The selloff in the world’s bond markets and the corresponding rise in interest rates continued this week especially in Euroland. The reasons for that are many including inflation fears and the Federal Reserve pulling back on their asset purchases which were $120 billion per month. Icing on the cake is the Fed claiming they will continue raising rates throughout the year; however some argue that that is supportive to LONG TERM bonds because it represents the Fed fighting against inflation which is the biggest danger to long term fixed income assets.

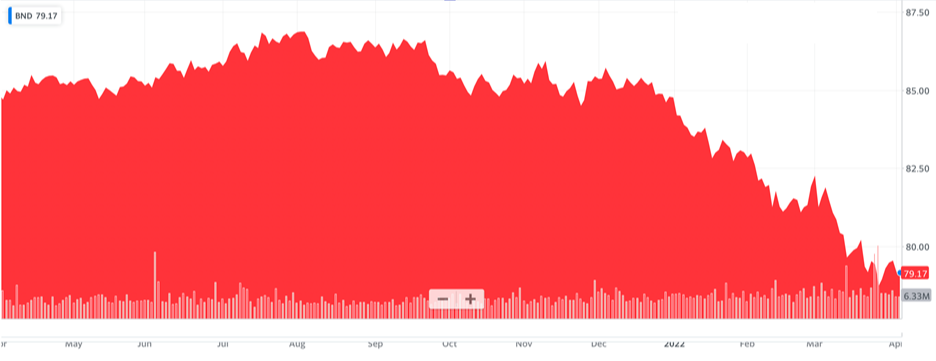

Of course, the economic world is reeling from supply shocks carrying over from the Covid “pandemic” and now the Ukraine situation. The biggest input in the inflation fears right now is the end user cost of gasoline. That is obviously just a headline issue with many problems behind the scenes – and the end result is a precipitous selloff in bonds of all different varieties. Our impression of the situation as usual, is that the Federal Reserve is largely at fault because of their actions inflating a ginormous world-wide bond bubble. Now the bonds are selling off leading financial observers to fear a popping of this bubble which would force the Fed to come in with more “stimulus” to prop the markets up. Take a look at a chart of the Vanguard total bond fund…

This has been an aggressive selloff in bonds in general, but what about the junk bonds? High yield corporate bonds or junk bonds are the debt with the most risk and therefore pay the highest interest rates. These bonds are what typically indicate stress in the credit system that may cause problems, even a purge of bad debt. For example, back in 2008 the interest rate difference between junk bonds and US Treasuries (no risk) was HUGE. It peaked at 21% – which means that junk bonds were viewed as so risky as the system was shocked by 2008 financial market chaos that they yielded 21% more interest than no-risk treasury bonds.

In March of 2020 at the depth of the Covid market fears, this spread pushed out to 11% – not panic like 2008, but a hefty interest rate difference. For perspective, now the spread between junk and treasuries is hovering near historic lows around 3%. That isn’t telling us that a financial market Apocalypse is around the corner. As a matter of fact, it is an indicator that the markets are taking higher interest rates and the other economic dangers quite well. Of course, that is not an endorsement of the actions of the Fed – more a statement that it seems to us they are still getting away with their policies of way too loose money.

The stock market has stabilized, and commodity markets have calmed down. However, the Fed and many market observers are predicting as many as 10 more interest rate hikes before this credit tightening cycle is over. We will be looking for cracks in the dam all along the way because the idea that the Fed is going to raise rates until there is a soft landing in inflation, and everything goes back to “normal” seems WAY overly optimistic to us. So stay tuned, don’t get overly leveraged and don’t sell your gold!

Regards and good investing,

Greyson Geiler