Welcome to October – as happens quite often this time of year, the last couple weeks have brought quite a lot of uneasiness to financial markets. The war in Ukraine continues and now the world has added a second “war” with the violence between Palestine and Israel. Interest rates in the US have hit new 15-year highs and that has spooked equity investors prompting a selloff in the major stock indexes.

Some economic numbers continue to come in quite robustly – such as very low unemployment numbers. But as we have mentioned before, labor market statistics are typically trailing indicators. That means that, for example – unemployment numbers would begin to tick higher AFTER a recession has already started. Also, as we mentioned a couple weeks ago, the Department of Labor is testing its credibility with the consistent revisions DOWN of employment numbers after the headlines read how great the labor market is.

On the other hand, some economic numbers are coming in very poorly and there aren’t any revisions coming to save the day. Auto loans are a prime example. According to Cox Automotive, there will be 1.5 million autos repossessed by lenders in America in 2023. That is up from 1.2 million in 2022. Not good – and yet another indication that many consumers are stretched pretty thin…

The interest rate situation is a little worrisome for financial market watchers/investors because the latest surge higher in rates didn’t accompany higher interest rate speech by the FED. Many believe that the financial profligacy of our Federal Government is the culprit behind the latest move higher in interest rates. Budget concerns abound with line-item additions of ridiculous proportion to fund Ukraine and Israel. The Federal Government is running deficits about 6% of GDP which is an awful number. However, as much as we dislike much of what our government does, we are wondering what is new and why bond traders would be selling because of bad fiscal policies now. The White House has had problems even publishing a budget for more than a decade. We think there are a multitude of factors at play and in the end – just like most everyone else – we believe interest rates will come down. We just can’t tell you when.

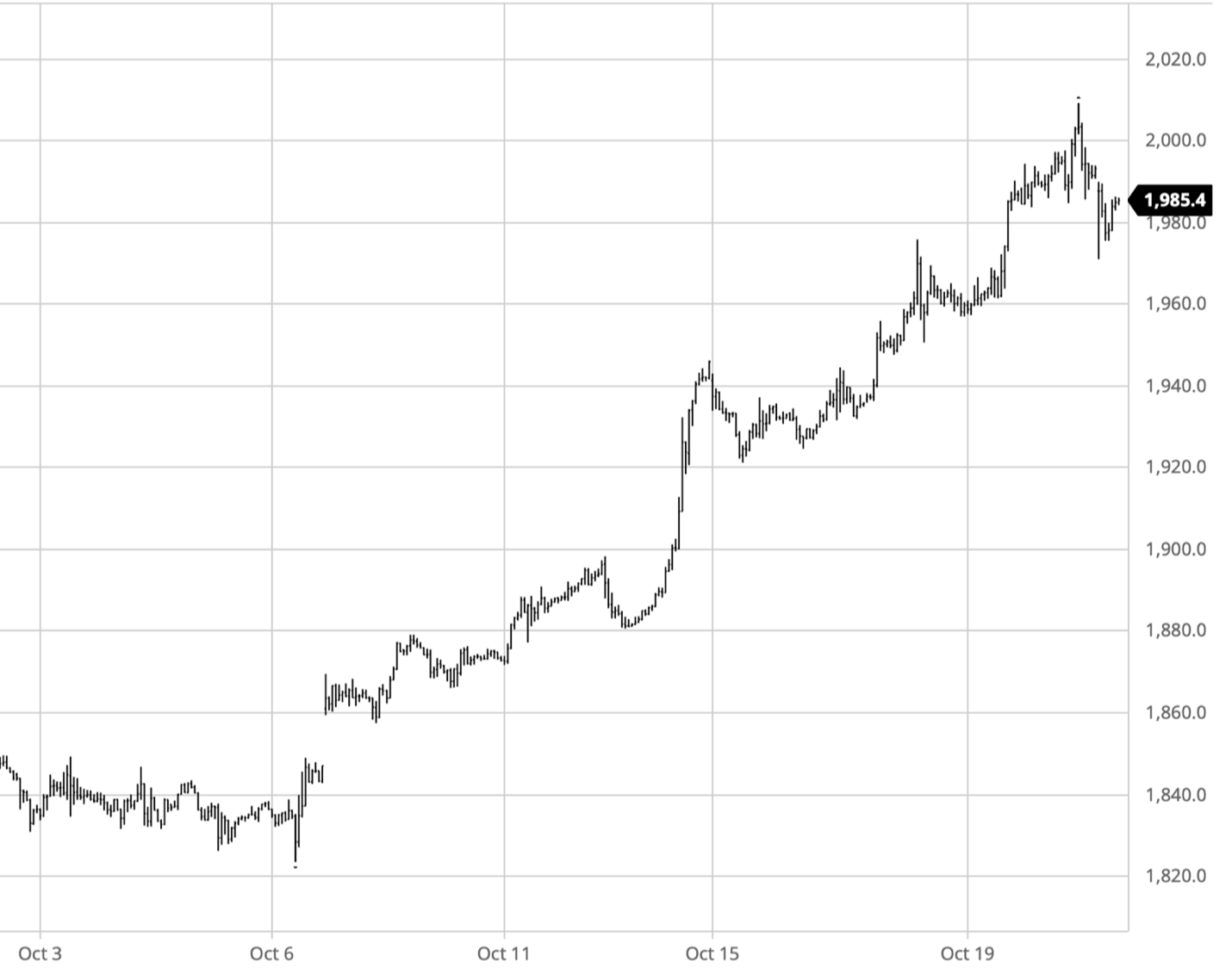

The US dollar continues its strength and we continue to believe that there is more upside. We believe that the rougher things get overseas, the more people will run to our capital markets for safety. Speaking of safety, the uneasiness in financial markets couple with the new violent conflict in Gaza initiated an October rocket launch in the ultimate financial safety asset, gold…

We are advocates of owning gold as a hedge against uncertainty and considering that you can safely deposit and earn interest on your gold holdings now – rather than storing it in your closet – there really isn’t much reason not to…

Going forward, as usual, investors will be watching the Fed. They have eased off their assertions that they will raise rates in November again and the Fed Funds Futures contract is oscillating between about a 25%-50% probability that the Fed will raise rates in December. We don’t want to try predicting what politicians will do, but we certainly hope the Fed DOES NOT raise rates again until things look different. We are afraid they are going to break too much of the world economy with these higher rates and then be forced to slam interest rates back down violently. That is a rollercoaster that is hard to do forward planning while riding on.

Regards and good investing,

Greyson Geiler