by Greyson Geiler | April 29, 2024

The dichotomies in the financial world continue to manifest with several contradictions simultaneously occurring and financial commentators scratching their heads in an attempt to make sense of things. Earnings season is in full steam this week – and looking positive – but right after GDP data seriously disappointed last week showing a lackluster economy. The commercial real estate market appears to be a disaster waiting to happen – yet continued high interest rates don’t seem to facilitate any meaningful meltdown. Fiscal deficit and total US debt numbers are at nightmarish proportions and rocketing higher – yet the US Dollar is strong and is trending higher…

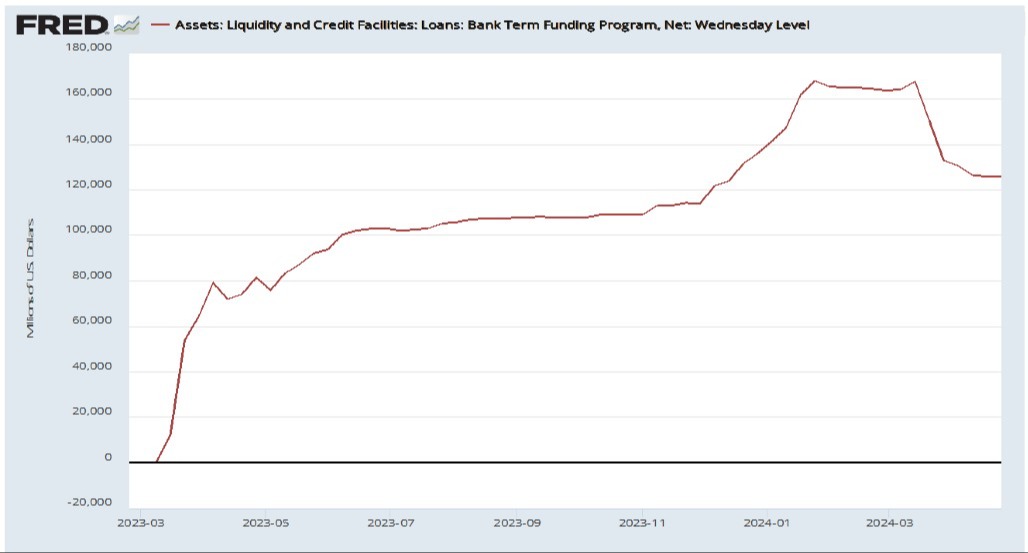

Yet another example – It has been almost precisely a year since the failure of First Republic Bank the aftermath of which was the FDIC gutting the carcass of the bank and “selling” the filet to JP Morgan Chase. The financial conditions that led to the bank failure (including an inverted yield curve) have not eased and yet the banking sector has held together pretty well – until last week. Now we have Republic First Bank in Pennsylvania being closed by regulators. Although this bank is quite small compared to Silicon Valley Bank and First Republic, which went belly-up last year, one has to be concerned about the banking environment and whether or not we will see more bank failures. The big question is whether or not the ending of the Bank Term Funding Program is going to be a catalyst for more such failures…

During the Covid “pandemic” interest rates went to all-time lows in the US. The ten-year treasury traded at a yield of less than .6%. With interest rates so low, of course note and bond prices are high. Many of the assets bought by banks such as Silicon Valley Bank were priced very high, and then came down as the Federal Reserve raised interest rates. So essentially, the Fed caused the problem for banks – they lowered interest rates taking bond prices very high, and then raised interest rates pushing bond prices back down. The yield curve inverted, and banks were in big trouble. In response to this, the Fed created a lending program in which banks could borrow against those under-water bonds at FULL PAR VALUE. Although many banks didn’t participate in this program because it may have strained capital requirements, banks that were in dire straits had a life raft and about $160 billion was loaned out through this program. Now it is coming to an end and the loans are due – here is a chart of the outstanding loans…

Could the ending of a small program like this be a catalyst for another round of bank failures? If $125 billion in loans has to get repriced or restructured across the multi-trillion-dollar banking system?

Could that really be what sets off more problems in our monetary system? Stay tuned…

In the meantime, some of the indicators of a change in the monetary landscape have been sending up red flags. Specifically, the Japanese Yen has sold off to multi-decade lows. Here’s another chart to take a look at:

This is another indicator to keep an eye on. As we have said for some time – the Japanese Yen is the “canary in the coalmine” for the world central banks’ continual strategy of printing money when their economy doesn’t perform perfectly. The problem won’t be the Yen going lower, if the problem comes it will be the Yen ACCELERATING lower. That would mean that the 5th largest economy in the world is in serious trouble.

As for now the US capital markets and economy are still holding together well considering some of the aforementioned concerns. This is a busy week of earnings and economic reports so we will reevaluate accordingly.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | March 25, 2024

The financial markets in the U.S. never stray very far away from the question of what the Federal Reserve is going to do with interest rates and this week is no different. Stock and bond markets are currently pricing in the Fed not raising interest rates until the June meeting.

However, some economic numbers are weakening will likely cause more speculation that interest rates may come down at the next Fed meeting in May. Asset markets (stocks and bonds) have been holding together remarkably well for months now – but some indicators are starting to show some real complacency and too much comfortability in the markets. This is when we look for things that could go wrong and try to find cracks in the dam. If the economy hits large challenges, the Fed will have to lower interest rates in support as they have historically done. Here are some concerns we see going forward that we think could be indicators that the Fed will have to shift…

- The VIX is pinned near five-year lows. This is a volatility or “Fear” indicator and is a calculation of how much insurance fund managers are buying to hedge the downside of their stock portfolios. When this number is low, it indicates people aren’t afraid of the stock market going down. When few people are looking for problems, that’s when they tend to happen – and a big move down in stocks could get the Fed to lower rates early.

- The February PPI (Producer Price Index) report came out much hotter than expected. This means that inflation isn’t going away quietly as quickly as the Fed has indicated they thought it might. Putting the inflation genie back in the bottle is not easy – as history has proven to us – and we don’t imagine that general inflation will revert back down to the 2% target anytime soon. This complicates how the Fed is going to manage the interest rates going forward.

- Government spending is horrific. We complain regularly in this post and we are doing it again today. Projections of budget deficits from the Congressional Budget Office don’t look accurate to us – so we just have to do the math ourselves. Since the beginning of the fiscal year (Oct 1) the U.S. govt debt has increased $1.411 trillion according to the treasury’s own website. The math is easy – double that for the rest of the year and you are at $2.822 trillion. Our economy is $28 trillion – so we are running a 10% budget deficit???? Let’s hope tax receipts are going to change these numbers a bit in the next few months because normalizing budget deficits like this is banana republic kind of stuff – not what the stewards of the world’s reserve currency should be doing. Financial markets are being distorted by this reckless spending as well and only time will show us exactly how.

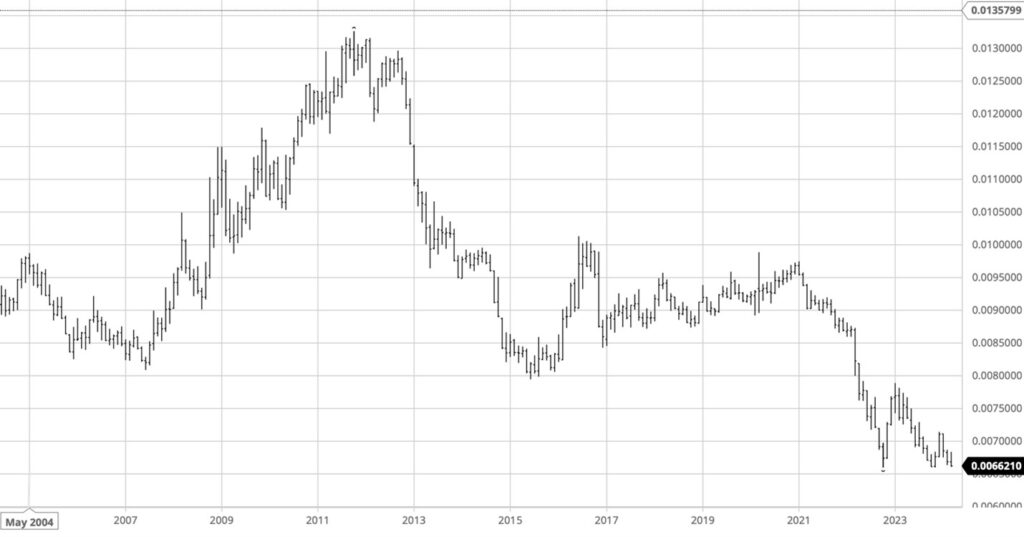

- The Japanese Yen. For going on 10 years, we have talked about the Yen as the proverbial canary in the coal mine of the world’s monetary system. As much as we complain about our Federal Reserve distorting capital markets, the Bank of Japan is WAY worse. They create Yen and buy assets in the Japanese markets to a wildly greater degree than the Fed does in the U.S. Japan is the world’s 4th largest economy by some measures and if the dam breaks and the value of their currency melts down then we need to be on guard. Take a look at a picture of the value of the Japanese Yen vs the U.S. dollar over the last 20 years…

As you can see the Japanese Yen is at the lowest valuation it has been against the U.S. dollar in recent memory. We aren’t afraid of the yen going lower – we are afraid of it completely melting down. This picture suggests the Yen is going lower AND the ingredients are in the pot for a serious meltdown. Let’s hope that doesn’t happen but understand that if it does there will be implications for the whole world’s economy and monetary system. The Fed would likely have to pour huge resources out towards Japan to help hold things together and no one knows how that would look logistically – so stay tuned…

We continually look for potential roadblocks in the world’s economy even though things look quite rosy right now. The economy has held up to higher interest rates much better than most would have expected – which is obviously good news. However, we can’t get complacent and we have to keep on the lookout for the challenges – things that could cause the Fed to lower interest rates sooner and/or more than expected.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | January 8, 2024

We have mentioned in the past how we are skeptical of the reliability of some government numbers relating to the economy that we have seen over the last few years. This is not a political statement. This is simply an opinion after watching governmental numbers and reports and the corresponding responses by the financial world for decades. Some of the most influential reports deal with employment numbers for a myriad of different reasons. Historically employment numbers can tell a lot about the health of our economy. More recently, people make short-term trading decisions driven by employment numbers in the near term assuming that the strength or weakness of the labor market will be very influential on whether the Federal Reserve raises or lowers interest rates. This will then reflect in the value of asset prices as lower interest rates tend to make such prices go up and conversely higher interest rates make asset prices go down. The reporting of labor market numbers from the BLS (Bureau of Labor Statistics) over the last year or so is appearing to be more of a political tool than an accurate description of the state of the employment marketplace. The December payroll numbers reported last week were no exception…

As a matter of fact, from this chart you can see that ten of the last eleven jobs reports have been revised substantially lower. Along with the December numbers which came out quite drastically higher than expectations, also came revisions lower of both October and November numbers. Someone is clearly manipulating the data – and we are not the only ones pointing this out!

Even if the December numbers aren’t revised lower in the months to come, looking under the hood of this report does not show a strong job market. The first concern of ours is that the government was the number one provider of “new jobs” in this report followed by jobs in travel and leisure. Government hiring does not engender a trustable economy and there are other cracks in the dam so to speak referencing current job statistics. When you look at part – time employment, the numbers of people with multiple jobs has rocketed to all-time highs. Full-time employment numbers haven’t rebounded since Covid with anything close to that sort of strength!

Whatever the current administration is doing to alter the true picture of the labor market for short term headlines, the reality is that things are starting to weaken. Of course, that begs the question as to whether or not the Federal Reserve will lower interest rates at the March meeting. With a stronger than expected headline number on this employment report the probability of lower rates is waning. The stock market has performed well over the last couple months and actually overextended the Santa Claus rally a bit. The rally was at least partially fueled by expectations of lower interest rates. That may not materialize until we get weaker economic data. Stay tuned for an interesting bad-news-is-good-news dichotomy as some investors hope economic numbers weaken so that the Fed will lower rates in order to bolster asset prices. Right now, we are seeing weakening economic numbers but not to the degree that would justify the rate cuts from the Fed that are already baked into our financial markets. So, will the administration keep skewing numbers for the image of a robust labor market in an election year? There is plenty of anecdotal stories about administrations of the past all the way back to LBJ that have tried to lean on the Fed to lower interest rates. It will be interesting to see if this administration changes horses and starts down the same path.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | December 18, 2023

The Federal Reserve pivoted off of “higher for longer” with regard to interest rates at this week’s meeting. Chairman Powell came into the Fed meeting being quoted as recently as December 1 saying “We are prepared to tighten policy further” implying that they may not be done raising interest rates. He shifted at the Dec 13th meeting saying that rates have peaked, and the Fed is looking at three rate cuts coming in 2024. Wait, what? That is quite an adjustment in less than 2 weeks and the asset markets responded violently. The interest rates on the longer end of the curve came crashing down and the Dow Jones Industrial average rocketed to a new all-time high. The move higher in stocks and bond prices was accelerated by short-sellers that got caught and had to buy back in a frenzy. The 10-year treasury bond yield – which printed over 5% just over a month ago in October – crashed down to 3.9% and so far hasn’t bounced. That is quite a remarkable move. Why would the Fed change verbiage so drastically? Is this a rerun of the fall of 2018 when the Fed tried to raise rates and immediately backed off because of warning signals from the overnight repo market? Is the Fed seeing something in the banking system that is prompting them to back off the “higher for longer” mantra? The big banks still have north of a half a trillion dollars in unrealized losses in their bond portfolios. Is the Fed trying to rally those prices to avoid banks having to realize those losses?

The long-awaited recession still hasn’t materialized in the U.S. but parts of Europe are clearly in a recession. Interest rates are still sitting much higher than anyone reasonable would have thought that the world’s economies could have stood up to. It appears that we have come to the conclusion of that pleasant surprise, however as the Fed is strongly hinting at lower rates quickly. Now we are wondering if lowering interest rates can help maintain a stock market rally considering there are likely some downturns upon us in the economy. Can the Fed truly engineer a soft landing of the economy considering the wildly volatile policies that they have implemented over the last three years? Or are unintended consequences of their actions inevitable?

We have been mentioning that we expected a Santa Claus rally in stocks – but last week even outdid our expectations. If you have been nervous about your stock portfolio being too risky, this short covering rally is providing a nice escape point to sell some positions. Our guess is that asset prices will probably continue higher for the short term but that is just a guess and the Fed may actually be spooked by something serious that could start weighing on stock prices.

One indicator worthy of note is the quick move in 30-year mortgage rates – take a look…

We keep hearing about pending doom in the residential real estate market but mortgage rates coming down would clearly stem some of the pain in that market. We don’t need to return to all-time low mortgage rates to support real estate – there is simply a shortage in homes in this country. The looming danger in refinancing needs for corporate bonds would also be ameliorated by the slide lower in interest rates. There are many things that could be restimulated by interest rates coming back down and we should remain cautiously optimistic that 2024 can get started without any serious setbacks economically. At the same time we should remain forever vigilant as the Federal Reserve has engendered an unstable interest rate system with their shenanigans specifically in the last three years.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | December 11, 2023

Analyzing the current performance of the entire U.S. economy is clearly a subjective endeavor. There are some obviously very good things going on in some manufacturing and tech industry spaces. On the other side of the coin some industries -such as residential home mortgages – are really struggling. One thing that is not subjective is the price change of the S&P 500 and that just made a new high for 2023 and may break out to the upside for that proverbial “Santa Claus Rally.”

We mentioned a few weeks ago that the ingredients were in the pot for the market to continue higher – so today we will show you some of the fundamentals that could potentially throw a wrench in Santa’s seasonal gift giving…

Transportation companies are clearly the life blood of the economy moving products from producers to consumers. Right now, transportation companies are not reporting the best of times. In fact, earlier this year, things were pretty grim as bankruptcies and layoffs piled up. The number of authorized interstate trucking fleets in the U.S. declined by nearly 9,000 in the first quarter of 2023, according to federal data analyzed by Motive, a fleet management technology company. Several midsized fleets have already shuttered this year, including Florida’s Flagship Transport and North Carolina’s FreightWorks Transport. Major freight brokerages have laid off thousands of employees in 2023. Although the Dow Jones transportation Average has had quite a nice bounce off of its October lows, it is still about 9% off of its high point from earlier this year. Historically, market pundits have been nervous of a stock rally in which the transportation stocks weren’t participating. The trannies have a lot of work to do to catch up to the rest of the market.

As important as the transportation sector is, of course we must be worried when we see the challenges that the banking system is having. Of course, The Fed had to bail the whole system out in the first quarter of this year when Silicon Valley Bank went belly up. Since then, the Fed has allowed banks to borrow against some of the bonds that they have which have sold off drastically in price. We will see if this is enough to keep things liquid – but at the same time deposits (checking and savings accounts) have fled banks for greener pastures (money market funds) so banks are starving for deposits. Wells Fargo bank just shut down 13 locations in one week and Citigroup is announcing widespread layoffs as part of a “restructuring.” Of course, we don’t know if that just the current low-light reel of the banking sector or if that is a systemic issue. The largest financial ETF – XLF – has aggressively bounced off of its October lows. It has yet to make a new high for the year but may be set to do so along with the S&P 500 if some of the above listed negativity stays in the rear-view mirror.

For our friendly chart of the week, we will show you what concerns us for the long-term. This is a macro-economic indicator and clearly has nothing to do with whether or not a fat guy in a red suit is going to be flying around in a sled this year handing out gifts. This is the big picture item that has us up at night hoping things don’t turn nasty in the monetary system. This is the U.S. government’s budget deficit as a percentage of GDP for the last 20 years…

This represents how much more our government spends vs how much it takes in every year as a percentage of our total economy. To call this absurd is an understatement. You can see that the budget deficit during Covid was nearly 15% of our GDP. Today it is still north of 5%. An entertaining sidenote comes to us from the European Union. At the onset of that that “organization” it was mandated that EU countries could have a maximum budget deficit of 3% of their GDP. The U.S. isn’t involved in that agreement, but it is a comical reference point as you can see that there was very little time in THE LAST 20 YEARS that the U.S. wasn’t north of 3% of GDP with our budget deficit. Consequently, the national debt of America has TRIPLED in the last 15 years to a mind-boggling $34 trillion. Of course, the rocketing higher of interest rates that the U.S. government is paying on that debt exacerbates the situation and the math has become flat-out intimidating. Will the Fed have the flexibility to keep interest rates this high for very long considering this interest situation? Interest on the national debt will be well north of $1 trillion for 2024. We are nervous about that in the long run, but are guessing that reindeer hooves will be heard on our rooftops in the next couple weeks.

Regards and good investing,

Greyson Geiler