There is a lot of talk in the economic/financial news about inflation – both what we are looking at today and expectations of future inflation. First let’s agree on the definition of inflation because we hear many different explanations. From 20,000 feet everyone can agree that the devaluation of a currency or stated differently, the decrease in the purchasing power of a currency is the core of the definition of inflation. The problem in measuring and quantifying inflation is where the disagreement starts. Some analysts see measuring inflation as a function of the money supply, while others define it as simply the increase in costs of a predetermined basket of goods. For the purposes of this discussion, we will consider inflation to be determined by the increase in the price of goods as the U.S. Bureau of Labor Statistics puts out. Many observers criticize the BLS and postulate that their mechanisms are faulty resulting in a continual understatement of the statistics that get published. We will leave that argument for a different discussion and use the BLS data.

Historically CPI – or Consumer Price Index – has been the go-to number to describe the inflation in the moment. Recently the BLS reported that for the year ending in September, CPI was 5.4% which is raising eyebrows. Of course, many of us are old enough to remember the double-digit inflation of the late 1970’s. Back then, the situation seemed so dire that we had to initiate Donald Rumsfeld as a de facto inflation czar, and he was tasked with putting governmental control on inflation. Clearly the situation today is nothing close to where we were then, but this is the highest number since the brief inflationary period of 1989-1990. So now the obvious question is – why would the Federal Reserve still have the pedal to the metal (effectively zero short term interest rates, buying $120B per month of bonds, and taking over the repo market) when inflation is running hotter than it has in decades? We don’t really like the answers to that question but here they are…

- The Federal Reserve has prepped us for this situation. They have said that with such a disruptive and deflationary event (Covid-19) they were willing to tolerate more than their typical 2% targeted inflation for some period of time – completely arbitrary – but that is what they said

- The Federal Reserve has labeled the present bout with inflation “transitory” meaning that they believe the temporary supply chain disruptions are causing short term problems that manifest in inflation numbers now, but will soon abate as supply chain disruptions are repaired

- Clearly the Federal Reserve has taken on a mandate of supporting asset prices – completely of their own accord. They have never been officially tasked with this mandate – however, they are obviously making decisions with this in mind

So, these reasonings of present Federal Reserve behavior are by no means complete. But they do give a basis for what is going on. We do not appreciate the concept of one entity having the sort of power the Fed does (although we do doubt that they control to do the degree the financial press implies.) They have poured amazing amounts of “liquidity” on the present situation – trillions and trillions of dollars – and yet we only have 5.4% inflation? Viewing with a historical lens one would expect runaway hyper-inflation. So, what gives? The Fed clearly wants and needs inflation (the mountains of debt in our system need to be devalued) – but it is quite mild considering their actions.

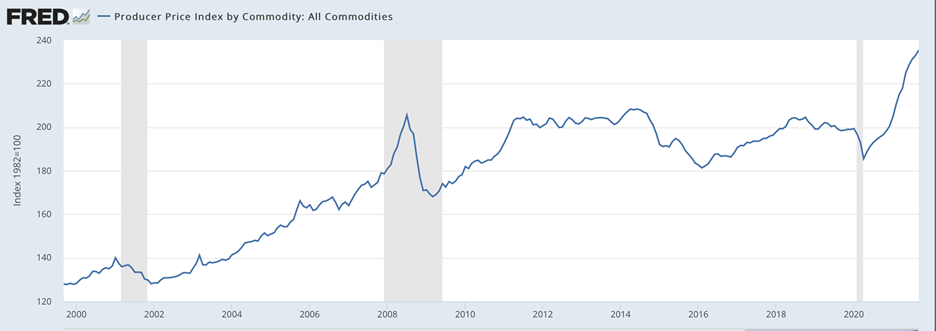

One thing we would like to point out is how far the PPI – or prices that producers are paying – have outpaced CPI. Supply chain issues have obviously been the catalyst to this launch in pricing that producers are experiencing. We are surprised considering this and other factors that CPI numbers – and the prices consumers pay for basically everything aren’t DRASTICALLY worse. Is this an indication that producers are having a tough time pricing their costs into what they charge consumers? Are business profit margins in trouble going forward?

To make sense of why consumer price inflation isn’t significantly worse than it is, we have to consider some deflationary factors that are running strong counterbalances to the Feds nauseating blizzard of “liquidity.”

- An aging population in the developed world is clearly a factor with loan demand from the big banks being tepid as an obvious manifestation. Baby boomers are consuming less and some of them full on downsizing and moving into group communities

- Mountains of debt require interest payments to be serviced. That imposes deflationary effects of tens of trillions of dollars of debt are being piled on top of existing mountains of debt in the developed world

- Technology is going parabolic creating amazing efficiencies in many different industries

We obviously have reservations of the monetary system as the Fed has designed it and is abusing it. However, when we try to read the tea leaves about consumer price inflation that may be coming in the near term, we believe that the fears have been overblown. Our list of potential deflationary reasons for that may be incomplete but something is holding hyperinflation at bay – that is good news! We believe that good news is at least part of what is pushing stock prices continually higher – so it is getting priced in as we speak. As soon as the financial media starts agreeing with us that may be an indication that asset prices are getting near a top – so stay tuned.

Regards and good investing!