In a rapidly evolving global financial environment, gold is reasserting its role as a pivotal asset. Recent developments in China and the United States are accelerating its prominence within the international monetary system. Two key events—China’s offshore yuan-to-gold conversion initiative through a Hong Kong depository and U.S. Treasury Secretary Scott Bessent’s February 2025 announcement regarding monetizing the U.S. balance sheet—underscore gold’s increased relevance in tackling macroeconomic challenges and redefining global trade dynamics.

China’s Yuan-to-Gold Conversion in Hong Kong

In late June 2025, China launched its first offshore gold vault in Hong Kong, accompanied by yuan-based gold contracts on the Shanghai Gold Exchange. This initiative permits trade partners running a surplus with China to convert yuan directly into physical gold at prevailing market prices, entirely bypassing the U.S. dollar. This move, widely discussed on X, is a direct challenge to the dollar’s dominance in global trade and to Western-centric gold pricing systems.

The rollout leverages blockchain technology, using platforms such as mBridge to enable instant settlement. It positions gold at the core of a nascent financial framework and could potentially lay the foundation for a BRICS-based, SWIFT alternative. This effort is consistent with China’s broader renminbi (RMB) internationalization agenda, though notable constraints remain: strict capital controls and a tightly managed exchange rate.

China’s foreign exchange reserves exceed $3.3 trillion (excluding Hong Kong’s $496.8 billion), with an estimated 50–60% in dollar-denominated assets. The Hong Kong vault offers a path for diversification away from dollar reliance—particularly in light of geopolitical risks, such as the Western freeze of Russia’s $300 billion reserves in 2022. Direct yuan-to-gold conversion not only increases the yuan’s utility as a trade settlement currency but also reaffirms gold’s credibility as a store of value during times of economic uncertainty. Notably, China’s economic slowdown is driving up domestic gold demand, as observed in real-time commentary on X.

While this development may reshape global trade by providing an alternative to dollar-based transactions, especially for Belt and Road Initiative partners, the yuan’s limited capital account convertibility and managed exchange rate mean that dollar reserves remain vital for maintaining the perception of stability. Nevertheless, the Hong Kong vault marks a meaningful pivot—framing gold as a hedge against currency risk and as a mechanism for decreasing reliance on the U.S. financial system.

U.S. Treasury’s Gold Revaluation: Monetizing the Balance Sheet

Meanwhile, the United States is reevaluating gold’s place in economic policy. On February 3, 2025, President Donald Trump signed an executive order to establish a sovereign wealth fund, followed by Treasury Secretary Scott Bessent’s announcement: “We’re going to monetize the asset side of the U.S. balance sheet for the American people.” Delivered from the White House, this statement has sparked speculation that the government could revalue its 8,133 tonnes of gold, currently shown at $42.22 per ounce (statutory value), totaling $11 billion. At present market prices—roughly $3,300 per ounce—these reserves would be worth over $863 billion, representing a substantial potential funding source for the Treasury.

Revaluation could allow the Treasury to increase its General Account at the Federal Reserve without liquidating gold holdings. This would be achieved through an accounting change similar to that outlined in a 1974 Federal Reserve paper—by increasing the value of gold certificates held by the Fed, thereby crediting the Treasury with the gain. The maneuver could lower the U.S. debt-to-asset ratio and create greater fiscal flexibility amid projections of a $6.5 trillion federal debt increase tied to proposed tax and spending legislation.

However, experts caution that fully exhausting the gold revaluation account could leave the balance sheet under-collateralized if gold prices fall below the new statutory level. This risk may prompt the establishment of a minimum gold price—edging the system closer to a gold standard.

Bessent’s remarks, alongside the executive order, indicate a pragmatic effort to leverage national assets and manage fiscal challenges. Gold, once dismissed as a “barbarous relic,” is being reconsidered. Francisco Blanch of Bank of America argues that revaluation would amplify gold’s status in the monetary system and boost market confidence in the metal. That said, Bessent has tempered expectations, telling Bloomberg TV he has “no plans to visit Fort Knox,” reaffirming that the gold remains secure. The approach comports with broader objectives to preserve the dollar’s reserve currency status and address trade imbalances, as ongoing tariff negotiations with China demonstrate.

A New Era for Gold?

The convergence of China’s yuan-to-gold initiative and the U.S.’s gold revaluation signals an evolving, multipolar financial world. For China, gold strengthens the yuan’s international standing and curtails dollar dependence as the economy faces structural challenges. For the U.S., monetizing gold reserves provides fiscal breathing room without market upheaval, while maintaining dollar predominance.

These shifts prompt important questions: Will China’s Hong Kong vault accelerate dedollarization by encouraging trade settled with yuan-backed gold? Will the U.S. embrace gold revaluation as a fiscal tool, hinting at a partial return to gold-backed policies? While a full gold standard remains unlikely, both countries’ actions show gold is emerging from its historical stigma to play a critical role amid economic uncertainty.

As U.S.-China trade tensions continue to influence global markets, gold’s neutrality and intrinsic value reinforce its appeal as an anchor asset. Despite ongoing rivalry, both countries demonstrate a growing acknowledgment of gold’s enduring relevance in 21st-century finance.

Earning a Yield on Gold

Gold is a cornerstone of a balanced portfolio—and now it’s again a productive asset. Over the past decade, a transparent marketplace for gold leases and bonds has emerged, enabling institutional and private investors to generate interest paid in ounces of gold. While central and bullion banks have engaged in gold leasing for decades, the market is now open and more standardized for private participants. As a result, gold is once again being deployed as a capital asset and generating yield, rather than simply remaining idle. Lease and bond volume is growing parabolically, and our fund is at the forefront of this renaissance in gold. For more information, please reach out.

Regards, and good investing.

Greyson Geiler Lead Portfolio Manager

Market and industry data used in this presentation have been obtained from sources believed to be reliable. However, we have not independently verified such data and make no representation or warranty as to its accuracy or completeness.

Goldrush Yield Fund, LLC is managed by Andorra Capital, LLC, a Registered Investment Advisor. Andorra Capital has a conflict of interest in recommending the Fund to prospective investors. This material is informational only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. The Goldrush Yield Fund is an unregistered private placement and is available solely to accredited investors. No securities commission or regulatory authority has approved or disapproved of the Fund, and there is no obligation to provide investment advice. Investing in the Fund involves risks, including the potential loss of principal. Past performance is not indicative of future results. Any forward-looking statements are based on current assumptions and are subject to change. Investors are responsible for conducting their own due diligence. Please review the Private Placement Memorandum (PPM) for detailed risk factors and consult with legal, tax, and investment professionals before considering any investment. For more information, please contact Greyson Geiler at ggeiler@andocap.com

Income is an important part of any investment portfolio, whether we are referring to individual investors spending their savings in retirement, institutional funds trying to continually compound consistent growth or any investor class in between. Over the last few decades, the #1 complaint about owning gold has been that it’s not a “producing” asset. Legendary investor Warren Buffett has made multiple remarks through the years alluding to gold being a pet rock, or that if you own an ounce of gold for eternity, you will own only an ounce of gold for eternity. Since gold became available for individual investors in 1975 the price has had a 5.68% Compound Annual Growth Rate (CAGR) according to Macrotrends—which is strangely similar to the average of the interest rate of the 10-year U.S. Treasury Note (5.9%), also according to Macrotrends. Of course, 10-yr treasuries pay a coupon – simple interest rate, so we are comparing apples to oranges a bit—but the point is that just the price increase of gold has kept up with some traditional investment strategies since it became available in 1975…

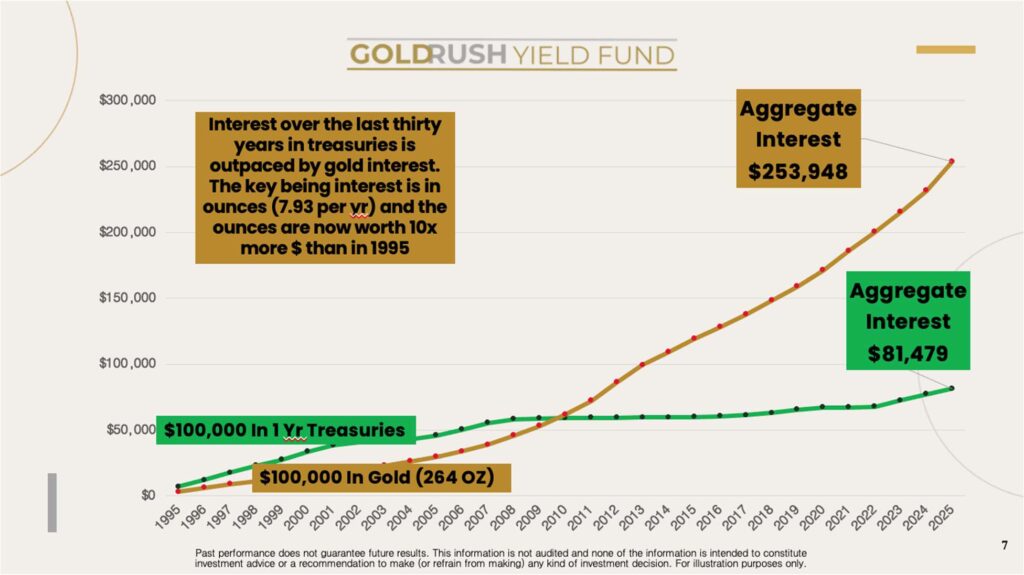

But now we are in an investing environment where things are changing, especially with regard to investing in gold. Gold is coming back into the monetary system and is being deployed as a capital asset! In the last decade, a transparent marketplace has emerged of leases and bonds that are denominated in ounces of gold and silver rather than in U.S. dollars. Once again there is an interest rate on gold! The interest earnings of these leases and bonds are also a percentage of the original investment—just like the treasuries discussed above. However, the percentage is a calculation of the number of ounces of principle, not the dollar value of the ounces. This is where the rubber really meets the road. Let’s take a look at a chart of a comparison over the last 30 years of fixed income between gold leases—getting interest paid in ounces of gold—and ONE YEAR treasuries to compare the same duration as the gold lease marketplace. We will hypothetically invest $100,000 in one yr treasuries, withdraw the interest as income and keep rolling the principal into one yr treasuries at the historical rates that occurred. The comparison is buying $100,000 of gold (264 ounces as of Jan of 1995) withdraw the OUNCES of interest (7.93 ounces per year,) spend the dollar value of the ounces of interest and continually roll principal into hypothetical one year gold leases at a constant 3% interest rate.

The comparison is quite staggering with the DOLLAR VALUE of the aggregate gold interest earned being more than triple of that which treasuries paid. In the mid 1990s, there was a decent interest rate for treasuries. But because of the “dot bomb” in 2001—and then especially after the 2008 financial crisis—the Federal Reserve kept interest rates artificially low. Consequently, the returns on treasuries have been anemic for decades on the aggregate. The annual income in our example for much of the 2010s was a pathetic .15% or so equating to about $150. Then we compare treasuries to leasing gold. A thirty-year interest rate is hypothetical, but for the last decade, the marketplace of one-year gold leases available to private investors has averaged about 3% (right now many of these leases are paying 4%). When you factor in how much the price of gold has gone up, the 3% (7.93 OZ per year) is now income of over $20,000. That’s a pretty good annual return considering the size of the original investment. Comparatively the income from the treasury is now about $4000 which isn’t good – but at least better than 10 years ago… Traditional or conservative investors might argue that treasuries are a better investment because they are risk-free. However, we would point out that the U.S. government has restructured its debt twice in the last hundred years casting some shadow on the “risk free.” In 1933, Roosevelt devalued the dollar against gold, changing it from $20.67 per ounce to $35 per ounce giving a HUGE haircut to anyone who owned some of the $22 Billion of U.S. debt. Then in 1971, Nixon took the U.S. off the gold standard all together, which wildly repriced the dollar lower for a second restructuring of U.S. Debt. Sadly, since then, Congress has been on absolute bonanza of reckless spending, rocketing sovereign debt into the stratosphere ($36 Trillion). The point is that while there isn’t any risk that you won’t get your dollars back when you own U.S. debt, but there is a question of how much those dollars be worth…

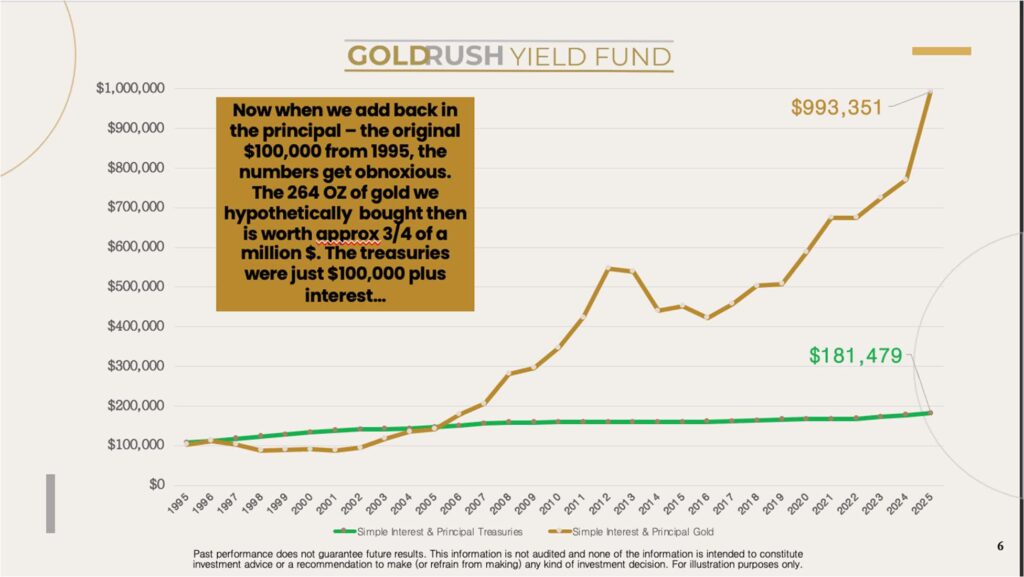

Now, let’s take a look at the second part of the equation—the value of the principle of the original investment being added in to the aggregated interest earned over the 30-year stretch. Again, these are hypothetical results, but if you bought $100,000 of gold in 1995 it would be worth about $750K as of January 2025. Of course, the value of the treasury note being rolled in our example is still just the original $100,000 from 1995…

The performance of gold over treasuries during this 30-year window is more than five to one, and this is with simple interest being withdrawn. That is not a trivial amount of time. We would need another chart to show the performance if interest were rolled back in, compounding over thirty years. Gold out-performs more than eight to one in that scenario…

Obviously, assets of different types can outperform treasuries over certain periods of time. A stock or real estate portfolio might show similar multiples of overperformance. Our objective as investors is to design resilient portfolios that can withstand various economic scenarios rather than depending on one specific asset class. Gold is more than a hedge – it is a necessary part of this resilient portfolio. It is not issued by a central bank and historically it has been a stabilizer during turbulent adjustments within monetary systems at the end of credit cycles. However, in the past to realize any part of the portfolio protection that gold provided – an investor had to sell gold returning them to the fiat currency issues they were trying to avoid! Now we can get income in ounces to protect against the printing/debasement of the world’s paper currencies and investors don’t have to time buys and sells within gold price movements to consistently realize gains! Our Goldrush Yield Fund is a yield on gold by owning the physical and deploying into leases and bonds for an INCOME IN OUNCES!

Regards and good investing!

Greyson Geiler

Market and industry data used in this presentation have been obtained from sources believed to be reliable. However, we have not independently verified such data and make no representation or warranty as to its accuracy or completeness.

Goldrush Yield Fund, LLC is managed by Andorra Capital, LLC, a Registered Investment Advisor. Andorra Capital has a conflict of interest in recommending the Fund to prospective investors. This material is informational only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. The Goldrush Yield Fund is an unregistered private placement and is available solely to accredited investors. No securities commission or regulatory authority has approved or disapproved of the Fund, and there is no obligation to provide investment advice. Investing in the Fund involves risks, including the potential loss of principal. Past performance is not indicative of future results. Any forward-looking statements are based on current assumptions and are subject to change. Investors are responsible for conducting their own due diligence. Please review the Private Placement Memorandum (PPM) for detailed risk factors and consult with legal, tax, and investment professionals before considering any investment. For more information, please contact Greyson Geiler at ggeiler@andocap.com

Accumulating wealth involves a combination of strategies that focus on increasing assets and investments over time. For different people, the end objective can be drastically different. A pension fund manager is going to have a completely different perspective than a young family who paid off bad debts and are now investing for their future. Everyone wants – all other things being equal – to have more money. However, there are many variables considering investor objectives that can affect investment strategy including risk tolerance, time frame for achieving objectives, liquidity needs among many other things. One variable that fits into nearly every investor’s planning strategy is diversification. No one wants “all of their eggs in one basket” so investors of all stripes attempt to have different investments to reduce volatility of the portfolio as a whole. The old-school retirement planning strategy of the 60-40 bond to stock ratio had a pretty good run from 1980 to 2008. That obviously correlated with a window of time where interest rates were going down across the world. Now the situation is different as interest rates went significantly higher a few years ago and are now trending sideways.

As much as investing changes with computer technology and central bank currency creation at will some things stay the same. “All-in” is a strategy in no-limit hold ‘em poker than many people are entertained by but few view as a viable investment philosophy. As a matter of fact, some of the most famous investors in recent history have declared that a true diversification is “The Holy Grail” of investing. Recent aggressive selloffs in the US stock market – where the bond market DID NOT rally higher have left some investors wondering if the whole monetary system and corresponding asset correlation relationships are changing…

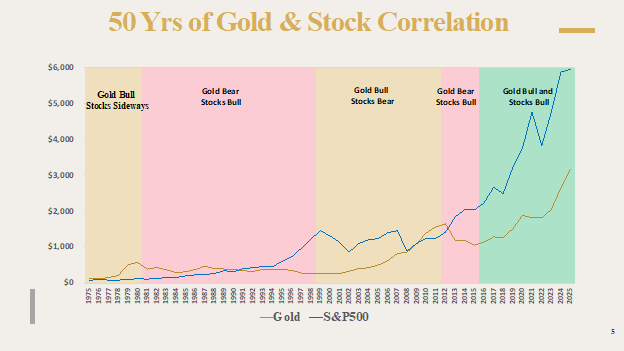

We have been advocates of diversifying – and especially a very uncorrelated diversification – using gold. The statistical analysis of the relationship between gold and stocks and bonds can get wildly complicated depending on the time frame. There is a positive correlation in almost all assets when you analyze on a long enough time frame – because the value of the dollar is designed to go down at 2% per year (2% is the Federal Reserve’s stated inflation target.) But if we are talking about numbers of years rather than numbers of decades, gold and stocks have virtually NO statistical correlation. That doesn’t mean that when stocks go up gold goes down – or vice versa – that would be a correlation, but a negative one. Interestingly, stocks and gold can go up, sideways or down independently of each other. Take a look at the many different periods that stocks (as represented by the S&P500) and gold have moved uncorrelated since gold became available for individual investors again in 1975…

Color-coded time periods are shown in this chart starting with 1975 to 1980 when there was a bull-market in gold and stocks traded sideways. Then gold went red and was in a bear market from 1981 to 1999 while stocks were in a bull market. 2000 to 2011 was another bull market for gold – but this time it was a bear market for stocks. Next, we had another bear market for gold and a bull market for stocks. Finally, since 2015 we have had a bull market in both gold and stocks. You can see that until the recent joint bull market in these assets over the last decade – there is no correlation between them.

Looking at total portfolio management, the above comparison shows a true diversification which has been called the Holy Grail of Investing. Fund managers, retirees and every investor in between want to have assets in their portfolio that move independently of each other. In a stock bear-market a non-correlating asset may trade sideways or even rally providing a psychological advantage – maybe an asset to sell if liquidity were necessary. All assets going one direction in a portfolio is only nice when everything is going up!

Between stocks, bonds, real estate, gold, private equity, crypto, and many other assets the world of investing is getting ever more complicated. As much as things have changed, some things stay the same. Gold has represented value for thousands of years but some investors in recent decades in the west haven’t seen it as part of a modern portfolio. That is all changing now as gold is being recognized as such a non-correlating asset AND we can now get an interest yield while still owning the physical asset. Gold is coming back into the monetary system of the world as a capital asset! There is an interest rate on gold!! Our GoldRush Yield Fund has been built to participate in this rapidly expanding marketplace – reach our to us to learn more!

Regards and good investing,

Greyson Geiler

Market and industry data used in this presentation have been obtained from sources believed to be reliable. However, we have not independently verified such data and make no representation or warranty as to its accuracy or completeness.

Goldrush Yield Fund, LLC is managed by Andorra Capital, LLC, a Registered Investment Advisor. Andorra Capital has a conflict of interest in recommending the Fund to prospective investors. This material is informational only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. The Goldrush Yield Fund is an unregistered private placement and is available solely to accredited investors. No securities commission or regulatory authority has approved or disapproved of the Fund, and there is no obligation to provide investment advice. Investing in the Fund involves risks, including the potential loss of principal. Past performance is not indicative of future results. Any forward-looking statements are based on current assumptions and are subject to change. Investors are responsible for conducting their own due diligence. Please review the Private Placement Memorandum (PPM) for detailed risk factors and consult with legal, tax, and investment professionals before considering any investment. For more information, please contact Greyson Geiler at ggeiler@andocap.com

Gold has been in the headlines of financial news quite a lot over the last few months because of a historic run that topped out – for now – at about $3500 per ounce. It is about 25% higher in US dollar terms just in 2025 and we see a lot of pontifications about how much higher it is going to go from here. We are obviously heavily invested and involved in gold. However, we look at it differently than just as an asset that is going higher so it must be bought and stored. We are focused on how investing in gold has changed.

Warren Buffett is one of the world’s best-known investors because of an amazing performance track record over many decades. Although his father valued gold from a monetary system perspective because of the limits it inherently puts on central bankers and politicians, Warren wasn’t so fond of gold. He famously likened investing in gold to owning a pet rock. It didn’t produce any earnings or interest or income. Even though gold has historically trended higher in US $ terms, Warren had a point…

Passive income is a big component of creating long-term wealth. Whether investing in stocks for dividend yield, bonds for interest payments or real estate for rental/lease payments, investors rightfully place a big emphasis on consistent income. This compounds the return of an investment which can be drastic as time goes on. When an income stream is the focus, less importance is placed on the market price of an asset – unless you need liquidity being forced to get out of an investment.

Over the last decade investing in gold has been changing – and now it’s ready for the mainstream portfolio. The change is happening because gold leasing and lending is now a rapidly expanding marketplace of borrowers, lenders and investors. The leasing side of marketplace is what we are focusing on today – so let’s take a closer look at what’s going on…

Historically, it was typically big institutions like central banks or bullion banks that would lease their gold out to earn a return on it. This market has been notoriously opaque with no standardization. In many of these “lease” deals, the gold was actually sold, and the proceeds would be invested in interest bearing assets. There would be a promise to return the metal at a later date, but this isn’t a true lease – it is really looks more like a loan. That brings in a lot of counterparty risk and when the price of gold is trending higher the issues can be amplified.

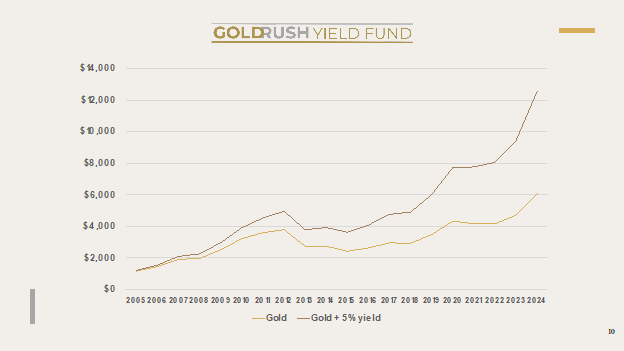

Now, rather than individual institutions leasing out their gold for a return in one-off opaque deals, there is a marketplace where businesses looking to lease gold can find investors with gold ready to lease out for an interest return. This marketplace of gold leases brings transparency and standardization to gold leasing, and it doesn’t only include the large institutions that have historically leased their gold. Our fund is participating in these standardized leases earning a risk-mitigated return on our gold. The interest rates are typically between 2-5% on the leases but they are set by a marketplace of supply and demand rather than dictated by central bankers like so much of our fixed-income world. These are true gold leases where the ownership of the gold stays with the investor – mitigating risk. Take a look at what a compounding 5% interest rate would mean to the dollar value of your gold holdings if you bought $1000 worth of gold 20 years ago.

This is a hypothetical example but comparing the US dollar value of gold holdings over the last 20 years between keeping it in storage vs leasing it out for interest payments is quite compelling. Keep in mind, the interest payments received by leasing gold out is in ounces of gold – not in US dollars. The ounces earned are also appreciating in value over time in US dollar terms. If the interest is continually leased out the compounding is quite impressive. Much like real estate, gold goes higher in US dollar terms. Also, much like real estate, we can now get lease payments from those who want to use our gold.

With the maturing marketplace of gold leases, a whole new world of opportunity opens up for investors. Getting a consistent income return from gold holdings reduces investor anxiety of paying too much for it – such as now after an historic run higher. Estimates from researchers vary, but there is probably about $5 Trillion of gold in bars and coins in private ownership stored around the globe. It has been sitting idle for decades, but now it is moving being deployed as a capital asset -there is an interest rate on gold again! Gold doesn’t have to be viewed as the doomsday asset that protects a portfolio from Armageddon. It can still fill that role, but now it can also be an income producing asset the likes of which even Warren Buffet might take a look at.

Regards and good investing,

Greyson Geiler

Market and industry data used in this presentation have been obtained from sources believed to be reliable. However, we have not independently verified such data and make no representation or warranty as to its accuracy or completeness.

To understand where gold is now, we need to take a quick look back at fairly recent history. Richard Nixon pulled the US Dollar off the gold standard in 1971 when it was priced at about $40 per ounce. The reason he did that was because many foreign trading partners of the US were starting to demand payment in gold instead of the Greenback. In the press conference he said it was a temporary solution to protect the dollar from shorts-sellers, but the fact of the matter was that too many dollars had been created by the Fed Reserve for the amount of gold on account. At that point, private investors in the US couldn’t legally purchase gold as FDR had issued an executive order in 1933 for all citizens to turn in their gold – and that executive order was still in place. The removal of gold backing of the dollar removed the guardrails to keep the government from overspending. The US dollar truly became a fiat currency being borrowed into existence with nothing tangible backing it. The great monetary expansion had begun…

Then on New Year’s Eve 1974, President Ford issued an executive order rescinding the gold ownership ban (Congress had passed a bi-partisan bill re-legalizing gold for investors a few months prior.) The price of gold averaged about $170 in January of 1975 as investors bid up the price with their first purchases in 40+ years. There was fear of inflation and gold was the go-to asset back then to retain purchasing power.

Gold had an eye-popping rally in the late 1970’s launching up to $850 in 1980. At that time Federal Reserve chairman Paul Volcker raised interest rates as high as 19% to fight inflation and gold sold off for two decades – finally putting its low in at about $265 in late 2000.

The subsequent rally in the US Dollar price of gold off that low was quite impressive as it traded higher 11 years in a row! (2001-2011) There were some wicked selloffs during that time as well when speculators got over leveraged, but the demand for gold was fierce. Then from 2012 to 2020 gold traded sideways with some big down moves but finally traded over $2000 per ounce.

Since the Covid crisis of 2020, central bankers around the globe have conjured up a blizzard of new currency units of every flavor and at the same time have gobbled up thousands of tons of gold for their own portfolios. The recent run-up over $3500 per ounce has been fueled by fear of international trade wars and “de-dollarization” of different trading groups. Gold has pulled back a bit, but the million-dollar question is – should investors still buy it at these levels? Here’s the million-dollar answer…YES!

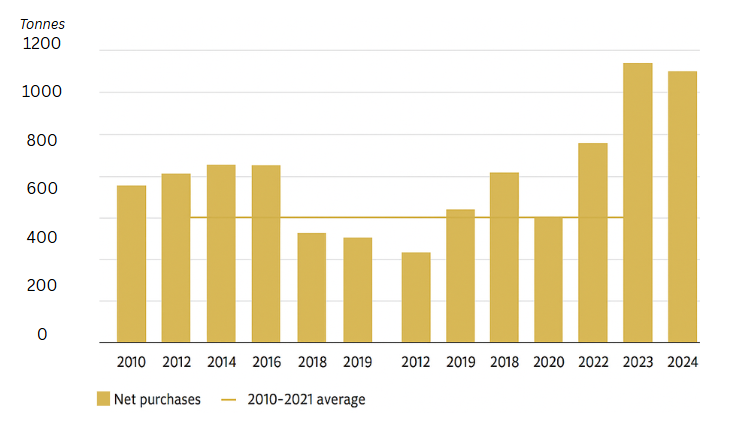

An historic look at demand-driven rallies in ANY market will educate you quickly that NO ONE knows how high “high” is. Meaning – gold could go a lot higher from here. No one can perfectly time market movements, the simple reality is that conditions are still bullish gold! The demand-driven description that we are using for this rally is because central banks and individual investors alike continue to acquire more gold. We can’t tell you when that slows down. The percentage of central bank assets that are in gold is still historically low and the percentage of private investors’ portfolios comprised of gold is probably still below 1%. All investors should own some gold and the demand side of the equation remains strong. Take a look at central bank net buying of gold over the last few years…

Sources: Metals Focus, Refinitiv GFMS, World Gold Council

Obviously, no one knows when this central bank buying slows down. Considering this demand which is more than 20% of total world production and a NUMBER of other factors, we continue to suggest acquiring more gold.

Here is the key – get a yield on your gold assets!! Warren Buffett famously described gold as a pet rock because it was a “non-performing” asset. There was no yield on holding it for individual investors. In fact, most people pay storage fees or mutual fund fees for their ownership of gold. However, now individual investors can lease or loan their gold out and earn a return on their assets. Our GoldRush Yield Fund is on the cutting edge of this change in the investing world. The marketplace of gold – and silver – returning to the monetary system as a capital asset being leased and loaned is growing exponentially! The anxiety of paying too much for an asset that has been rallying is mitigated by getting a consistent yield when you purchase! Think about it in terms of ounces rather than dollars. Interest payments increase the number of ounces you own – the dollar value of those ounces can be calculated later.

Reach out to us to learn more on getting a yield on your gold holdings!

Regards and good investing,

Greyson Geiler

Market and industry data used in this presentation have been obtained from sources believed to be reliable. However, we have not independently verified such data and make no representation or warranty as to its accuracy or completeness.

Goldrush Yield Fund, LLC is managed by Andorra Capital, LLC, a Registered Investment Advisor. Andorra Capital has a conflict of interest in recommending the Fund to prospective investors. This material is informational only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. The Goldrush Yield Fund is an unregistered private placement and is available solely to accredited investors. No securities commission or regulatory authority has approved or disapproved of the Fund, and there is no obligation to provide investment advice. Investing in the Fund involves risks, including the potential loss of principal. Past performance is not indicative of future results. Any forward-looking statements are based on current assumptions and are subject to change. Investors are responsible for conducting their own due diligence. Please review the Private Placement Memorandum (PPM) for detailed risk factors and consult with legal, tax, and investment professionals before considering any investment. For more information, please contact Greyson Geiler at ggeiler@andocap.com