by Greyson Geiler | November 29, 2021

Here we go again…

The Omicron Variant is reportedly spreading around the world from a starting point in South Africa and it may be resistant to all the vaccinations. On the Friday after Thanksgiving that sent a huge shockwave through financial markets that put up some volatility numbers that were bigger than anything we have seen since March 2020. Much of the fear stems from the idea that lockdowns are imminent reminiscent of the summer of 2020 and the Dow Jones Industrial average – as an example – was down more than 1000 points for much of the short trading day. Of course, widespread lockdowns outside of Australia would likely return us to some dismal economic numbers in the near future. Some people are questioning the news saying that governments are claiming this variant is resistant to the vaccines just to cover up the fact that the vaccine efficacy has been shown to wane – sometimes only after a few months. Being pragmatists for the most part, we don’t like spend time on theories such as this, we just notice that the lockdowns may be fact. It looks like the Israelis may be the first in shutting down air travel from foreign countries. Mapping out details on that out will be a moving target as the situation progresses but stay tuned because this could start to get serious.

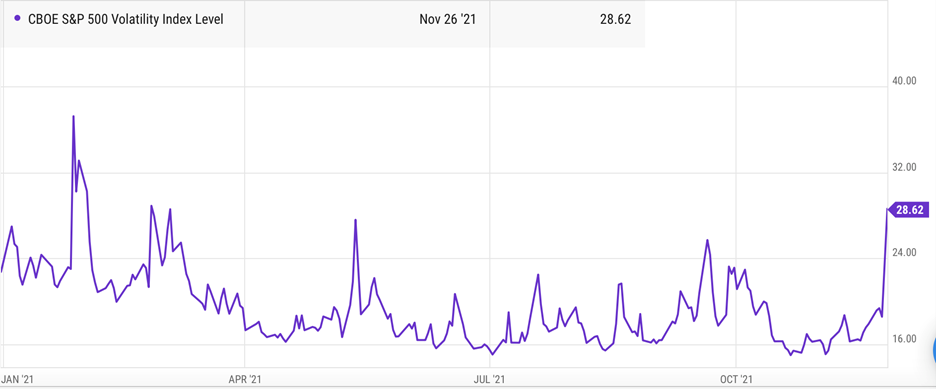

As far as the market’s reaction to the news on Friday, the VIX (volatility numbers) rocketed higher. This is not a huge surprise considering the continued uptrend in markets and real lack of “put buying.” This means that, by some historical measures, there was less insurance being bought by fund managers for the potential of a downside market move was at a very low number historically and near the low Year-To-Date. The VIX rocketed more than 50% in one day – this chart gives an indication of the fear that ravaged the market on Black Friday.

Clearly the stock market was overdue for a little “shaking of the tree” so to speak. Are the markets telling us there is more bad news coming and the Black Friday pullback was actually the start of something worse? At this point we don’t see that and the huge pullback in crude oil is one data point that is actually good news. As we have mentioned in previous weeks – we have a hard time believing that inflation is rampant and getting worse when we see charts of bonds rallying and commodities like gold and crude oil selling off. Well on Black Friday, crude oil sold off about 14% !!! That’s right an enormous move down in one of the big inflation-indicating assets. That is only one data point, so we have to remain diligent – maybe someone cracked the code on the “Holy Grail” of energy and figured out cold fusion on Friday. We doubt it. Friday’s selloff probably doesn’t mean the asset rally of the “everything bubble” is over yet – but if that move ruined your holiday weekend, it is time to reduce risk. The new Covid variant could turn out to be more than we anticipate – but only time will tell. Regardless of how serious the Omicron variant truly is, we are guessing volatility stays elevated for the foreseeable future – so stay tuned!

Regards and good investing,

Greyson Geiler

by Greyson Geiler | November 22, 2021

If you listen to radio adds encouraging you to refinance your mortgage, you may think that interest rates will be going higher imminently. You would get that same opinion from a lot of the financial market pundits who postulate that, considering inflation is running hotter than it has for thirty years in the US, long term interest rates would have to go higher in response. But these opinions have been running for quite some time now, and the ten-year treasury interest rate remains about 1.5% (recent inflation prints have been around 6%.)

So, what gives? Is the Federal Reserve going to raise short term interest rates to fight inflation? Are they going continue to ease off the treasury and mortgage-backed security purchases that have been running at a $120 billion per month pace?

Inflation has been surprisingly benign – really for decades – in conjunction, interest rates have continued their downward path that began in 1981. Recent Federal Reserve comments involve discussion of “transitory” inflation – meaning that expectations going forward are for inflation to subside. So even with big inflation prints and unemployment levels that are heading back toward pre-Covid levels, interest rates aren’t heading higher. Morgan Stanley’s head of quantitative research, Vishwanath Tirupattur just published his opinion that the Federal Reserve won’t even raise short term rates until 2023! Obviously only time will tell if MS is correct, but they are seeing supply chain healing and more people returning to work as pressures down on inflation. We mentioned a couple weeks ago that some market indicators look similar to us. https://andorracapital.com/a-different-look-at-inflation/

Inflation isn’t running rampant for now – but of course that can change.

Take a look at a chart of the recent price action of the US Dollar index:

Of course, this is an approximation of the value of the U.S. Dollar versus other currencies internationally – and heavily weighted toward the Euro. So, this is not a magic indicator of America’s economic strength. However, it is an indicator when coupled with charts of many world commodities including gold and oil (not going higher) that the US Dollar is not falling apart 1970’s style. Intuitively the actions of the Federal Reserve would ignite the inflation that many remember and fear from the 1970’s. Something different is at work, however and that is good news for us – for at least the near term. In light of that, we expect interest rates to remain historically low both short term and long term. But stay tuned for possible changes in our weather report.

Regards and good investing,

Greyson Geiler

by Greyson Geiler | November 8, 2021

There is a lot of talk in the economic/financial news about inflation – both what we are looking at today and expectations of future inflation. First let’s agree on the definition of inflation because we hear many different explanations. From 20,000 feet everyone can agree that the devaluation of a currency or stated differently, the decrease in the purchasing power of a currency is the core of the definition of inflation. The problem in measuring and quantifying inflation is where the disagreement starts. Some analysts see measuring inflation as a function of the money supply, while others define it as simply the increase in costs of a predetermined basket of goods. For the purposes of this discussion, we will consider inflation to be determined by the increase in the price of goods as the U.S. Bureau of Labor Statistics puts out. Many observers criticize the BLS and postulate that their mechanisms are faulty resulting in a continual understatement of the statistics that get published. We will leave that argument for a different discussion and use the BLS data.

Historically CPI – or Consumer Price Index – has been the go-to number to describe the inflation in the moment. Recently the BLS reported that for the year ending in September, CPI was 5.4% which is raising eyebrows. Of course, many of us are old enough to remember the double-digit inflation of the late 1970’s. Back then, the situation seemed so dire that we had to initiate Donald Rumsfeld as a de facto inflation czar, and he was tasked with putting governmental control on inflation. Clearly the situation today is nothing close to where we were then, but this is the highest number since the brief inflationary period of 1989-1990. So now the obvious question is – why would the Federal Reserve still have the pedal to the metal (effectively zero short term interest rates, buying $120B per month of bonds, and taking over the repo market) when inflation is running hotter than it has in decades? We don’t really like the answers to that question but here they are…

- The Federal Reserve has prepped us for this situation. They have said that with such a disruptive and deflationary event (Covid-19) they were willing to tolerate more than their typical 2% targeted inflation for some period of time – completely arbitrary – but that is what they said

- The Federal Reserve has labeled the present bout with inflation “transitory” meaning that they believe the temporary supply chain disruptions are causing short term problems that manifest in inflation numbers now, but will soon abate as supply chain disruptions are repaired

- Clearly the Federal Reserve has taken on a mandate of supporting asset prices – completely of their own accord. They have never been officially tasked with this mandate – however, they are obviously making decisions with this in mind

So, these reasonings of present Federal Reserve behavior are by no means complete. But they do give a basis for what is going on. We do not appreciate the concept of one entity having the sort of power the Fed does (although we do doubt that they control to do the degree the financial press implies.) They have poured amazing amounts of “liquidity” on the present situation – trillions and trillions of dollars – and yet we only have 5.4% inflation? Viewing with a historical lens one would expect runaway hyper-inflation. So, what gives? The Fed clearly wants and needs inflation (the mountains of debt in our system need to be devalued) – but it is quite mild considering their actions.

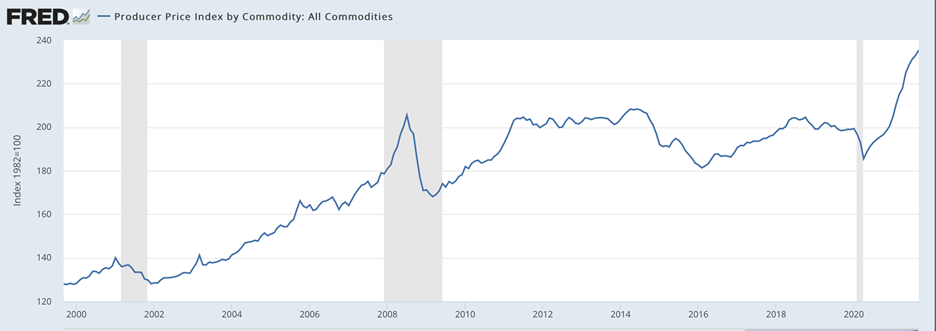

One thing we would like to point out is how far the PPI – or prices that producers are paying – have outpaced CPI. Supply chain issues have obviously been the catalyst to this launch in pricing that producers are experiencing. We are surprised considering this and other factors that CPI numbers – and the prices consumers pay for basically everything aren’t DRASTICALLY worse. Is this an indication that producers are having a tough time pricing their costs into what they charge consumers? Are business profit margins in trouble going forward?

To make sense of why consumer price inflation isn’t significantly worse than it is, we have to consider some deflationary factors that are running strong counterbalances to the Feds nauseating blizzard of “liquidity.”

- An aging population in the developed world is clearly a factor with loan demand from the big banks being tepid as an obvious manifestation. Baby boomers are consuming less and some of them full on downsizing and moving into group communities

- Mountains of debt require interest payments to be serviced. That imposes deflationary effects of tens of trillions of dollars of debt are being piled on top of existing mountains of debt in the developed world

- Technology is going parabolic creating amazing efficiencies in many different industries

We obviously have reservations of the monetary system as the Fed has designed it and is abusing it. However, when we try to read the tea leaves about consumer price inflation that may be coming in the near term, we believe that the fears have been overblown. Our list of potential deflationary reasons for that may be incomplete but something is holding hyperinflation at bay – that is good news! We believe that good news is at least part of what is pushing stock prices continually higher – so it is getting priced in as we speak. As soon as the financial media starts agreeing with us that may be an indication that asset prices are getting near a top – so stay tuned.

Regards and good investing!

by Greyson Geiler | November 1, 2021

In case you missed our post last week, we discussed the policies of the world’s central banks – specifically the inflation of asset prices worldwide. https://andorracapital.com/historical-ratio-divergence/ We don’t have perfect solutions to the world’s financial issues, but we certainly think there are better ways to approach the monetary system than relentlessly pouring trillions of dollars into asset markets like drunken sailors. Clearly this is not sustainable, but we have also repeatedly theorized that doom is not imminent. When you read the news there is plenty of bad news and we are still climbing the “wall of worry” in asset markets from bonds to stocks, commodities and real estate. Among the worries that are keeping buyers on the sidelines are the supply chain disruptions, potential tax law changes, the Chinese invading Taiwan, the Fed tapering their support of markets, new Covid regulations/outbreaks and may others. As long as people are still looking for reasons that asset market rallies will stop soon – we will probably continue to go higher.

When we start hearing about how great everything will be and there are no risks, that is when we need to start worrying about the end of market exuberance. We are certainly not there yet. To be clear, there is no precise calculation of when the bull market has run too far and it is time to sell. No one rings a bell at the top of a bull market and tells you to get out. We must do our best to read the tea leaves and estimate when it is time to reel in risk. Here is one indicator that is surprisingly positive and when more of this type of good news is made public, we need to assume that the information is priced into the market already. That indicator is the amount of corporate debt that America has amassed. Here is a historical chart of the amount of corporate debt outstanding as a percentage of the US Gross Domestic Product – or the best (although seriously flawed) guess that we have of the dollar figure of the U.S. economy.

Surprisingly, this is showing the amount of U.S. corporate debt in terms of percentage of the GDP screaming in back toward pre-Covid levels. This is really good news for the future of the U.S. economy. This is also quite a surprise considering the Covid-rattled economy that U.S. corporations are dealing with. Interest rates are historically low – very enticing for a company to issue more debt and yet corporations are bringing their leverage ratios back to where they were a couple years ago. Keep in mind that the Federal Reserve branch of St. Louis is only providing these numbers through the second quarter of this year – but the trend has continued even further through the third quarter. To be clear, the debt is still a big issue – but it is not the runaway profligacy that one might fear considering the situation (we cannot give the same props to the Federal Government, surprise surprise.)

So, there we have it. On a weekly post that consistently complains about the runaway debt numbers that are being rung up by individuals, corporations, and government entities, finally we have some good news. Let’s not let that get too far out of hand though – the debt numbers across the board are still ridiculous and getting worse. But this is obviously the first good news you have heard from us recently on the debt front. Ironically, the more good news you hear from us, the closer we are to the top of this amazing bull run in asset prices!

Regards and good investing,

Greyson Geiler

by Greyson Geiler | October 25, 2021

Many strange things are permeating our financial markets even as hopes of a “return to normal” are still the goal – at least on surface level for reasonable participants. Of course, the more control of the financial world taken by the Federal Reserve, the less likely a return to normal will be a smooth transition – honestly it may not ever actually be achieved. We have repeatedly discussed our distrust of the methodology of Fed (and other central bank) asset purchases within the world’s financial markets. How would we ever get back to normal in the financial world with an accumulation of assets that looks like this?

The vast majority of what you see on this chart are the bonds (sovereign and corporate) that the world’s central banks have accumulated. Everyone who reads this post on a regular basis knows that when bond prices go up, interest rates go down. So, the end result of all these purchases from bankers using money conjured out of thin air is artificially low interest rates- even way out the duration curve as the banks have set short term rates at essentially zero.

Interest rates are so low, that private investors are now going way out the risk curve for yield. That has distorted historical norms from the perspective of the price of ALL TYPES of assets and the ratios between them. In a recent post, we discussed how an astonishing 90% of JUNK BONDS were yielding a negative rate when taking into consideration inflation https://andorracapital.com/central-bank-liquidity/

That is a historical norm that is way out of whack. Others include things such as PE ratios of stocks (that everyone talks about) or the total stock market capitalization vs GDP, total corporate debt to GDP, US government debt to GDP and so on. The point is that our financial world is levered up and much of the historical analysis is getting thrown out the window when attempting to position resources.

In addition to many financial indicators that point to a volatile new world, worriers on the fundamental side have plenty to worry about as well. The biggest headline today is about the supply chain issues causing shipping containers to stack up outside of Long Beach, CA and other ports. We can add the energy supply problem – largely in Europe right now – and of course, the real estate market teetering on disaster in China. The corona virus isn’t gone, Australia is struggling while coming out of total lockdown and some provinces in China are showing a whole new surge in virus cases. In addition to that, Inflation is on everyone’s mind and is a serious concern. Our Treasury Secretary is talking about it, but our Federal Reserve Chair is the one that should be. Finally, almost like a cherry on top of the world’s geopolitical sundae is the thought that China may invade Taiwan in the near future.

When so many worries are hitting the headlines of our media – generally it means we are climbing a “wall of worry” in the stock market and the high isn’t in yet. That is likely where we are today. We are now sounding like a broken record – continually outlining serious potential problems in our socio-economic world – but ending with the thought that doom is not imminent…

So next week we will talk about some of the surprisingly good things that are going on (US corporate deleveraging as an example) so that it makes sense to then contemplate when we might see a topping out of asset prices.

Regards and good investing,

Greyson Geiler