by Greyson Geiler | October 23, 2023

Welcome to October – as happens quite often this time of year, the last couple weeks have brought quite a lot of uneasiness to financial markets. The war in Ukraine continues and now the world has added a second “war” with the violence between Palestine and Israel. Interest rates in the US have hit new 15-year highs and that has spooked equity investors prompting a selloff in the major stock indexes.

Some economic numbers continue to come in quite robustly – such as very low unemployment numbers. But as we have mentioned before, labor market statistics are typically trailing indicators. That means that, for example – unemployment numbers would begin to tick higher AFTER a recession has already started. Also, as we mentioned a couple weeks ago, the Department of Labor is testing its credibility with the consistent revisions DOWN of employment numbers after the headlines read how great the labor market is.

On the other hand, some economic numbers are coming in very poorly and there aren’t any revisions coming to save the day. Auto loans are a prime example. According to Cox Automotive, there will be 1.5 million autos repossessed by lenders in America in 2023. That is up from 1.2 million in 2022. Not good – and yet another indication that many consumers are stretched pretty thin…

The interest rate situation is a little worrisome for financial market watchers/investors because the latest surge higher in rates didn’t accompany higher interest rate speech by the FED. Many believe that the financial profligacy of our Federal Government is the culprit behind the latest move higher in interest rates. Budget concerns abound with line-item additions of ridiculous proportion to fund Ukraine and Israel. The Federal Government is running deficits about 6% of GDP which is an awful number. However, as much as we dislike much of what our government does, we are wondering what is new and why bond traders would be selling because of bad fiscal policies now. The White House has had problems even publishing a budget for more than a decade. We think there are a multitude of factors at play and in the end – just like most everyone else – we believe interest rates will come down. We just can’t tell you when.

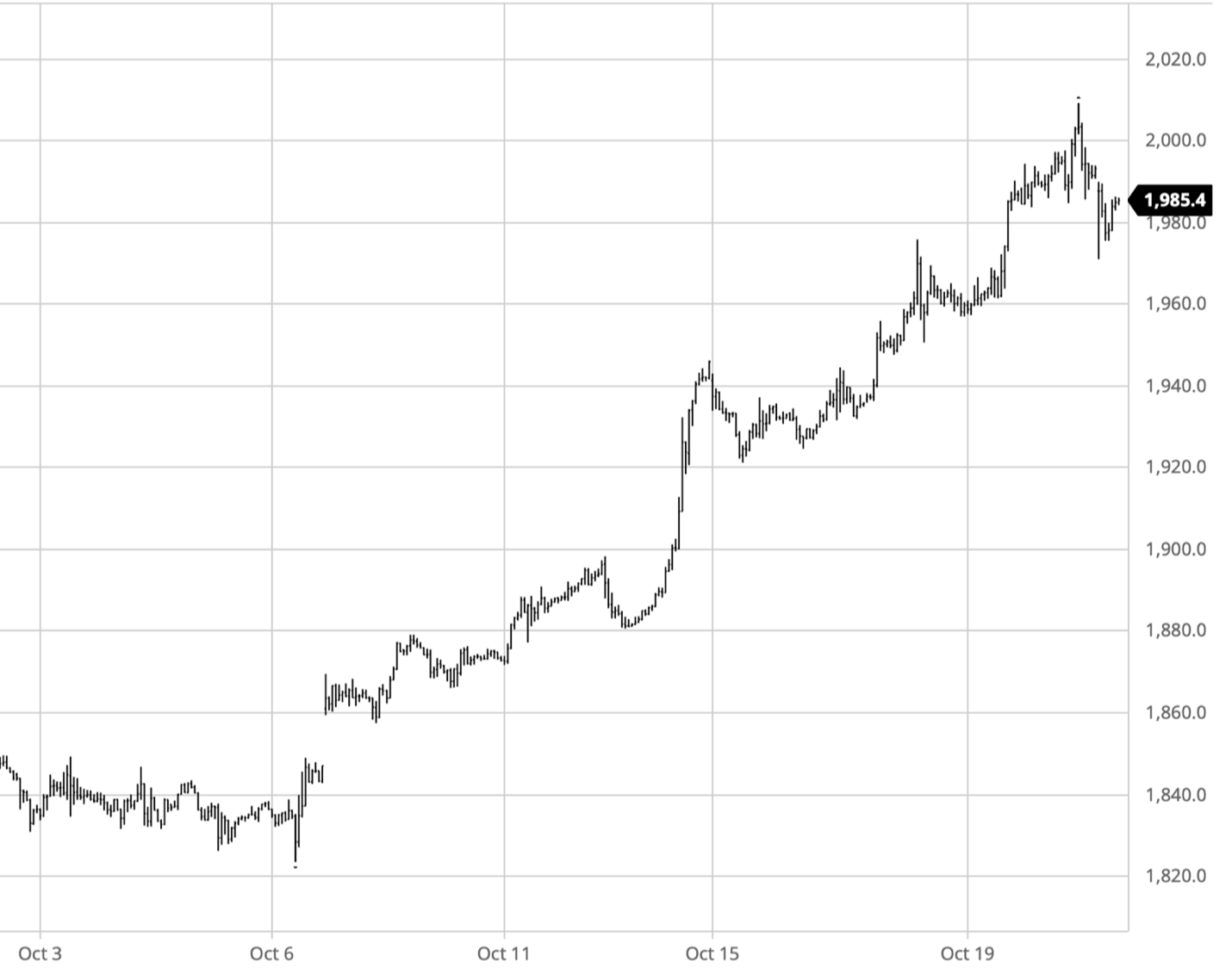

The US dollar continues its strength and we continue to believe that there is more upside. We believe that the rougher things get overseas, the more people will run to our capital markets for safety. Speaking of safety, the uneasiness in financial markets couple with the new violent conflict in Gaza initiated an October rocket launch in the ultimate financial safety asset, gold…

We are advocates of owning gold as a hedge against uncertainty and considering that you can safely deposit and earn interest on your gold holdings now – rather than storing it in your closet – there really isn’t much reason not to…

Going forward, as usual, investors will be watching the Fed. They have eased off their assertions that they will raise rates in November again and the Fed Funds Futures contract is oscillating between about a 25%-50% probability that the Fed will raise rates in December. We don’t want to try predicting what politicians will do, but we certainly hope the Fed DOES NOT raise rates again until things look different. We are afraid they are going to break too much of the world economy with these higher rates and then be forced to slam interest rates back down violently. That is a rollercoaster that is hard to do forward planning while riding on.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | October 2, 2023

Negativity continues to circulate in the financial media and recently some well known economists at Morgan Stanley have focused their antagonism toward the US consumer. Some of the news we have already commented on in this weekly post include some horrendous existing home sales numbers and stubbornly high inflation. Now we are staring the restarting of student loan payments which will initiate quite a drag on consumer spending. There are some 28 million Americans with student loans outstanding and the payments will amount to something on the order of $16 billion monthly or about $190 billion annually. Considering the government owns a strong majority of these loans, that may help the annual budget deficit numbers look less horrific, but we have to wonder how well the economy will handle this drag on consumption.

Back to the Morgan Stanley commentary – their equity strategist Michelle Weaver joins the chorus of Morgan Stanley Wall Street watchers with some sobering thoughts. She joins JPMorgan trader, Brian Heavey who has turned quite negative on the US consumer and Mike Wilson, Morgan Stanley’s chief investment officer who wrote about the “consumer falling off a cliff.” From 20,000 feet her analysis shows that the American consumer has run out of the excess savings from Covid lockdown time. From there, her focus is on the weakening leisure travel numbers that have spread pretty much across the board of hotels, airlines, low-cost airlines and even luxury travel. Although an AlphaWise Consumer Survey shows that 58% of respondents do want to keep traveling, some are resorting to driving or taking trains to keep costs down to more modest budgets. A chart of the large airline stock prices concurs…

Obviously, these numbers can be partly due to the tightness in crude oil supplies and corresponding prices. But it still looks pretty soggy – especially considering how tight the Fed is clamping down with high interest rates.

There are many other economic fronts that aren’t looking robust either. One of the concerning things to us is how the economic numbers are being reported by this administration. We do our best to not get political in our weekly posts, but we have been watching economic numbers reported by our different government agencies for nearly three decades. Things have recently changed and NOT for the better. An example is the Bureau of Labor Statistics who reports on many economic statistics, but very notably the high-profile monthly payroll numbers. So far in 2023 EVERY SINGLE monthly payroll number was later revised lower (June later cratered by a whopping 50%!) For that to happen every month if the statistics were being reported honestly would be a 12-sigma event. Obviously, it is politically motivated and that is just one example. Personal consumption number, savings numbers and full GDP numbers are being adjusted later as well. We are wondering about a lot of government numbers now and it is not encouraging.

All this being said, the financial markets are still holding together quite well considering the negativity. September was a fairly rough month for most of the stock market averages, but the indexes as a whole are not outrageously priced like they have been in past bubble times (2000 and 2008 for example.) If the Fed is serious about “higher for longer” referencing the interest rates on the short end of the trading curve (overnight rates that are about 5.5% now) then some of the doom projectors could certainly be correct. These interest rate WILL break more things in the world economy if they remain this high or higher. We can’t time any of this and we can’t predict what the Fed will do in the near to medium term. If the turbulence in your stock portfolio over the last month is keeping you up at night you need to lighten up your positions. The last 25 years has brought wild volatility to our financial markets. Reduce your risk to the point that the next “March of 2020” event at the start of Covid doesn’t change your lifestyle.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | August 7, 2023

Strange economic numbers continue to show up in our post-Covid world and the most consistently surprising of these numbers has to do with employment…

“If every unemployed person in the country found a job, we would still have 4 million open jobs.”

– U.S. CHAMBER OF COMMERCE

So, according to the U.S. Chamber of Commerce we have more jobs than employees and there are only 5 states where this is not the case. That lends for interesting dynamics in the financial markets when the Federal Reserve stomping on the economic breaks with aggressively higher interest rates.

One has to ask how the employment numbers remain so strong – and of course government involvement because of Covid has something to do with the present employment situation.

During and after Covid, government support for those who lost work and other subsidies made it easier for people to stay home and out of the workforce. A Chamber of Commerce survey found that 1-in-5 people have changed their work style since the pandemic, with 17% having retired, 19% having transitioned to a homemaker role, and another 14% working only part time. Ed Dowd who is a former Blackrock guy on Wallstreet is putting out research that the vaccination has handicapped several million workers and put them into the disability category. His thesis is that more disability claims has tightened the labor pool and that is the driving force behind low unemployment even though the Fed is aggressively raising interest rates.

Regardless of the reason, unemployment remains stubbornly low and the Fed will have that to contend with if they are going to bring inflation back down toward 2 percent…

On the other side of the coin some economic numbers don’t look so hot. A.P. Moller-Maersk A/S, the world’s largest owner of container ships and one of the best bellwethers for global trade, has spent the last several quarters warning about a slowdown in container demand on major shipping lanes. The Danish shipping and logistics group released yet another warning last week – this time it feared a contraction in global trade would be longer and deeper than previously thought:

The inventory correction observed since Q4 2022 appears to be prolonged and is now expected to last through year end. Based on the continued destocking, A.P. Moller – Maersk now sees global container volume growth in the range of -4% to -1% compared to -2.5% to +0.5% previously.

The shipping numbers look pretty tepid and of course everyone is still pointing toward China wondering when they will start showing better economic numbers. The collective Chinese credit card was the largest recovering force for the world economy after the 2008 meltdown – that hasn’t been the case post Covid.

Big news hit last week when Fitch officially downgraded its U.S. credit rating from AAA to AA+. Of course, this is huge news and Fitch cited many of the factors we have been discussing for years in order to justify their downgrade decision. By and large, the national debt burden is of serious concern and with budget deficits EXPANDING rather than contracting now that we are past Covid – reasonable people need to be concerned…

Not only are these debt numbers rocketing to the stratosphere, but the amount of interest that has to be paid on the debt is rocketing higher too. Don’t forget, after the Fed took short term interest rates to zero in response to the 2008 economic meltdown, the Treasury started spinning longer term debt notes and bonds into shorter term bills when they matured because the interest payments were so low. Consequently, even though total debt owed by the Federal government dramatically increased in the years after 2008, the total interest being paid on that debt was actually going down as interest rates were so low. Obviously that has come snafu on our financial overlords as now interest rates are booming higher on bigger numbers of debt – a double whammy. Interest payments on the national debt has already gotten to the fourth largest budget item at more than $650 billion annually behind Social Security and Medicare. Soon these interest payments will surpass national defense and be the third largest budget item. One has to wonder when the Minsky Moment rears its ugly head – next week we will talk about formulating a Plan B to hedge some of our risk.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | July 10, 2023

Most every week we begin this post talking about the lack of consensus that financial markets and financial pundits are presenting. In addition to that most of our posts involve complaining about the Federal Reserve and their creation of these chaotic conditions. This week will be no different…

Intuitively we are in for some rough economic waters. The Federal Reserve kept interest rates artificially low- essentially zero – for more than a decade and then raised rates at the fastest pace of more than four decades. That makes for a rough environment – especially in some of the long-term planning that goes on in very capital-intensive businesses (e.g., the massive semi-conductor production facilities being built right here in AZ.) However, like we also frequently mention in this post – the economic environment is holding together remarkably well…

We can sit around and pontificate on how dangerous the economic/financial world is all we want, but sooner or later we have to look at statistical facts. Of course, one of the most important statistics involves companies that simply cannot survive and declare bankruptcy. We have referred to these numbers as they have been coming in from the real-world economy this year. Now we have completed the first half of 2023 and can make comparisons to historical norms…

In the first six months of 2023, there were 340 corporate bankruptcies, topping every other comparable span in 13 years, according to S&P Global Market Intelligence. This is up 93 percent from the same time a year ago and higher than in 2020, when there was a spike during the early days of the coronavirus pandemic. This is clearly of serious concern, especially when the Federal Reserve is indicating that they will be raising rates again in the fall. Here is another fun statistic – Year-to-date through June, 15 companies with more than $1 billion in liabilities filed for bankruptcy, such as Cyxtera Technologies, Diebold Holding, Bed Bath & Beyond, Diamond Sports Group., and Party City. Those are the big companies, but here is another daunting stat – according to Epiq Bankruptcy, a U.S. bankruptcy filing data provider, 2,973 total commercial Chapter 11 bankruptcies were filed in the first half of 2023, up 68 percent from the same period in 2022!

Obviously, the raising of interest rates has been the catalyst for a big percentage of these companies that are finally throwing the towel in. They are having a tough time refinancing debt at these higher interest rates – but another concern is how little banks are lending regardless of interest rates. A recent Goldman Sachs survey found that three-quarters of small business owners say they are worried about accessing capital as banking stress has forced the sector to tighten lending. Ladies and gentlemen, we are entering a credit crunch of sorts – but that is laser focusing on banks lending to smaller companies. Rest assured big banks and big companies are who the Federal Reserve works for and who their policies will not only protect but enhance. So, unless we see a larger capital market meltdown, maybe we aren’t staring at Armageddon. How does the age-old indicator of the junk-bond credit spread look?

As you can see the difference between junk bond interest rates and “no risk” 10-year treasury bond interest rates looks relatively OK. Junk bond yields are higher than most of recent history, but 10-year treasuries are higher than they have been since 2007. The spread between these yields is about 4% – which is fairly high historically but take a look at 2008. The difference between interest rates on junk bonds and treasuries was more like 20% then!!! So, what does that mean to us as financial market investors today? In overgeneralized terms it means that we don’t appear to be looking at a widespread capital market panic at the present. Yes, there are lots of corporates (especially smaller companies) going bankrupt, but that is part of a free market system. From a systemic perspective, we aren’t sounding alarm bells…

Remember the Federal Reserve is manipulating the system in meaningful ways right now backstopping the big banks and it appears to be working. They continue to involve themselves in the inner workings of everything financial to greater degree as the crises they engender stack up. No one can be certain that this manipulation will continue to stave off disaster in the long run – and actually history says that it won’t – but no one can time these sorts of macro-changes. The Federal Reserve created $6 trillion out of thin air to support markets after Covid. We are worried about the size of the next bailout…

Considering that, we are fans of building a plan “B” to this monetary system. That involves building gold reserves and deploying some of that gold to earn interest in gold. It is a grass-roots monetary system that is gaining a lot of momentum. Let us know if you would like to look further into it…

Regards and good investing,

Greyson Geiler

by Greyson Geiler | June 26, 2023

As we have mentioned repeatedly in this weekly post, the resilience of the U.S. stock market considering aggressive interest rate hikes from the FED has been quite impressive. The driving force behind this strength could be a combination of a number of things. Left over cash balances from the ridiculous blizzard of money creation the Fed embarked upon after Covid could be one thing. The continual progression of technologies that are making businesses more efficient could be another. The idea that America is doomed and China is the preeminent world power is clearly fading – so that seems to be supporting our asset markets. There could be factors that we have no awareness of getting priced into the markets. Time will tell…

All of that considered, looking forward we are starting to get concerned. The lag time between the Fed raising interest rates and the corresponding affects on the economy is generally considered to be about 18 months. If that is accurate, then we are just now getting to the slowdown that the Federal Reserve was attempting to engender with higher rates. They started raising rates in the spring of 2022. Clearly things are slowing down now – the million-dollar question is how much and will it spill over into a recession.

The yield curve has been inverted for about a year now – historically that has resulted in a recession – however the timing is never exact. The Fed has officially paused its hiking of interest rates but they may increase again at their next meeting. They are continuing to read from a faulty playbook. Their number one error is one we have mentioned before – that higher interest rates equal lower consumer prices – or lower inflation. That is an obvious fallacy as higher interest rates discourage investment in production resulting HIGHER consumer prices. Also, interest payments are part of the cost of production – when those rates are higher, producers have to pass costs on to consumers or go out of business.

The second misstep of the Fed is their focus on employment numbers. Employment is a lagging indicator number one, but more importantly, post Covid the labor force is smaller. Looking at disability claims from insurance companies, disability rates have skyrocketed. https://www.westernstandard.news/news/expert-tells-nci-us-death-and-disability-up-40-for-adults-under-65/article_2810b2f6-eac6-11ed-8c44-4335ce522654.html

This explains a lot of the tightening in the labor market – so it is not a situation where the economy is so strong that it is supporting extra workers and needs to be cooled

So, if the Fed is so wrong and we are so right – then how does this get reconciled? We think there is at least a significant possibility that the economy continues to deteriorate and the Fed is forced to lower interest rates. Sadly, our guess is that something will have to break (more than the banking problems we have already had) for the Fed to lower rates. Here are some of the indicators to watch going forward…

- The continued deterioration of the commercial real estate situation. Vacant office spaces are piling up all around the country, but one example is in San Francisco where a Coldwell Banker report had office vacancies at an all-time record rate of 29.4%.

- Banks borrowing from the Fed’s emergency bank term funding program facility. Currently the facility has loaned out $102 billion. Continued increase would be an indicator of continued erosion in banking system conditions due to higher interest rates.

- Global Purchasing manager indexes – especially in Europe – have clearly shown a decline in manufacturing activity. The U.S. continues to be the bright spot, but no one knows how long that can continue.

Consumer strength and resilience in the U.S. has maintained well since Covid, but cracks are appearing in the dam. Don’t forget that student loan payments resume in a few months and personal savings rates look terrible back at the 2007-08 levels…

Our concerns our growing that the economic slowdown could accelerate due to the higher interest rates finally taking effect on consumer spending. Keep in mind that doesn’t mean we should sell all our stocks and run for the hills– because we have been through several iterations historically of bad economic news being good news for asset markets. Traders may assume that interest rates will be lower and continue buying stocks and bonds. That being said, we are instituting more caution – and you can get decent interest rates while you cautiously wait.

As we frequently end with…don’t sell your gold!

Regards and good investing!

Greyson Geiler