added a staggering 272K payrolls, which was 50% higher than the consensus forecast of 180K and 14K more than the highest Wall Street estimate (258K from Regions Bank). Wall Street really didn’t see this one coming as JP Morgan and Goldman were both below consensus average at 150K and 165K respectively. Wages were reported as going higher as well which indicates a strong labor market – but keep in mind, labor is one of the “trailing” economic indicators. The response from the bond market was a selloff as hopes of a near-term interest rate cut diminished. Stocks sold off a bit as well but held their own as the day went on.

Strangely the unemployment rate reportedly rose from 3.9% to 4% which doesn’t make sense when the jobs report was so strong. Looking under the hood of this report, things are looking much less than rosey. When we aggregate the performance of the labor market over the last few years, we get a better understanding of the dichotomy of the economic reports from the media and the significantly different view from financially struggling Americans.

The first thing further analysis of the jobs report uncovers is the difference between the BLS Establishment and Household surveys. The establishment survey counts payroll jobs while the household survey counts employees. So when you have people taking second and third jobs, one survey can look strong and the other can look weak. Now we have the biggest delta ever recorded between these two surveys – the chart being curtesy of ZeroHedge…

…and if that weren’t bad enough, we now compare data of American born employment and foreign born now working here – and the picture gets worse. Looking at just the past year, native-born workers have lost 668K jobs while foreign-born workers – and they are largely illegal immigrants – have gained 934K jobs. When you look at a chart of the last five years it is fairly daunting…chart also from ZeroHedge.

The number of jobs occupied by people born in America has not increased in FIVE YEARS!! This is going to turn into a huge political issue if it is not already. We have huge border issues and if that recession finally hits that so many people have been anticipating, the political front could get dicey because many Americans feel left behind by the economy that we keep talking about hanging on surprisingly well.

Last week we mentioned that the restaurant industry is looking less than robust with some big chains looking tepid or worse with some potential bankruptcies pending. This week we want to show you some of the retailers that are looking pretty bad as well. Retail stores are being shut down at a staggering rate all over the country.According to the Daily Mail, nearly 2,600 store closings were announced during the first four months of 2024…Big names including Macy’s, Walmart, Walgreens, Foot Locker and 7-Eleven have all said they are closing shops. But discount stores like Family Dollar and bankrupt 99 Cents Only have been worst hit, as have drugstores like CVS and Rite Aid. If we stay on the pace that we are on, the total number of stores closed in 2024 will be nearly 40 percent higher than the total number of stores closed in 2023. This isn’t a booming economy to say the least – which brings us to our last data point for this week – credit numbers.

According to the Federal Reserve’s monthly consumer credit report, in April total consumer credit rose $6.4 billion, far below the median estimate of $10 billion, but more notably, the March number was shocking revised from $6.3BN to a negative $1.1BN, the biggest drop since last August. However, the real shocker in today’s print was the April revolving credit print, i.e., credit card debt. At -$0.5BN, it followed last month’s puny $1.7BN, and was the first negative number since the covid crisis! in the six years prior to the covid crash, the US had recorded just 5 months of negative prints, and all tended to precede major drawdowns in the economy. The resilient American consumers appear to be reeling the spending in and we are raising our concern levels from an investment perspective. We certainly aren’t predicting an imminent market collapse, but the divergence of some of the numbers we have shown today are not sustainable indefinitely. Stay tuned.

We don’t have any empirical evidence, but our intuition is that a survey of economists guessing forward from 2020 would have predicted financial market doom with an overnight interest rate of 5.25%-5.5% in the middle of 2024. The economy and financial markets held up to these higher interest rates and have, in fact, performed amazingly well. The bond markets have not collapsed, the US dollar is holding quite firmly against other major currencies, the stock market is near all-time highs and unemployment is less than 4%. We can all speculate as to how and why, but the reality is that things in general are WILDLY better than one would expect considering the circumstances. The recession that many economists have been predicting hasn’t materialized and the big question is, of course, will things continue to hold strong?

At least some of the performance of financial markets can be attributed to expectations that the Federal Reserve will be bringing interest rates back down – asset prices in general will be higher with lower interest rates, all other things being equal. The Fed politically has to have a handle on inflation to justify lowering interest rates. Part of getting a handle on inflation is the Fed succeeding in demand destruction. This is a deflationary force combatting the inflation that the Fed created. So, strangely, we are back to the dichotomy of a few years back where bad economic information is good for the price of bonds and stocks. Bad information has been coming out and this week is no exception. Here are some recent reports:

The manufacturing ISM (Institute for Supply Management) slipped again in May and was below expectations.

OPEC has recently agreed to extend its production cuts of crude oil until 2025 as outlook for demand is soft.

A restaurant collapse is showing a weaker middle-class consumer. Applebee’s is closing 35 more stores, Boston Market and Red Lobster are contemplating filing for bankruptcy protection as sales struggle. Even McDonalds is feeling the heat and they are about to launch a $5 meal-deal for a promotional month to attempt to juice sales.

The widely tracked University of Michigan survey of consumers released last week showed consumer sentiment leaking to the lowest levels in six months.

The Chicago PMI numbers for May were a train wreck. This is the fifth month of contraction for the index – well below expectations. This is a widely watched economic indicator and is one data point of an economy starting to struggle under tight monetary conditions from the Fed.

Government spending is the one spot where we can see strong growth. The Federal government has already rung up a $1.4 trillion deficit putting it on pace for a $2 trillion deficit. This is a 7% budget deficit when the economy is supposedly doing well. What happens if the economy clearly goes into a recession?

The government filling some of the gap with deficit spending is the part that worries us the most. The economy has held together well under higher interest rates, but we are stacking a public debt load together that will have to be dealt with at some time. Here is a visual of the ever-increasing debt load…

Again – not only is the debt load going higher, but the interest rate is staying higher for longer than anticipated. So, the interest owed on all this debt is now at an annual run rate of about $1.1 trillion…

Fed Funds Futures are trading with a more than 50% probability that the Fed will lower interest rates by the September meeting. We don’t think a .25% move really means anything to the economy – we are just hoping the Fed doesn’t really break something and get forced into drastic interest rate changes. With the geopolitical risks out there, we may be asking a lot…

Not to sound like a broken record, but the economy and financial markets are holding together well considering the headwinds out there. A recession DOES NOT appear to be in the works – but some indicators look a little weak in the short term. As leveraged as the system is that could start to domino. In the long run we are nervous about debt loads, but there does not appear to be an imminent reckoning. Stay tuned…