by Greyson Geiler | October 11, 2021

The launch of cryptocurrencies began with Bitcoin in 2008 and at that point it had very little fanfare. The cost per Bitcoin was just over $.01. The origins of Bitcoin are still very mysterious even to this day. The “founder,” Satoshi Nakamoto – and no one knows if this is even an actual person – originated the decentralized currency and its price quickly started higher.

Quickly the value of Bitcoin began its assent and by the end of 2017 had traded at nearly $20,000. It sold off from there but in spring of this year traded $64,000 and now may be heading back towards the high. Thousands of other cryptos have been created in the meantime attempting to cash in on the same frenzy and it is still a very hot topic.

We frequently get questions from investors about crypto-currencies and whether we believe they will replace the banking system, whether they are a complete Ponzi-scheme and will soon crater to zero, or something in between. Our response is that we see crypto as innovative technology, but speculative financially. There is nothing wrong with having a “toe in the water” as we suggested nearly a year ago https://andorracapital.com/u-s-dollar-weakness/ – but we certainly don’t agree with going “all-in” as some aggressive bloggers do.

One of the big reasons we view Bitcoin and other cryptos as speculative is because their core functionality – and that is a decentralization that can’t be taken control of by a government or a central bank. As we have repeatedly discussed in this post, the central banks of the world have far more power than ever and it continues to grow. That power will not be relinquished easily. We don’t have any insider information on that, we are just referencing one of the core axioms of human nature. We also don’t see these cryptos replacing the functions of our banking/monetary system. Without going of too far on a tangent – a quick illustration of this – Imagine in summer of 2019 you borrowed $300,000 in Bitcoin to buy a new house. Your monthly payments – from about $1300 in 2019 are now NEARLY $17,000 PER MONTH (corresponding value of Bitcoin.) But it gets worse – now instead of owing about $285,000 – you owe Bitcoin that are worth about $3.98 million. Cryptos as they exist are NOT going to replace our banking system – but the market capitalization (total value) of these currencies has gotten quite impressive (courtesy of coinmarketcap.com) totaling nearly $2 trillion…

But now the story gets more complicated. Central banks are figuring out some of the power that the cryptocurrencies have – and they are developing versions of their own. The big difference in the government/central bank issued currencies is they will be centralized rather than decentralized. The issuing bank will have total control over the currency units. They will know who holds them, how they are spent, when they are spent – they will even have an off switch if they want to shut a new crypto – currency holder down. The Chinese are expecting to roll their new crypto yuan in time for the 2022 Olympics – and have already divulged that it will have a timing mechanism programable into it. Meaning, if the “People’s” Bank of China chooses to, they could put an expiration date on specific units of the new currency. That’s right, if you are contemplating storing these crypto yuan for future use (or for capital gains like Bitcoin) you may want to rethink your strategy.

And don’t think for a second that a timing mechanism is the only thing that can and will be programmed into these “cryptos” launched by central banks. They will have the power to dictate precisely how these currencies will spent, and quite obviously, if these currencies ever hit the market, they will use that power. Many communist countries historically have figured out in isolated situations how to pay workers tokens rather than currency that could be used internationally or even nationally. Chinese steel workers were a perfect example. They got paid in tokens that were only redeemable at the company store on campus (prices probably weren’t very competitive.) Central bank issued cryptos would be the same animal with different stripes. The bank could create currency that couldn’t buy books written by people spreading “misinformation” as an example. Digital cash could be programmed to ensure it is only spent on essentials, or goods which an employer or government deems to be sensible. This isn’t conspiracy theory paranoia. A quote from Agustin Carstens, head of the Bank for International Settlement (kind of the central bank for central banks in Switzerland) sounds like this:

[The key difference [with a Central Bank Digital Currency] is that the central bank would have absolute control on the rules and regulations that will determine the use of that expression of central bank liability, and they have the technology to enforce that]

First of all, how do you like the fact that a central banker for central banker refers to your money as “central bank liability” – and second to consider that, therefore it is only their right to control it? This is ominous for the long term…

…or how about a quote from one of our favorite directors at the Bank of England, Tom Mutton…

“You could introduce programmability […] There could be some socially beneficial outcomes from that, preventing activity which is seen to be socially harmful in some way”

This is obviously an arbitrary all-encompassing power over society that would make George Orwell’s skeleton blush. But before we go off the deep end and run for the hills with our freeze-dried food and shotguns, let’s consider some of the good news when looking at this situation from 20,000 ft…

The U.S. dollar is the world’s reserve currency – that is still paying us dividends on the whole as a society. No matter how often we disagree with Chairman of the FED Powell, it is quite apparent that he is aware of our position and isn’t going to attempt to launch a crypto in the near term. Although it will happen eventually – quote from Powell ensures that: “It’s more important to do this right than to do it fast,” we have time to watch how this rolls out around the world and prepare accordingly if necessary.

As we sit now, our financial “leaders” have a lot of work to do just in weaning us lowly Americans off cash (and they are attempting to do just that.) Right now, in our society, nearly half of all daily transactions less than $50 are done in cash. THAT IS GREAT NEWS!! Our officials can’t spend their political capital squashing that – it is largely in the parts of society that are “marginalized” according to the identity politics that are prevalent today that this cash is utilized. Any large changes to our financial system will be staged in – and right now it still looks like officials are “testing the water.”

In the meantime, don’t sell your gold and consider using cash on a more regular basis. A movement is starting for Americans to only use cash on Fridays rather than debit/credit cards. We are fans of this idea – cash is the ultimate economic freedom, and we don’t want to lose that!

Regards and good investing!

by Greyson Geiler | September 27, 2021

With the worst of the Covid issue seeming to be in the rear-view mirror, and the Federal Reserve (and the rest of the world’s central banks) continuing to provide more “liquidity” than is reasonably necessary, we begin to look at what is coming down the pike that we need to worry about from an economic and financial market perspective. Asset prices have been rocketing higher ever since the March 2020 meltdown and look like a unicorns-and-ice cream depiction of the state of our world. So, what could derail the “everything bubble” which is what some doomsdayers have labeled the present state of our economy and financial markets? Considering where there may be rough waters ahead from an overhead perspective looks something like this…

Our biggest concern is of course the predicament of the “stimulus” that is being poured on the world’s monetary system by the central banks. There are many problems and unintended consequences of this sort of meddling by the central banks, but the most obvious is simply the mountains of debt that have been accrued. Government entities, individuals and corporations have all stacked up unprecedented amounts of debt due to the artificially low interest rates and the reigning in of natural market forces that would force liquidation and default. We could argue all day about what caused the real starting point of this debt deluge, but it is obviously accelerating at this point and that is becoming unnerving. Can the world central banks allow markets to stand on their own? We suggest that there would be unprecedented carnage of the central banks quit their injections of “liquidity” – but will they slow down? Inflation is heating up and the FED in particular, is starting to have a tough time justifying keeping the pedal to the medal. If they did back off it may take quite an economic hiccup and aggressive selloff in asset prices to bring them back to the table. Of course, they would have to come back in and “save the day” as they have taken so much control and responsibility. When would that happen? How much of a temper tantrum will the market throw when the FED takes its foot of the gas? How much “stimulus” will the markets/economy require next time around or during the next “crisis”? These questions make the financial markets more like a casino than they should be…

Next up on our list of concerns is political turmoil. The biggest ball getting tossed around in Congress is of course a $3.5 trillion “infrastructure” bill which, pass or fail could mean a lot to financial markets. Fearing more treasuries hitting the market (our government would have to issue a lot more debt,) the 10-year treasury yield has snuck back out to almost 1.5%. That interest rate isn’t a backbreaker now but what if more fiscal “stimulus” gets voted in and more treasuries hit the market pushing rates further? Other political fighting largely looks like theater, but if too many vaccination restrictions get mandated, we could see big economic pullbacks as that is a very polarizing concept. Another serious political concern that could really throw a curve ball to the economy and asset markets is the issue of corporate and personal taxation. We believe in general that tax rates will go higher, but the specifics seem wildly unorganized right now and this could turn out to be much different than any current expectations. Stay tuned…

Of course, we have to worry about China with the recent real estate and debt domino worries from Evergrande Group. The Chinese government has recently been quoted as saying they will “protect consumers” but we still don’t know exactly what that means. Some financial pundits are worried that this could still trigger a contagion reminiscent of Lehman Brothers from 2008. Markets have really calmed down with regard to this, but we certainly aren’t sure that we are out of the woods yet. China has been a disproportional driving force in global growth since the 2008 meltdown and a new debt crisis there would be hugely detrimental to the world economy.

Asset price (stock, bond, and real estate market) valuations are a concern. Overbought markets get more overbought, so trying to time the demise of a long running bull market is a fool’s errand. Bubbles don’t really collapse under their own weight, but when we have historical valuations at the sort of highs we have now, one fears that long term gains from this starting point won’t look so good. Many of the historical indicators, P/E ratios, Price to Sales ratio, Warren Buffet’s stock market capitalization to GDP ratio, corporate debt to GDP ratio – all are at or near historical highs. Again – this doesn’t mean we need to run for the hills and sell everything, however this needs to be on the radar…

Business hiccups with supply chain problems and declining margins. This is a 10,000 ft concern without real specifics. Some industries – shipping for example – are still struggling from some of the supply chains broken by the virus crisis. Some companies just can’t find the proper materials and labor to get their projects done. The intricacies of these issues are industry specific, but across the board margins are tightening on companies from every angle including corporate taxation and increasing wage/salary pressures. This could turn into some serious headwinds for the earnings of companies and dampen the justification of valuations and current lofty levels.

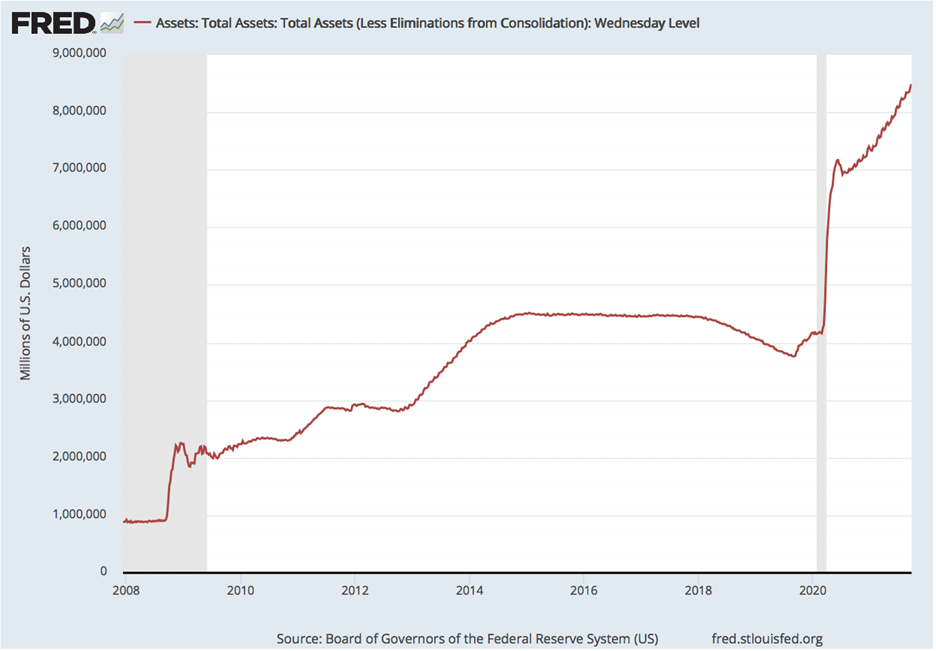

This is our worry list for now- so for our chart of the week we have the Federal Reserve’s balance sheet. This is an accounting of all of the assets they have sucked up in our financial markets over the years. One private entity (that has yet to be audited) owning this volume of assets is obviously ridiculous, but no one knows how much more ridiculous it can get before some breaking point is found…

Eight and a half trillion dollars – and counting? Wow…

One of the justifications for the creation of the FED (in the year 1913) was for it to be a lender of last resort in emergency and stave of economic/financial crisis. Now they are developing into the lender of first, middle and last resort for a comically financially profligate government. Because interest rates are so low, free markets won’t lend as much money to this government on a long-term basis that they “need.” Their balance sheet reflects buying all this debt from our government (and other assets of dubious valuation.) Historically this has been labeled “monetization of debt.” We’re not sure what people are calling it now, but it seems to us that the FED is actually creating rather than preventing financial crisis. The cure has become worse than the disease – surprise, surprise…

Clearly this won’t end well. However, we still don’t see imminent doom – but we will keep looking!

Regards and good investing,

Greyson Geiler

by Greyson Geiler | September 20, 2021

After a summer hiatus and without posting our weekly writeup, we are back after it and preparing for the fall. Hopefully all readers are healthy and happy and ready for the holiday season – of course Covid-free as the weather cools off!

Looking at the financial markets as we head into the historically dangerous part of the year, the same situation is playing out that we have been describing for quite some time now. The Central Banks of the world are drowning financial markets in “liquidity” – meaning basically they are printing a ton of cash! Historically when so many currency units were conjured up the price of day to day living rocketed higher. Of course, there are many stories of people in the Weimar Republic in Germany taking long lunch breaks during workdays to go spend money in stores before the afternoon came and prices were higher. Domestically some of us have the memories of the 1970s where the Nixon Administration implemented price and wage controls on the American economy to stifle inflation in many industries. (Donald Rumsfeld was in one of the positions of control as the director of the “Cost of Living Council” – not a joke, look it up!) Of course, there were many unintended consequences of attempted centralized control, but that discussion is for a different post…

Mark Twain said it best – history doesn’t repeat, it rhymes. In this episode of currency unit creation by the Central Banks the inflation has taken a different shape. That of asset price inflation…

Technological innovation has brought about amazing efficiencies – in food production as an example -over the last few decades. Many of the day-to-day consumption expenses such as food and energy just haven’t rocketed higher to the degree even that we saw in the 2011 commodity launch. On top of that, America is aging and bulging at the waist, so freshly printed money doesn’t really flow into consumption type goods the way it comparatively did in the past. This time around excess “liquidity” is getting piled into financial and real estate markets. Bonds in particular are of completely manipulated prices as interest rates are artificially suppressed by the FED. The bond market as a whole has historically feared inflation. Now bond investors assume that the FED will keep prices elevated and they continue to buy. Look at the percentage of JUNK bonds in the U.S. market that yields less than THE GOVERNMENT’S OWN CALCULATION OF INFLATION.

That’s right, in real terms you are not even making money on 90% of JUNK bonds and you are taking a lot of risk (if you are not taking the risk and own treasuries you are losing a lot of money in real terms because the yield is so low.) When you look at the chart historically, you can see that this is quite the anomaly. The percentage of JUNK bonds losing money after calculating in the inflation numbers has never even been 10% before now! The Federal Reserve says that the high inflation numbers that are making these JUNK bonds yield negative in real terms is transitory. The FED is saying that inflation will subside in coming months as supply chains are bandaged back together following this Covid destruction. Well, they better be right because this is an unsustainable situation as the FED is purchasing $120 Billion per month of assets on the open market and fueling this inflation AND the financial markets.

But the trillion dollar question is when will the FED take their foot of the gas and stop pouring $120 Billion per month into financial markets? Justification for all of these asset purchases, interest rates artificially low and basic currency creation by the world’s central banks of course has been the Covid situation over the last 18 months or so. Now financial markets are running into a snag with the Chinese real estate situation and the Evergrande bond default. Many are drawing parallels between this and the Lehman Brothers situation in the U.S. in 2007. Will the Evergrande situation spiral downwards into a contagion like the “Schemin” Brothers situation? Will the FED stop supporting markets with the possibility of that on the horizon? We find it difficult to believe that they will get religion now and try to let the financial markets stand on their own feet. We guess that one of the FED governors this week will make a statement that the tapering of FED support will get put on hold until the Chinese situation is resolved. We also guess that the Bank of China will calm markets down with additional “stimulus” in the near term as well.

Of course, with all of the tens of trillions of dollars of leverage in the world’s financial markets, eventually the Central Banks won’t be able to save the day. We are not speculating when that will be. In the meantime, don’t sell your gold.

Regards and good investing!

Greyson Geiler

by Greyson Geiler | June 28, 2021

When we are describing conditions in the financial markets, interest rates are of very high concern and commonly mentioned at the forefront. We need to understand that there are many different interest rates in the world economy, but they are all essentially the price of money – so they are really the most important prices at the foundation of our money systems. Now, the most obvious interest rate – and the one that we complain about most in this post – is the “discount rate” which is essentially the short-term interest rate which companies can borrow, and it is set by the Federal Reserve. We have been pounding it for years now that the Federal Reserve is in dereliction of its duty as steward of our monetary system specifically with regard to how low they have kept the short-term rates that they are explicitly responsible for and they have kept them too low FOR DECADES. Former Federal Reserve Chairman Alan Greenspan was too quick to reduce interest rates after the “dot bomb” in 2001-02-03. Former Federal Reserve Chair Janet Yellen left the discount rate at essentially zero for MORE THAN EIGHT YEARS after the 2008 disaster. That’s right, emergency policies of zero interest rates (free money) kept going for eight years. Speaking of emergency policies, the Fed still has interest rates at zero due to this Covid-19 mess – plus they are buying $120 billion of bonds in the market to keep long term interest rates down too. This is in the face of a white-hot residential housing market where demand is so high that materials are tough to source and outrageously higher in price. There are many other economic indicators other than the housing market that should be enough for the Fed to remove their emergency monetary measures. But they still have the pedal to the metal. The result of the price of money being next to zero is an explosion of debt across the entire developed world and wild speculative excesses in many asset markets. By many measures the stock market is more expensive (in America) than it has ever been in history. But my favorite example of how insane markets have gotten is in the art/collectible world. At a recent art auction an Italian sculptor sold his “invisible” sculpture for $18,300. This is not an Onion article. There is nothing there, but the “sculpture” sold for more than half of the median annual income for America. Of course, that is just one data point, but it shows some of the ridiculousness being fueled by central banks across the developed world.

Of course, invisible sculptures aren’t going to get any traction in the mainstream art appreciation world, but the ridiculousness of low interest rates is all around us and is really the underlying fuel for silliness in asset markets. American corporations have binged on these low interest rates ringing up a total of more than $10 trillion in debt. By some analysis 20% of American companies are now “zombie” companies. Meaning their profit margin is below their cost of capital, so they have to keep borrowing money in order to stay in business. What would happen if the Fed changed short term interest rates back to something more normal AND they allowed longer term interest rates to rise? Likely we would have a deflationary implosion if the Fed’s profligacy came to an end. The kicker that we still have a tough time getting a handle on is the SOVEREIGN debt overseas (mostly Japan and Western Europe) that is actually yielding a negative interest rate. That is not from an Onion article either. We have more than $13 trillion of worldwide sovereign debt that you are guaranteed to lose money if you buy and hold to maturity. It is not surprising that the vast majority of this negative yielding debt is owned by Central Banks who are buying the debt with money that is someone else’s (taxpayers.)

Many of the traditional measures by which asset prices are valued break down when interest rates are negative. Bear in mind, we are NOT predicting immediate doom of the world economy and of financial markets. Look at the chart above and you can see that the negative-yielding circus in government bonds started almost a decade ago. No one knows how much more debt will end up on this negative yielding chart – and no one can time the demise of a monetary system. However, we do know that there will be consequences. One would hope that the Federal Reserve would start to remove some of this excess in terms of pricing capital for free and stop buying assets that the open market should find a buyer for. We are not sure if that could right the ship or not, but sadly we doubt the Federal Reserve is going to attempt more discipline so we could find out.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | June 14, 2021

There has been much discussion and debate in recent weeks whether the current blast of inflation is permanent – or as the Fed has intimated, transitory because of Covid-19 supply chain disruptions. Surprisingly, there has been a sharp drop in treasury yields recently even as we have had consistently these higher CPI prints. The annualized number for the Consumer Price Index is running at 8.3% which is the highest number since 1980.

Deutsch Bank’s Jim Reid, when looking at stubbornly negative real rates on Friday pointed out that the current gap between 10yr U.S. yields (1.5%) and U.S. CPI (5.0%) is a whopping 3.5%, the highest since 1980 (In fact, the gap has only been more negative for 10 months in the last 70 years, all of which were in 1974, 1975 or 1980). When you throw in the combo of inflation & labor shortages at U.S. small businesses is the highest since 1974 things get dicey. There are some obviously conflicting messages in financial markets, but the outlying indicator to us is lower treasury yields.

As absurd as it may seem, the bond market continues to suggest deflation is the more significant threat as we are currently at the largest deviation between annual CPI and interest rates since 1980. Ten year treasury rates leaking back below 1.5% certainly agrees with the Fed’s view that inflation is transitory and the treasuries are pricing in sub-2% inflation and economic growth.

Also consider the calculation logistics of some of these inflation rates and spreads. Over the next two quarters, the year-over-year rate of change will slow the “base effect” as the economic ”shutdown” is removed from the calculation. Essentially, the starting point that was set so low during Covid lockdowns for growth rates -and inflation rates- will come out of the equation. So inflation won’t look so bad but growth won’t look so good. Another consideration is the fact that real wages are not keeping up with the actual cost of living increases. Much of this may be mitigated by the transitory nature of some of the inflation – but not with the housing situation. Housing costs are up -not going down anytime soon – and discretionary spending is taking a hit. Especially as the stimulus is fading as Congress is scaling back some of the free money it is launching out, one would expect things to slow. It seems that the pulling forward of future consumption to now may have run its course and we have likely seen a near term peak in the economy and earnings growth.

Of course a huge part of the whole analysis of our economic future – and one we articulated our disagreement last week in this post – is the “liquidity” being offered by the Federal Reserve. Again, they are buying some $120 billion in assets every month and keeping short term interest rates essentially pinned to zero. They have said they would not start scaling back this huge stimulus until there had been “substantial further progress” in healing the U.S. job market. Of course, the description is ambiguous enough that they can justify whatever they want to do – but for now, markets are bracing for the chance the Fed will start to communicate its taper strategy at its Jackson Hole symposium in August, with possible action later in the year. We see current Fed policies as COMPLETELY RECKLESS and can’t imagine that even they will keep the pedal to the metal for the rest of the year. The Norwegian central bank has already announced plans to raise rates in the third or fourth quarter of 2021. New Zealand and South Korea have similarly dropped loud hints that policy tightening is on the agenda as conditions improve.

Central banks around the world are still in emergency policy mode and the stock market is pinned to all-time highs. The recent highs by a lot of measures aren’t showing a lot of zeal – and by some of the indicators we have mentioned, a pullback may be imminent. But that doesn’t mean that doom is right around the corner. The lower treasury yields imply that inflation fears are overdone and the stock market may have some time in “goldilocks” zone until unless the Fed pulls the plug. Stay tuned…

Regards and good investing,

Greyson Geiler